Stratégie de trading de cassure bidirectionnelle basée sur les chandeliers K

Aperçu

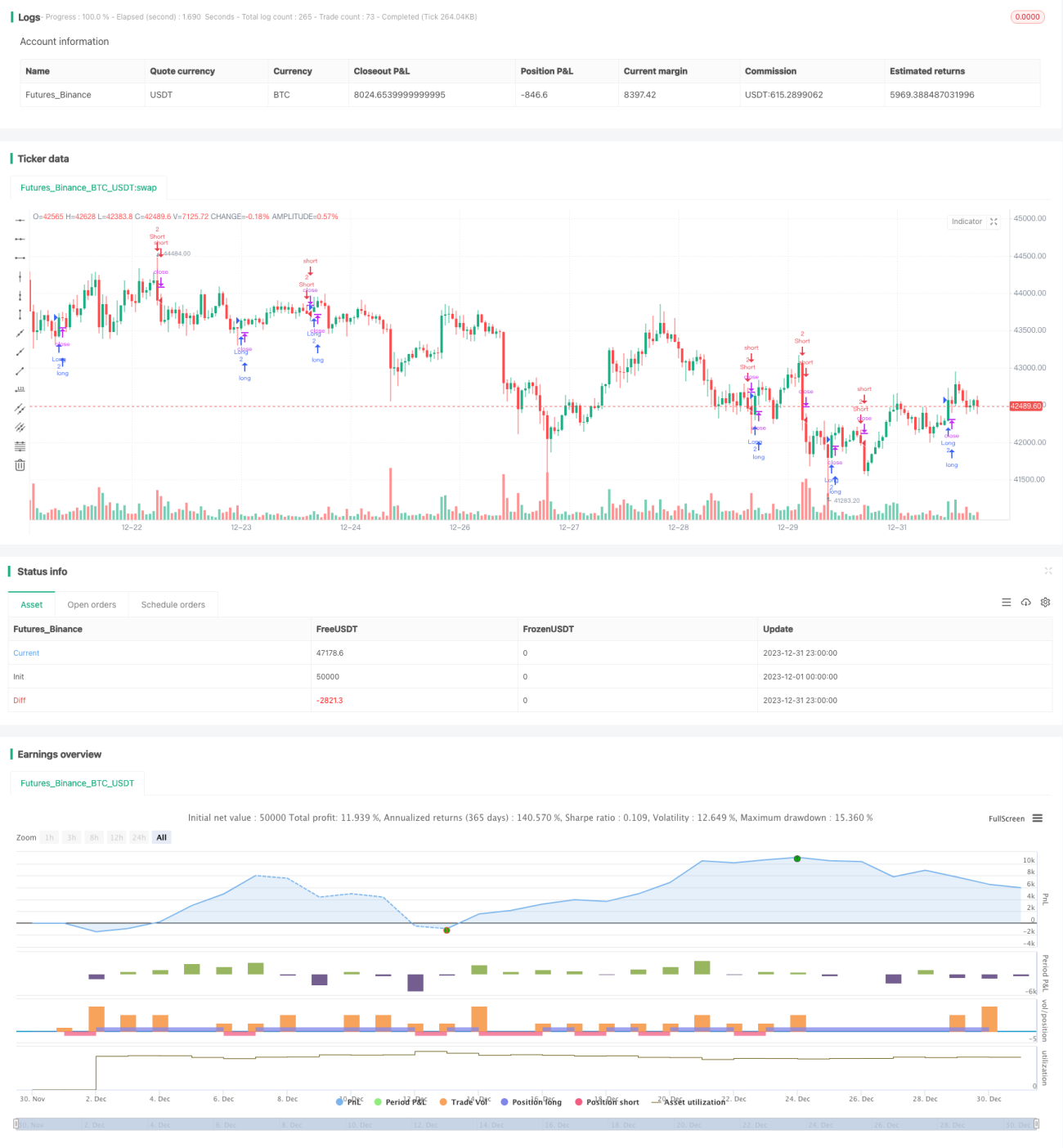

Il s'agit d'une stratégie de trading par cassure bidirectionnelle basée sur les chandeliers (bougies). Elle génère un signal de transaction lorsque le cours de clôture de la bougie actuelle casse à la fois le plus haut et le plus bas des deux bougies précédentes.

Principe de la stratégie

La logique de base de la stratégie est la suivante :

-

Définition du signal haussier :

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]. Cela signifie que le cours de clôture de la bougie actuelle est supérieur à son cours d'ouverture, et supérieur au plus haut des deux bougies précédentes, tandis que le plus bas de la bougie actuelle est inférieur au plus bas de la bougie précédente. -

Définition du signal baissier :

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]. Cela signifie que le cours de clôture de la bougie actuelle est inférieur à son cours d'ouverture, et inférieur au plus bas des deux bougies précédentes, tandis que le plus haut de la bougie actuelle est supérieur au plus haut de la bougie précédente. -

Lorsque le signal haussier se déclenche, on ouvre une position longue ; lorsque le signal baissier se déclenche, on ouvre une position courte.

-

Il est possible de définir un stop loss et un take profit.

Cette stratégie exploite les caractéristiques des cassures bidirectionnelles en identifiant les changements de tendance par le franchissement de niveaux de prix clés, générant ainsi des signaux de transaction.

Avantages

Il s'agit d'une stratégie de cassure relativement simple et intuitive, présentant les avantages suivants :

-

Logique claire, facile à comprendre et à mettre en œuvre, seuil d'entrée bas.

-

Les cassures sont des signaux de trading courants, susceptibles de générer des tendances.

-

Permet de trader à la fois à la hausse et à la baisse, offrant une opportunité de profit bidirectionnelle.

-

Possibilité de définir flexiblement un stop loss et un take profit pour contrôler le risque.

Analyse des risques

Cette stratégie comporte également certains risques :

-

Le trading bidirectionnel est plus risqué et nécessite une surveillance étroite.

-

Les cassures peuvent facilement être piégées, générant de faux signaux.

-

Un paramétrage inapproprié peut conduire à un excès de transactions.

-

Un stop loss et un take profit mal définis peuvent également affecter la rentabilité.

Il est possible d'optimiser les paramètres et de filtrer les instruments appropriés pour réduire les risques.

Pistes d'optimisation

La stratégie peut être optimisée dans les directions suivantes :

-

Optimiser les paramètres, tels que la période de cassure, l'amplitude du stop loss et du take profit.

-

Ajouter des conditions de filtrage pour éviter les faux signaux en cas d'arbitrage ou de range.

-

Combiner avec des indicateurs de tendance pour éviter les périodes de consolidation.

-

Optimiser la gestion du capital et améliorer l'algorithme de dimensionnement des positions.

-

Les paramètres variant selon les instruments, il est possible de tester et d'optimiser séparément.

Résumé

Il s'agit d'une stratégie simple basée sur le principe de cassure bidirectionnelle. Elle présente les avantages d'une logique claire et d'une mise en œuvre facile, mais comporte également un certain risque de surveillance. Grâce à l'optimisation des paramètres et des conditions, des résultats de trading satisfaisants peuvent être obtenus.

- 1