SMA, EMA और वॉल्यूम पर आधारित एक सरल मोमेंटम रणनीति

अवलोकन

यह रणनीति एक गैर-शॉर्ट (केवल लॉन्ग, शॉर्ट नहीं) सरल इंट्राडे मोमेंटम रणनीति है। यह SMA, EMA और वॉल्यूम संकेतकों का उपयोग करके सर्वोत्तम समय पर बाजार में प्रवेश करने का प्रयास करती है (जब कीमत और मोमेंटम दोनों बढ़ रहे हों)। इसका लाभ यह है कि यह सरल है और प्रवृत्ति की पहचान करने की क्षमता रखती है।

रणनीति सिद्धांत

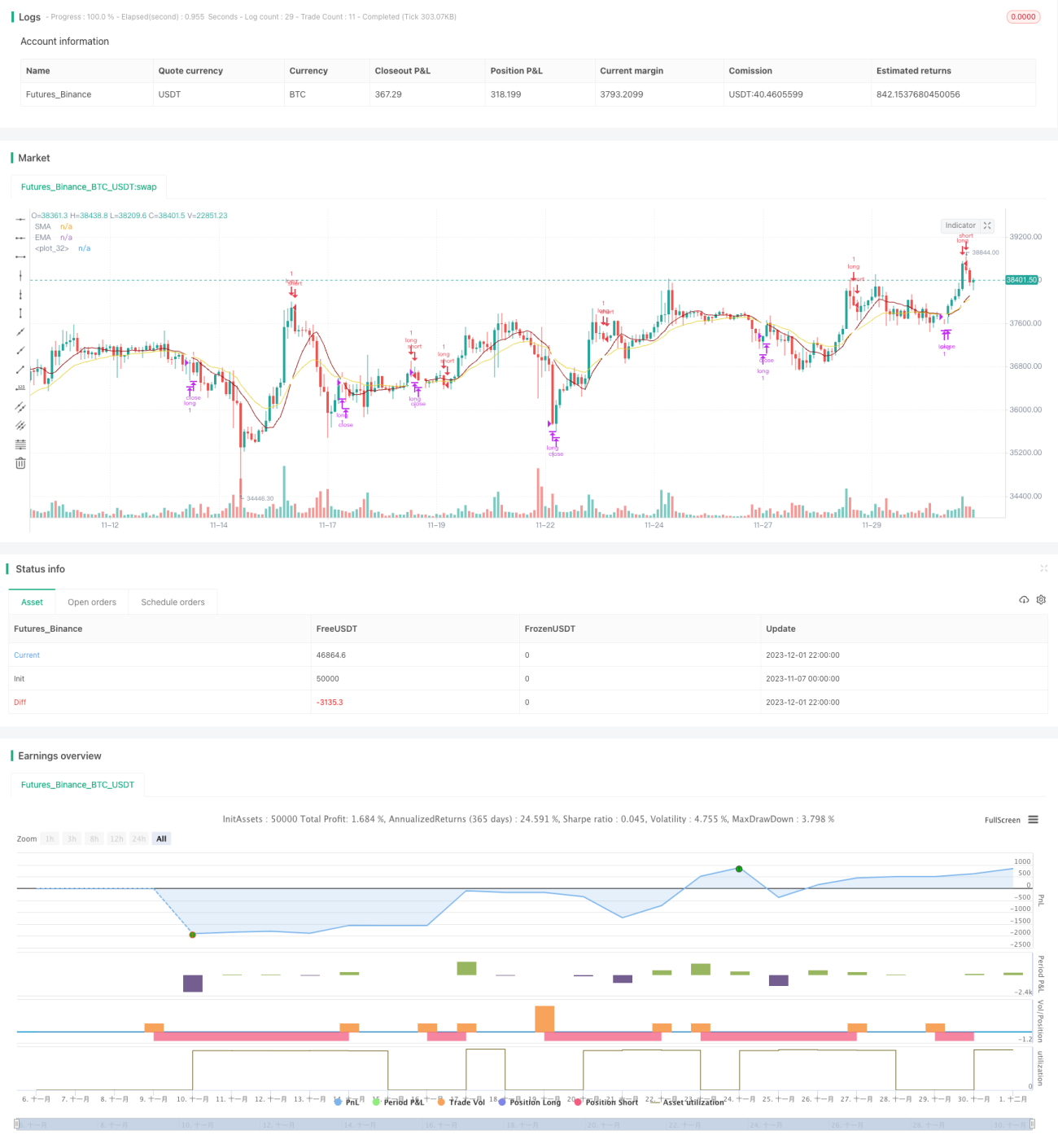

इस रणनीति के Entry सिग्नल उत्पन्न करने का तर्क इस प्रकार है: जब SMA संकेतक EMA संकेतक से ऊपर हो और लगातार 3 या 4 कैंडल्स एक ऊपर की प्रवृत्ति बना रहे हों, तथा बीच की कैंडल का सबसे कम मूल्य प्रारंभिक बढ़ती कैंडल के खुलने के मूल्य से अधिक हो, तब Entry सिग्नल उत्पन्न होता है।

Exit सिग्नल उत्पन्न करने का तर्क: जब SMA संकेतक EMA संकेतक को नीचे से पार करता है, तब Exit सिग्नल उत्पन्न होता है।

यह रणनीति केवल लॉन्ग पोजीशन लेती है, शॉर्ट नहीं। इसके Entry और Exit तर्क लगातार बढ़ती प्रवृत्ति की कुछ हद तक पहचान करने में सक्षम हैं।

लाभ विश्लेषण

इस रणनीति के निम्नलिखित लाभ हैं:

- रणनीति का तर्क सरल है, समझने और लागू करने में आसान है।

- इसमें SMA, EMA और वॉल्यूम जैसे सामान्य तकनीकी संकेतकों का उपयोग किया गया है, जो मापदंडों के समायोजन में लचीलापन प्रदान करते हैं।

- यह लगातार बढ़ती प्रवृत्ति की पहचान करने में सक्षम है, जिससे प्रवृत्ति में कुछ अवसरों का लाभ उठाया जा सकता है।

जोखिम विश्लेषण

इस रणनीति में निम्नलिखित जोखिम भी हैं:

- यह नीचे की ओर या साइडवेज़ बाजार की पहचान करने में असमर्थ है, जिससे बड़ी ड्रॉडाउन हो सकती है।

- यह शॉर्ट अवसरों का लाभ नहीं उठा सकती, मंदी की प्रवृत्ति के खिलाफ हेज नहीं कर सकती, और संभावित लाभ के अवसर खो सकती है।

- वॉल्यूम संकेतक उच्च-आवृत्ति डेटा पर प्रभावी नहीं होता, इसके लिए मापदंडों में समायोजन की आवश्यकता हो सकती है।

- जोखिम नियंत्रण के लिए स्टॉप-लॉस का उपयोग किया जा सकता है।

अनुकूलन दिशाएँ

इस रणनीति को निम्नलिखित पहलुओं से अनुकूलित किया जा सकता है:

- शॉर्ट ट्रेडिंग अवसर जोड़ना, द्वि-दिशात्मक (लॉन्ग और शॉर्ट) ट्रेडिंग की अनुमति देना, ताकि मंदी की प्रवृत्ति का लाभ उठाया जा सके।

- अधिक उन्नत संकेतकों जैसे MACD, RSI आदि का उपयोग करके संयोजन रणनीति बनाना, जिससे प्रवृत्ति निर्णय क्षमता में सुधार हो।

- स्टॉप-लॉस तर्क को अनुकूलित करके ड्रॉडाउन जोखिम को कम करना।

- मापदंडों को समायोजित करना, विभिन्न अवधियों के डेटा का परीक्षण करना, और सर्वोत्तम मापदंड संयोजन खोजना।

सारांश

कुल मिलाकर यह रणनीति एक बहुत ही सरल प्रवृत्ति-अनुगामी रणनीति है, जो SMA, EMA और वॉल्यूम संकेतकों के माध्यम से प्रवेश के समय का निर्धारण करती है। इसका लाभ सरलता और आसान कार्यान्वयन है, जो इसे सीखने के लिए उपयुक्त बनाता है, लेकिन यह साइडवेज़ और गिरती प्रवृत्तियों की पहचान नहीं कर सकती, और इसमें कुछ जोखिम हैं। शॉर्ट पोजीशन जोड़ने, संकेतकों को अनुकूलित करने और स्टॉप-लॉस जैसे उपायों से इसे बेहतर बनाया जा सकता है।

- 1