Stratégie quantitative de suivi de tendance basée sur les indicateurs Hull et LSMA

Aperçu

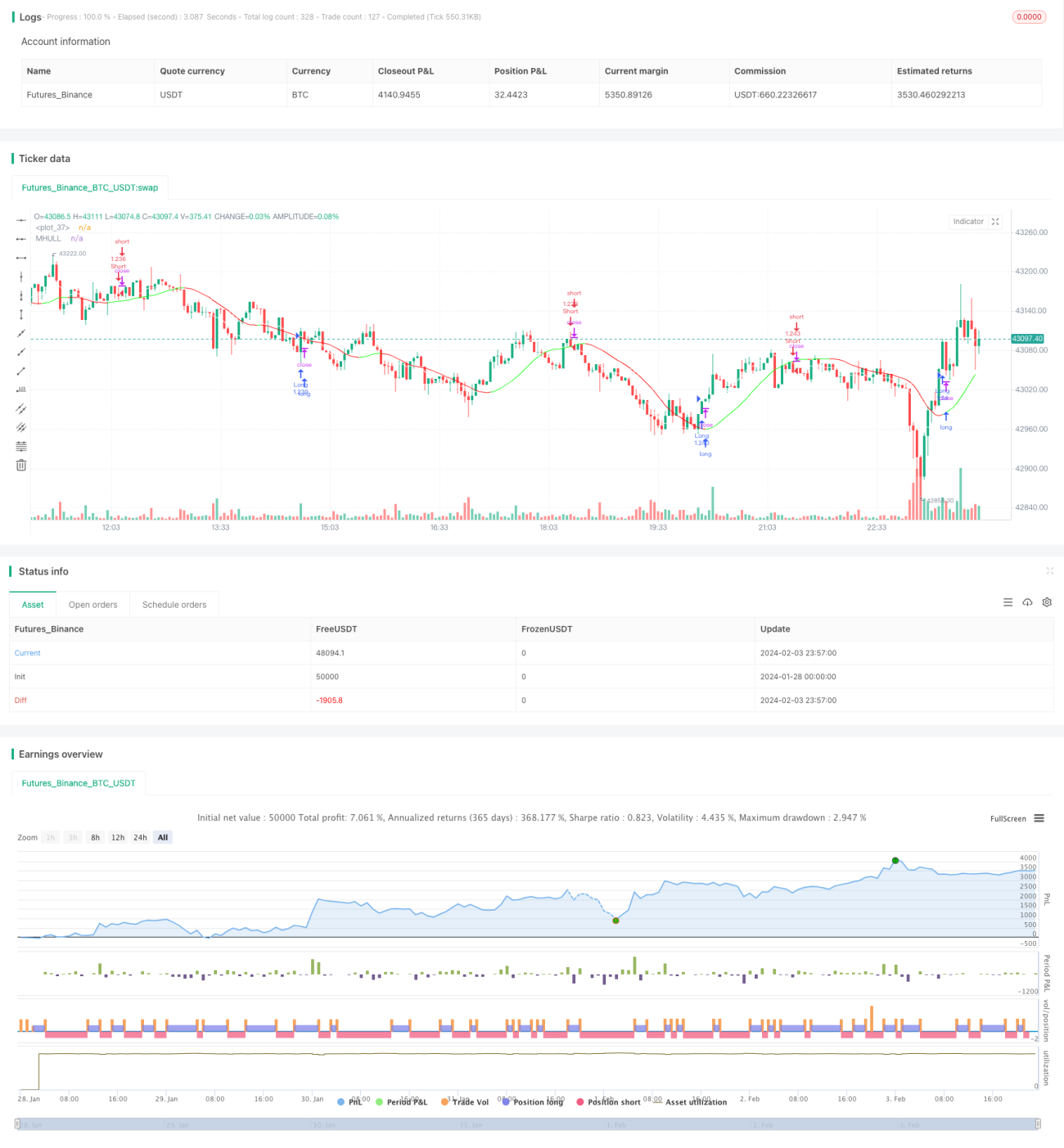

Cette stratégie combine l'indicateur Hull et l'indicateur LSMA (moyenne mobile des moindres carrés) pour identifier la direction de la tendance et les points de retournement, permettant ainsi de suivre la tendance. Lorsque l'indicateur Hull montre une tendance haussière et que la LSMA croise au-dessus de l'indicateur Hull, on prend une position longue ; lorsque l'indicateur Hull montre une tendance baissière et que la LSMA croise en dessous de l'indicateur Hull, on prend une position courte. Cette stratégie convient aux transactions à fréquence moyenne ou basse et peut être utilisée sur une unité de temps d'une minute.

Principe de la stratégie

-

L'indicateur Hull est utilisé pour déterminer la direction de la valeur de tendance. Lorsque la ligne médiane (MHULL) est au-dessus de la ligne inférieure (LHULL), cela indique une tendance haussière ; dans le cas contraire, une tendance baissière.

-

L'indicateur LSMA est utilisé pour identifier les points de retournement de tendance. Lorsque la LSMA croise au-dessus de la MHULL, cela signifie que la tendance haussière se forme ou s'accélère ; lorsqu'elle croise en dessous, cela indique que la tendance baissière se forme ou s'accélère.

-

En combinant les deux, lorsque l'indicateur Hull montre une tendance haussière (MHULL > LHULL) et que la LSMA croise au-dessus de la MHULL, on prend une position longue ; lorsque l'indicateur Hull montre une tendance baissière (MHULL < LHULL) et que la LSMA croise en dessous de la MHULL, on prend une position courte.

-

Le stop-loss est fixé au point de fluctuation le plus récent. Le stop-loss pour une position longue est le plus bas récent, et pour une position courte, le plus haut récent.

Analyse des avantages

Cette stratégie présente les avantages suivants :

-

L'indicateur Hull réagit rapidement et permet de capter les retournements de tendance en temps voulu ; la LSMA est lisse et fiable pour identifier les signaux de retournement. Leur combinaison est efficace.

-

En filtrant les faux signaux de l'indicateur Hull par les croisements de la LSMA, la probabilité de transactions erronées est réduite.

-

L'utilisation de points de fluctuation comme niveaux de stop-loss protège au maximum le capital.

-

Adaptée aux transactions à fréquence moyenne ou basse, elle peut être utilisée sur des unités de temps d'une minute, voire plus courtes, ce qui la rend largement applicable.

Analyse des risques

Cette stratégie présente également certains risques :

-

En période de marché sans tendance claire, les croisements multiples entre l'indicateur Hull et la LSMA peuvent entraîner des transactions trop fréquentes. Il convient d'ajuster les paramètres pour réduire la fréquence.

-

Le stop-loss basé sur les points de fluctuation peut être déclenché par des ajustements de prix à court terme. Il faut élargir l'écart des niveaux de stop-loss de manière appropriée.

-

En raison du décalage de la LSMA, il existe un léger risque d'erreur de jugement. Il est conseillé de confirmer avec d'autres indicateurs tels que les configurations de chandeliers.

Pistes d'optimisation

La stratégie peut être optimisée dans les directions suivantes :

-

Optimiser les paramètres de l'indicateur Hull et de la LSMA pour mieux les adapter à différents actifs et périodes.

-

Ajouter des filtres basés sur la volatilité, le volume de transactions, etc., pour éviter les transactions erronées en période de marché sans tendance.

-

Introduire des algorithmes d'apprentissage automatique pour aider à déterminer la propension de la tendance.

-

Utiliser des techniques d'apprentissage profond pour identifier les zones de support et de résistance clés, afin de rendre le stop-loss plus pertinent.

Résumé

Cette stratégie combine l'indicateur Hull et la LSMA pour juger les changements de direction de tendance et effectuer un suivi de tendance. Ses atouts sont la simplicité d'utilisation, une réactivité rapide et une large applicabilité dans le trading quantitatif à fréquence moyenne ou basse. En optimisant davantage les conditions de filtrage, les aides au jugement et les algorithmes de stop-loss, des résultats encore meilleurs peuvent être attendus.

- 1