सरल और समान खराब अनुबंध जाल

लेखक:नोबेल, दिनांकः 2021-11-18 17:28:35टैगः

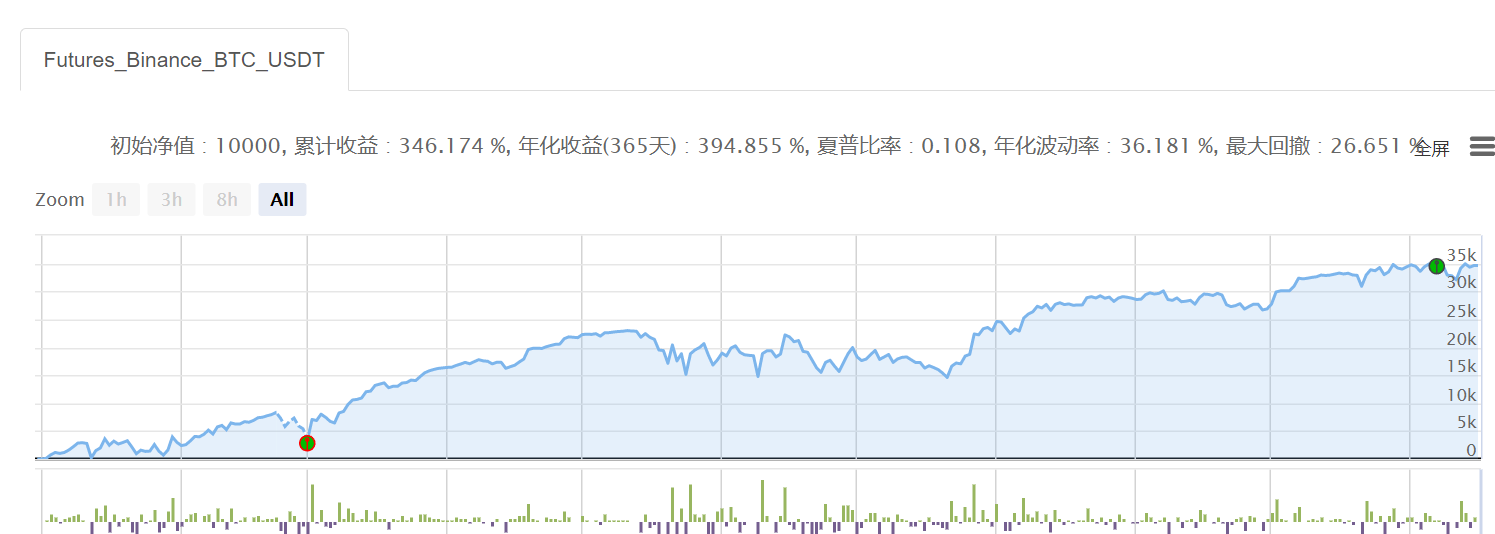

पैरामीटर बहुत सरल है, उदाहरण के लिए, बीटीसी के लिए, अधिक क्षेत्रों में सपाट, अधिक खुले क्षेत्रों में सपाट, और फिर से।

जाहिर है, मुद्रा के दायरे में, लंबे समय में, कोई भी जटिल मॉडल मस्तिष्कहीन ग्रिड से अधिक नहीं चल सकता है।

धन का पासवर्ड एक दिमाग रहित जाल + दिमाग रहित कुत्ता है।

आशा, पहले मार्टिन की तरह, सबसे सरल, सबसे असभ्य, लेकिन सबसे अच्छा रणनीति है।

'''backtest

start: 2021-01-01 00:00:00

end: 2021-11-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":2500}]

args: [["H",30],["n1",0.001],["grid",300],["xia",50000]]

'''

def CancelPendingOrders():

orders = _C(exchanges[0].GetOrders)

if len(orders)>0:

for j in range(len(orders)):

exchanges[0].CancelOrder(orders[j].Id, orders[j])

j=j+1

def main():

exchange.SetContractType('swap')

exchange.SetMarginLevel(M)

currency=exchange.GetCurrency()

if _G('buyp') and _G('sellp'):

buyp=_G('buyp')

sellp=_G('sellp')

Log('读取网格价格')

else:

ticker=exchange.GetTicker()

buyp=ticker["Last"]-grid

sellp=ticker["Last"]+grid

_G('buyp',buyp)

_G('sellp',sellp)

Log('网格数据初始化')

while True:

account=exchange.GetAccount()

ticker=exchange.GetTicker()

position=exchange.GetPosition()

orders=exchange.GetOrders()

if len(position)==0:

if ticker["Last"]>shang:

exchange.SetDirection('sell')

exchange.Sell(-1,n1*H)

Log(currency,'到达开空区域,买入空头底仓')

else:

exchange.SetDirection('buy')

exchange.Buy(-1,n1*H)

Log(currency,'到达开多区域,买入多头底仓')

if len(position)==1:

if position[0]["Type"]==1:

if ticker["Last"]<xia:

Log(currency,'空单全部止盈反手')

exchange.SetDirection('closesell')

exchange.Buy(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('sell')

exchange.Sell(sellp,n1)

exchange.SetDirection('closesell')

exchange.Buy(buyp,n1)

if len(orders)==1:

if orders[0]["Type"]==1: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

if orders[0]["Type"]==0:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if position[0]["Type"]==0:

if ticker["Last"]>float(shang):

Log(currency,'多单全部止盈反手')

exchange.SetDirection('closebuy')

exchange.Sell(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('buy')

exchange.Buy(buyp,n1)

exchange.SetDirection('closebuy')

exchange.Sell(sellp,n1)

if len(orders)==1:

if orders[0]["Type"]==0: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if orders[0]["Type"]==1:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

- बीयर के सिक्के के लिए बैल यू की संतुलन रणनीति

- डिजिटल मुद्रा वायदा बहुआयामी एटीआर रणनीति (शिक्षण)

- USDT को अनुबंध खाते से नकदी/धन खाते में स्थानांतरित करें ((OKEX, बिनान साथ में समर्थित)

- बिनाइन लेनदेन टर्मिनल धन हस्तांतरण टूल

- खाते में सभी ऑर्डर दिखाए गए हैं

- बिआन ने मैन्युअल रूप से ब्रीजिंग उपकरण खोला

- HttpQuery के माध्यम से सीधे बिनान के स्ट्रिंग डेटा प्राप्त करें

- डिजिटल मुद्राओं के लिए बहुआयामी द्विआधारी रणनीति (शिक्षण)

- प्रमुख एक्सचेंजों में पूंजीगत दरों का योग

- डिजिटल मुद्रा वायदा द्वि-समान रेखा मोड़ रणनीतियाँ (अध्यापन)

- वर्तमान सूचकांक संतुलन रणनीति v1.1 ((कुछ समय से चल रहा था, अब एक बग का संदेह है, क्योंकि यह काम नहीं करता है, इसे संशोधित किया जाना चाहिए)

- सिक्का usdt अनुबंध के लिए सभी मुद्राओं का नाम प्राप्त करें

- बिनान वेबसॉकेट सदस्यता स्थायी अनुबंध बाजार की जानकारी

- सिक्का के लिए नई कीमतें

- किसी ने धमाका किया तो उसने उल्टा मोड़ लिया

- स्वचालित रूप से बिआन स्थायी अनुबंध ट्रेडिंग सटीकता और न्यूनतम खोलने की स्थिति प्राप्त करें

- स्थायी अनुबंध के लिए एक-बंद बाजार मूल्य बेंचमार्क

- मौद्रिक संतुलन रणनीति - 0.0.1v

- बिनान कॉन्ट्रैक्ट ग्रिड - 0.0.2v

- सूचकांक हेजिंग (शूलो क्षेत्र) 0.0.1

मेक्समिनfor के लिए एक समस्या है।

हल्के बादलकृपया बताएं, वास्तविक डिस्क में त्रुटि है Traceback (most recent call last): File "

हल्के बादल

हल्के बादलअच्छा, धन्यवाद।

नोबेलस्थिति के लिए एक स्ट्रक्चरल सरणी को देखो, यह यहाँ एक समस्या होनी चाहिए।