Stratégie de suivi de tendance solide comme un roc

Aperçu

Cette stratégie est basée sur la combinaison du canal mixte SSL, de la version améliorée du QQE et de l'indicateur d'explosion de Vada Ata. Elle permet de suivre la tendance de manière robuste et d'obtenir des rendements stables sur les grandes cryptomonnaies comme le BTC et l'ETH, ce qui la rend adaptée aux opérations à moyen et long terme.

Principe de la stratégie

Logique d'entrée

Conditions d'entrée en position longue :

- Le cours de clôture est supérieur à la ligne de base du canal mixte SSL.

- La couleur de l'indicateur QQE amélioré devient bleue.

- L'indicateur d'explosion de Vada Ata est vert.

Conditions d'entrée en position courte :

- Le cours de clôture est inférieur à la ligne de base du canal mixte SSL.

- La couleur de l'indicateur QQE amélioré devient rouge.

- L'indicateur d'explosion de Vada Ata est rouge.

Logique de sortie

Conditions de sortie pour une position longue :

- La couleur de l'indicateur QQE amélioré devient rouge.

Conditions de sortie pour une position courte :

- La couleur de l'indicateur QQE amélioré devient bleue.

Analyse des avantages

Cette stratégie présente les avantages suivants :

- La combinaison de trois indicateurs garantit la précision et la stabilité des signaux de trading.

- La ligne de base du canal SSL et l'indicateur QQE amélioré permettent de capter efficacement la direction de la tendance.

- L'indicateur d'explosion de Vada Ata valide davantage les signaux de trading et évite les fausses cassures.

- La structure du code est claire, facile à comprendre et à modifier.

- Elle intègre des mécanismes complets de stop-loss, take-profit et de gestion des risques pour contrôler efficacement les risques.

- Sur des périodes de temps plus longues (comme 1 heure, 4 heures), les backtests montrent d'excellentes performances.

Analyse des risques

Cette stratégie présente également les risques suivants :

- Sur des périodes courtes (comme 5 minutes), les résultats des backtests sont médiocres.

- Sur des marchés très volatils, le stop-loss peut être déclenché fréquemment.

- Sur certaines cryptomonnaies spécifiques, les résultats des backtests peuvent être décevants.

Pour faire face à ces risques, les mesures suivantes peuvent être prises :

- L'utiliser uniquement pour des opérations à moyen et long terme, éviter le trading à court terme.

- Élargir raisonnablement la marge de stop-loss pour éviter des déclenchements trop fréquents.

- Tester davantage de sous-jacents pour trouver les cryptomonnaies correspondant aux caractéristiques de cette stratégie.

Pistes d'optimisation

Cette stratégie peut être optimisée sur les aspects suivants :

- Tester différents réglages de paramètres pour trouver la combinaison optimale.

- Ajouter des éléments d'apprentissage automatique pour rendre la stratégie plus adaptable.

- Intégrer plusieurs facteurs comme les indicateurs de sentiment pour améliorer la stabilité globale du système.

- Étudier les caractéristiques du secteur, ajuster les paramètres pour que la stratégie s'applique à un secteur spécifique.

- Ajouter un module de trading algorithmique pour passer des ordres de manière programmée et améliorer les rendements.

Conclusion

Dans l'ensemble, cette stratégie est recommandée. Elle est stable, facile à comprendre et dispose d'un système complet de gestion des risques. Avec les sous-jacents et les périodes de temps appropriés, elle peut générer de bons rendements. Grâce à une optimisation et un ajustement continus, elle peut devenir un outil d'investissement quantitatif efficace.

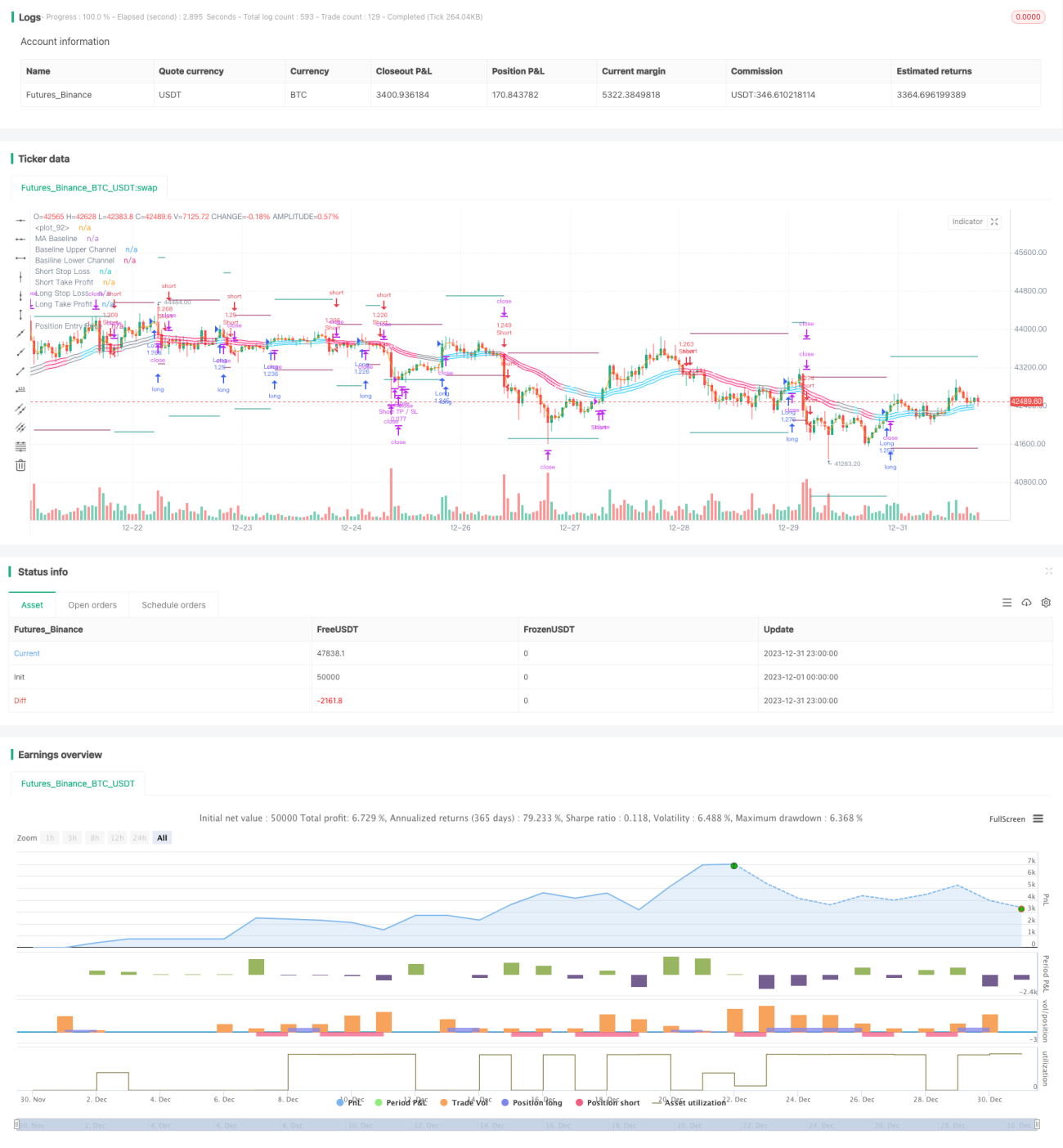

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1