मात्रात्मक संकेतकों पर आधारित बिटकॉइन ट्रेडिंग रणनीति

सारांश

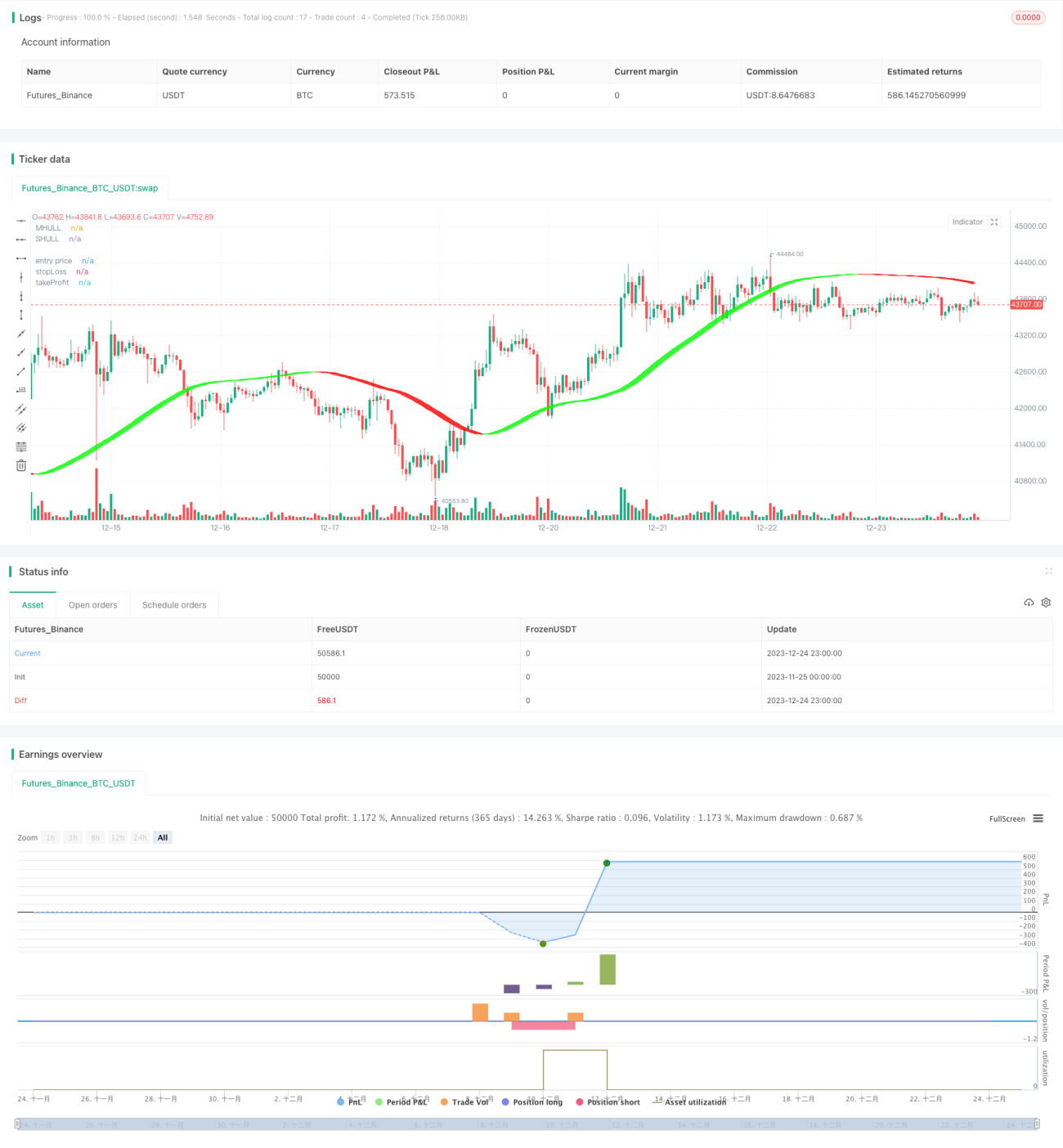

यह रणनीति बिटकॉइन के खरीद-बिक्री के समय का निर्धारण करने और स्वचालित ट्रेडिंग को लागू करने के लिए कई मात्रात्मक संकेतकों का उपयोग करती है। इसमें मुख्य रूप से हल इंडिकेटर (Hull), रिलेटिव स्ट्रेंथ इंडेक्स (RSI), बोलिंगर बैंड्स (BB) और वॉल्यूम ऑसिलेटर (VO) शामिल हैं।

रणनीति का सिद्धांत

-

संशोधित हल मूविंग एवरेज का उपयोग करके बाजार की मुख्य प्रवृत्ति दिशा का निर्धारण किया जाता है, और बोलिंगर बैंड की सहायता से ब्रेकआउट खरीद/बिक्री बिंदुओं का निर्धारण किया जाता है।

-

RSI संकेतक का उपयोग अनुकूली उतार-चढ़ाव सीमा के साथ ओवरबॉट/ओवरसोल्ड क्षेत्रों का निर्धारण करने और ट्रेडिंग सिग्नल उत्पन्न करने के लिए किया जाता है। साथ ही, दो सेट पैरामीटर डुप्लिकेट सिग्नल सत्यापन के रूप में सेट किए जाते हैं।

-

वॉल्यूम ऑसिलेटर खरीद/बिक्री की शक्ति का निर्धारण करता है और झूठे ब्रेकआउट से बचाता है।

-

स्टॉप लॉस/टेक प्रॉफिट अनुपात पैरामीटर के अनुसार पूर्व-निर्धारित स्टॉप लॉस और टेक प्रॉफिट स्तर स्थापित करके जोखिम प्रबंधन किया जाता है।

लाभ विश्लेषण

-

हल कर्व तेजी से प्रवृत्ति परिवर्तन को पकड़ सकता है, और बोलिंगर बैंड की सहायक निर्णय लेने से गलत सिग्नल कम होते हैं।

-

RSI संकेतक के पैरामीटर ऑप्टिमाइज़ेशन और डुप्लिकेट सिग्नल सत्यापन से विश्वसनीयता बढ़ जाती है।

-

वॉल्यूम ऑसिलेटर प्रवृत्ति और संकेतक सिग्नलों के साथ संयोजन कर गलत ट्रेडिंग से बचाता है।

-

पूर्व-निर्धारित स्टॉप लॉस/टेक प्रॉफिट विधि स्वचालित रूप से प्रति ट्रेड लाभ/हानि को नियंत्रित कर सकती है और समग्र जोखिम का प्रभावी नियंत्रण कर सकती है।

जोखिम विश्लेषण

-

पैरामीटर सेटिंग्स का अनुचित होने से ट्रेडिंग आवृत्ति अत्यधिक बढ़ सकती है या सिग्नल प्रभाव खराब हो सकते हैं।

-

अचानक घटनाओं के कारण बाजार में भारी उतार-चढ़ाव होने पर स्टॉप लॉस टूट सकता है, जिससे बड़ा नुकसान हो सकता है।

-

जब ट्रेडिंग इंस्ट्रूमेंट को किसी अन्य क्रिप्टोकरेंसी में बदला जाता है, तो पैरामीटरों का पुनः परीक्षण और ऑप्टिमाइज़ेशन आवश्यक है।

-

वॉल्यूम डेटा गायब होने पर वॉल्यूम ऑसिलेटर काम नहीं करेगा।

अनुकूलन दिशाएँ

-

RSI मापदंडों के अधिक संयोजनों का परीक्षण करके सर्वोत्तम पैरामीटर खोजें।

-

अन्य संकेतकों जैसे MACD, KD आदि को RSI के साथ मिलाकर संकेतों की सटीकता बढ़ाने का प्रयास करें।

-

मशीन लर्निंग का उपयोग करके बाजार की दिशा निर्धारित करने के लिए मॉडल पूर्वानुमान मॉड्यूल जोड़ें।

-

अन्य ट्रेडिंग इंस्ट्रूमेंट्स पर पैरामीटर प्रभाव का परीक्षण करें।

-

स्टॉप लॉस और टेक प्रॉफिट एल्गोरिदम को अनुकूलित करके लाभ को अधिकतम करें।

सारांश

यह रणनीति खरीद-बिक्री के समय का निर्धारण करने के लिए विभिन्न मात्रात्मक तकनीकी संकेतकों का समग्र उपयोग करती है। पैरामीटर ऑप्टिमाइज़ेशन, जोखिम नियंत्रण आदि विधियों के माध्यम से बिटकॉइन की स्वचालित ट्रेडिंग को लागू किया गया है। परिणाम अच्छे हैं, लेकिन बाजार में परिवर्तनों के अनुकूल होने के लिए निरंतर परीक्षण और अनुकूलन की आवश्यकता है। यह निवेशकों के लिए संदर्भ प्रदान कर सकता है और व्यापार निर्णयों में सहायता कर सकता है।

- 1