Stratégie de suivi de tendance patiente

Aperçu

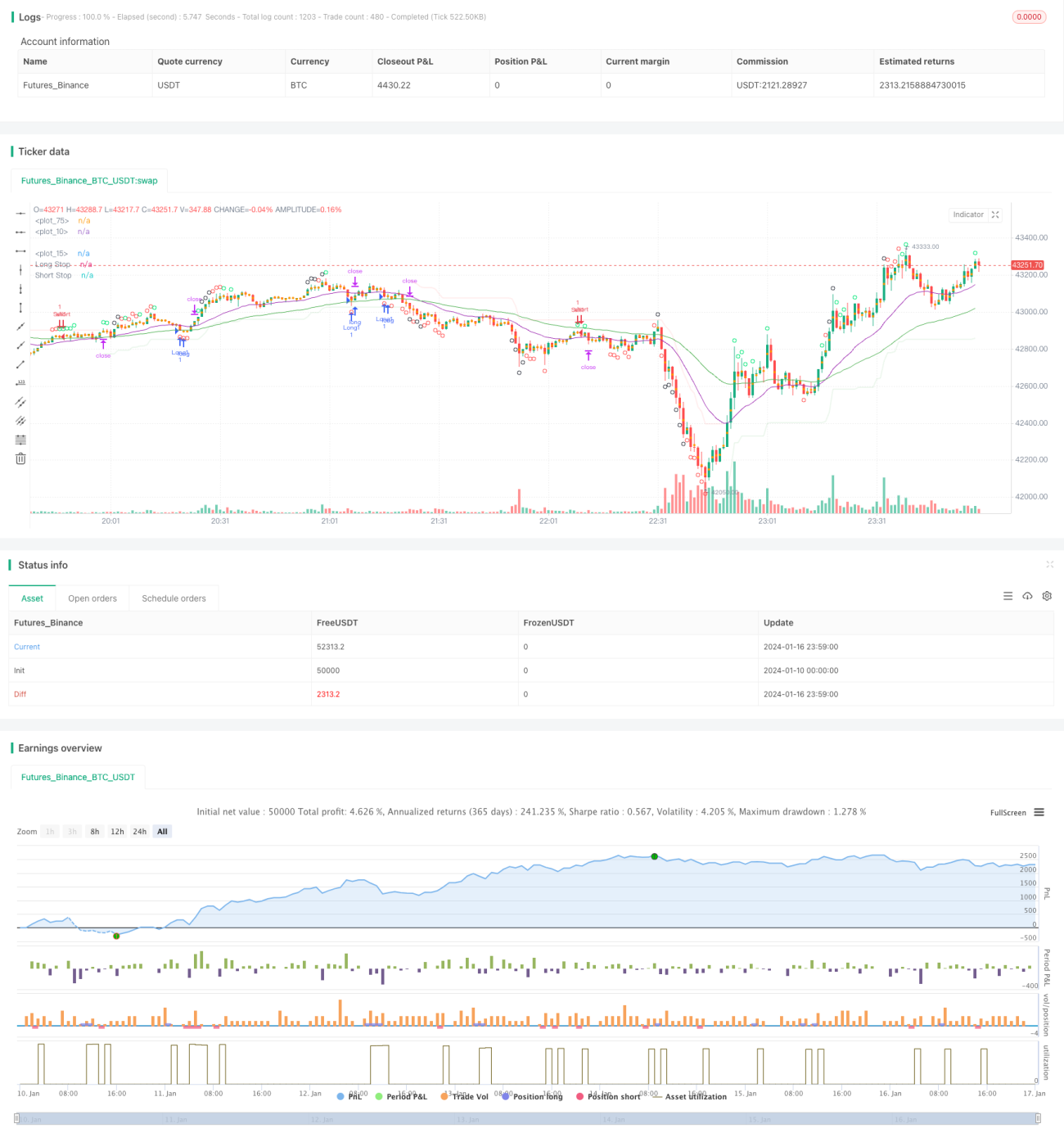

La stratégie de suivi patient des tendances est une stratégie de suivi de tendance. Elle utilise une combinaison d'indicateurs de moyennes mobiles pour déterminer la direction de la tendance et combine l'indicateur de surachat/survente CCI pour générer des signaux de trading. Cette stratégie recherche les grandes tendances et permet d'éviter d'être piégé dans des marchés oscillants.

Principe de la stratégie

La stratégie utilise la combinaison des EMA sur 21 et 55 périodes pour déterminer la direction de la tendance. Lorsque l'EMA court terme est au-dessus de l'EMA long terme, la tendance est définie comme haussière ; lorsqu'elle est en dessous, la tendance est définie comme baissière.

L'indicateur CCI est utilisé pour détecter les situations de surachat/survente. Un croisement à la hausse de la ligne -100 par le CCI est un signal de survente en bas, et un croisement à la baisse de la ligne 100 est un signal de surachat en haut. En fonction des différents niveaux de surachat/survente du CCI, la stratégie se décline en trois niveaux d'intensité de signal de trading.

Lorsque la tendance est jugée haussière et que le CCI émet un fort signal de survente en bas, une position longue est ouverte. Lorsque la tendance est jugée baissière et que le CCI émet un fort signal de surachat en haut, une position courte est ouverte.

Le stop-loss est défini par l'indicateur SuperTrend, et le take-profit est fixé en points.

Analyse des avantages

Les principaux avantages de cette stratégie sont les suivants :

- Suivi des grandes tendances, évitant d'être piégé

- L'indicateur CCI peut identifier efficacement les points de retournement

- Le stop-loss SuperTrend est correctement configuré

- Stop-loss fixe et take-profit fixe, risque contrôlable

Analyse des risques

Les principaux risques de cette stratégie sont les suivants :

- Probabilité d'erreur dans le jugement de la grande tendance

- Probabilité de signaux faux de l'indicateur CCI

- Probabilité de stop-loss inutile en raison d'un niveau de stop trop serré ou trop large

- Probabilité que le take-profit fixe empêche de suivre la tendance pour réaliser des gains

Pour faire face à ces risques, nous pouvons optimiser en ajustant les paramètres de période des EMA, les paramètres du CCI ainsi que les niveaux de stop-loss et de take-profit. Il est également nécessaire d'introduire davantage d'indicateurs pour valider les signaux de la stratégie.

Axes d'optimisation

Les principaux axes d'optimisation de cette stratégie sont :

- Tester davantage de combinaisons d'indicateurs pour trouver de meilleurs indicateurs de jugement de tendance et de validation de signaux.

- Utiliser un stop-loss et un take-profit dynamiques basés sur l'ATR pour mieux suivre la tendance et contrôler le risque.

- Introduire des modèles d'apprentissage automatique entraînés sur des données historiques pour estimer la probabilité de la tendance.

- Ajuster et optimiser les paramètres pour différents instruments.

Résumé

La stratégie de suivi patient des tendances est dans l'ensemble une stratégie de suivi de tendance très pratique. Elle utilise les moyennes mobiles pour déterminer la direction de la grande tendance, l'indicateur CCI pour détecter des signaux de point de retournement, et le stop-loss SuperTrend est correctement défini. Grâce à l'ajustement des paramètres et à la validation par combinaison de multiples indicateurs, cette stratégie peut être encore optimisée et mérite d'être testée en trading réel à long terme.

- 1