Stratégie de trailing stop dynamique

Aperçu

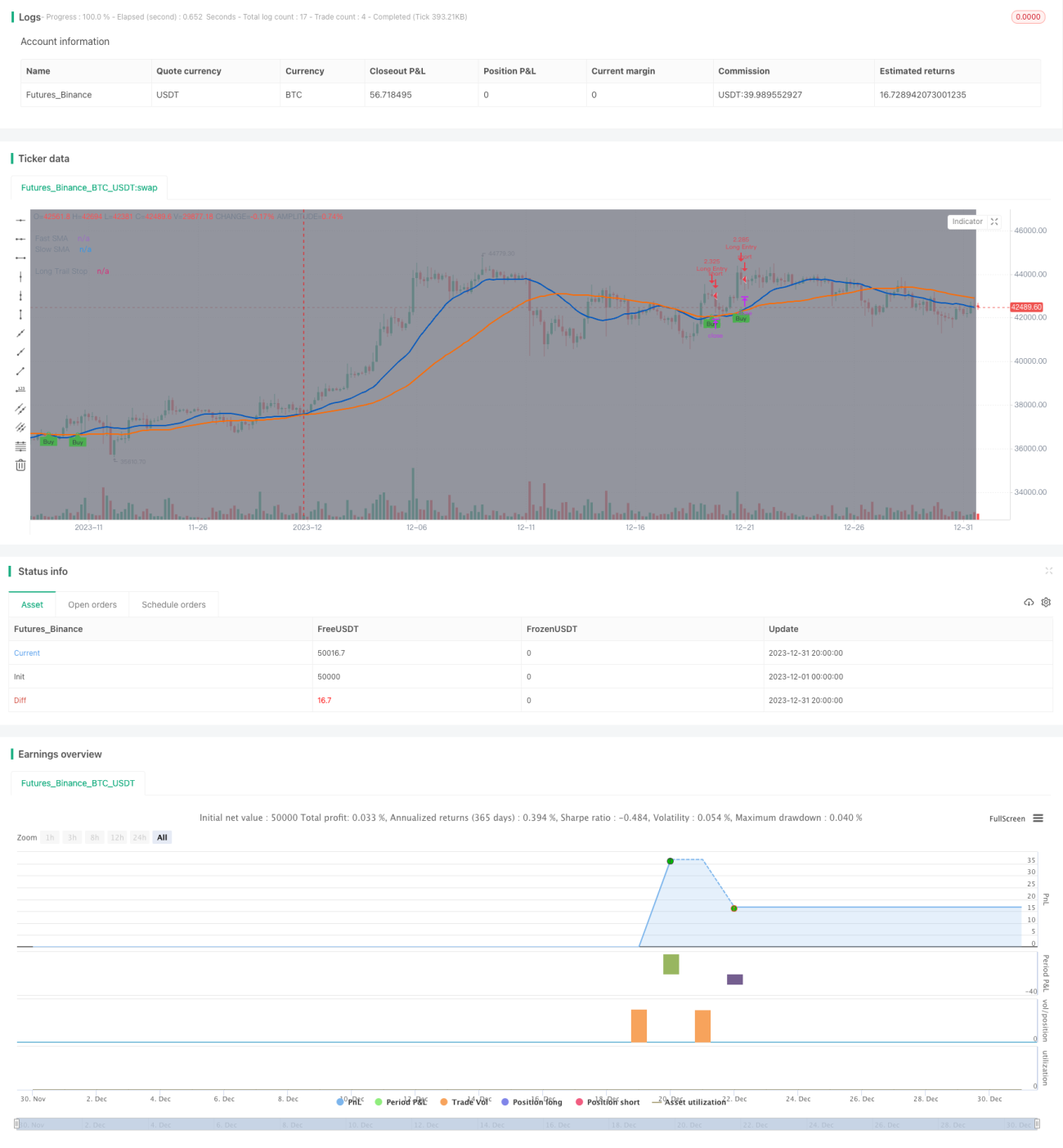

Cette stratégie détermine la tendance en calculant le croisement entre une moyenne mobile rapide et une moyenne mobile lente. Lorsque la moyenne mobile rapide passe au-dessus de la moyenne mobile lente, elle prend une position longue et définit un stop suiveur dynamique pour verrouiller les profits, et sort de la position lorsque le prix varie d'un certain pourcentage.

Principe de la stratégie

La stratégie utilise le croisement haussier (golden cross) entre la moyenne mobile rapide et la moyenne mobile lente pour identifier le début d'une tendance haussière. Plus précisément, elle calcule la moyenne mobile simple du prix de clôture sur une certaine période, compare les valeurs des moyennes rapide et lente, et lorsqu'elle dépasse celle-ci, juge que la tendance haussière a commencé et ouvre une position longue.

Après avoir ouvert une position longue, la stratégie ne définit pas un stop-loss fixe, mais utilise un stop suiveur dynamique pour verrouiller les profits. Ce stop est défini comme suit : prix le plus élevé * (1 - pourcentage de stop défini). Cela permet au stop de monter avec le prix, et de sortir lorsque le prix baisse d'un certain pourcentage.

L'avantage de cette approche est de pouvoir suivre une hausse sans limite, et de verrouiller les profits une fois qu'ils atteignent un certain niveau via le stop.

Analyse des avantages

Les principaux avantages de cette stratégie de stop suiveur dynamique sont les suivants :

-

Elle peut suivre une hausse sans limite et ne manque pas les grandes tendances. Un stop fixe peut facilement être déclenché trop tôt au début d'une grande tendance.

-

Elle permet de verrouiller les profits en définissant un pourcentage de stop. Sans stop, le gain peut se transformer en perte à la fin de la tendance. Le stop permet de sécuriser les profits.

-

Elle est plus flexible qu'un stop fixe. Un stop fixe ne peut être qu'à un seul prix, alors qu'ici il s'adapte au plus haut.

-

Le risque de retracement est plus faible. Avec un stop fixe, la distance entre le stop et le plus haut est grande, ce qui peut déclencher le stop lors d'un simple repli normal. Ici, le stop est très proche du plus haut, donc les replis normaux ne déclenchent pas le stop.

Analyse des risques

Cette stratégie comporte également certains risques :

-

L'indicateur utilisé pour identifier le signal d'entrée peut être instable et générer de faux signaux.

-

Une seule méthode de stop, sans considération d'autres facteurs. Un changement majeur soudain du marché pourrait rendre la stratégie inefficace.

-

Absence de take-profit, dépendance au stop. Si le stop échoue, cela peut entraîner des pertes importantes.

-

Les paramètres de données doivent être optimisés. Les périodes des moyennes mobiles et autres paramètres doivent être ajustés pour être optimaux.

Pistes d'optimisation

La stratégie peut être améliorée sur plusieurs aspects :

-

Ajouter plus d'indicateurs pour confirmer l'entrée et éviter les faux signaux. Par exemple, intégrer le volume.

-

Ajouter un take-profit, déclenché lorsque les gains atteignent un certain pourcentage.

-

Renforcer la sécurité du stop, par exemple en ajustant fortement la distance du stop en cas d'anomalie du marché.

-

Optimiser les paramètres en fonction des instruments et des périodes de trading. Les paramètres varient selon les instruments et les périodes.

-

Intégrer l'apprentissage automatique pour ajuster dynamiquement les paramètres, permettant au modèle d'optimiser automatiquement l'indicateur et la largeur du stop.

Résumé

La logique globale de cette stratégie est claire et raisonnable. L'utilisation des croisements de moyennes mobiles pour juger de la tendance est une méthode classique, et l'emploi d'un stop suiveur dynamique permet de verrouiller efficacement les profits et de réduire les risques. Cependant, ces indicateurs et paramètres doivent être continuellement testés et optimisés pour que la stratégie soit rentable de manière stable. Il faut également se prémunir contre l'impact de changements majeurs du marché sur la stratégie, en améliorant la structure globale et en ajoutant des mécanismes de sécurité.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1