एकाधिक संकेतकों को एकीकृत करने वाली भावना-संचालित ब्रेकआउट रणनीति

अवलोकन

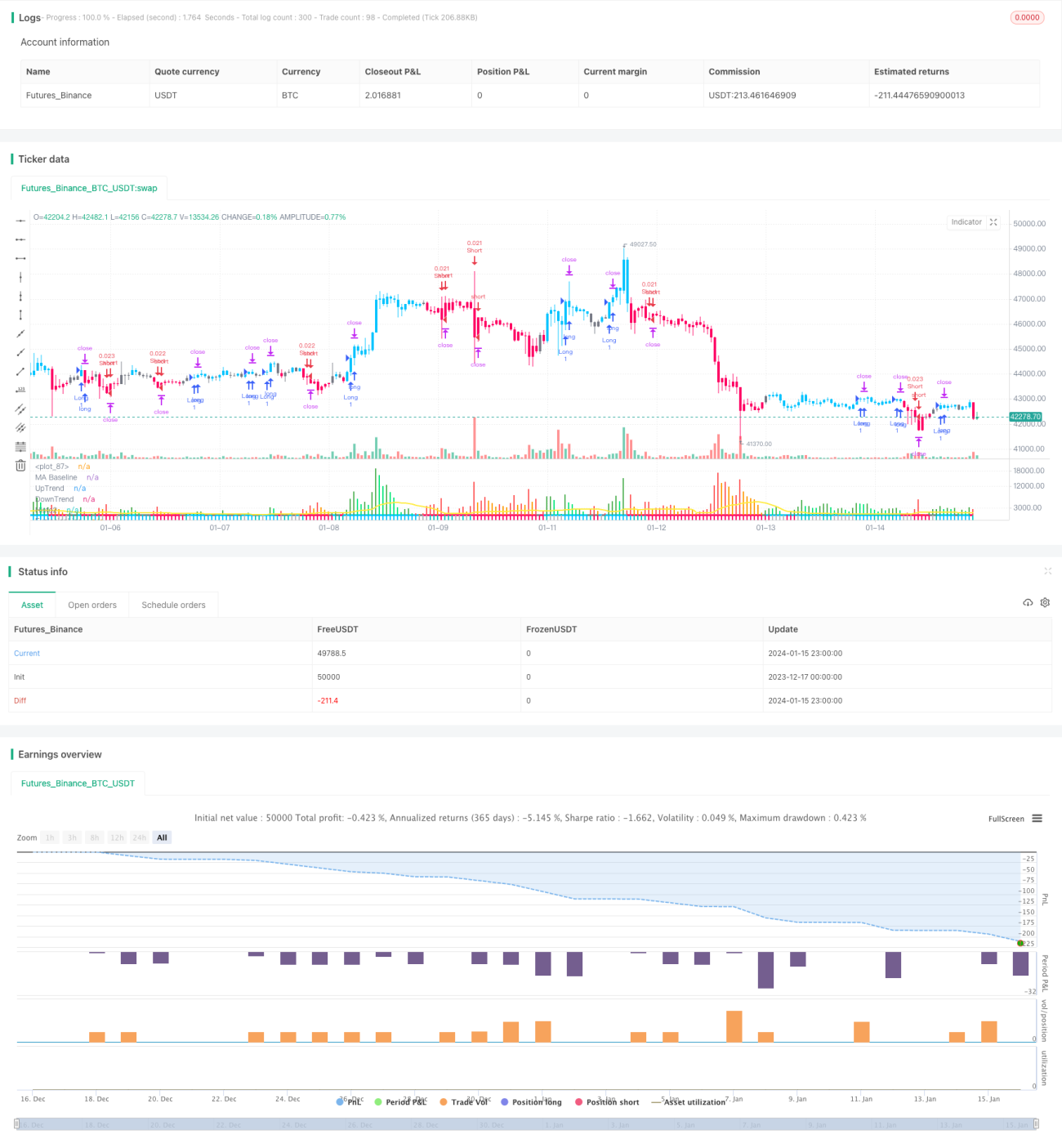

यह रणनीति QQE संशोधित संकेतक, SSL हाइब्रिड संकेतक और वाद्दाह अत्तार विस्फोट संकेतक - तीन भावना-आधारित संकेतकों को मिलाकर व्यापारिक संकेत उत्पन्न करती है। यह एक बहु-संकेतक-संचालित भावना आधारित ब्रेकआउट रणनीति है। यह ब्रेकआउट से पहले बाजार की भावना का आकलन कर सकती है और झूठे ब्रेकआउट से बच सकती है, जो इसे एक बेहतर ब्रेकआउट रणनीति बनाती है।

रणनीति का सिद्धांत

इस रणनीति का मूल तर्क तीन संकेतकों के आधार पर व्यापारिक निर्णय लेता है:

QQE संशोधित संकेतक: यह संकेतक RSI संकेतक को संशोधित करके इसे अधिक संवेदनशील बनाता है, जिससे बाजार की भावना के उच्च और निम्न स्तरों का पता लगाया जा सकता है। इस रणनीति में इसका उपयोग निचले स्तर के उलट (बॉटम रिवर्सल) और ऊपरी स्तर के उलट (टॉप रिवर्सल) संकेतों का पता लगाने के लिए किया जाता है।

SSL हाइब्रिड संकेतक: यह संकेतक कई मूविंग एवरेज के ब्रेकआउट पर विचार करके बाजार के संकेतों का आकलन करता है। इस रणनीति में इसका उपयोग चैनल ब्रेकआउट पैटर्न का पता लगाने के लिए किया जाता है।

वाद्दाह अत्तार विस्फोट संकेतक: यह संकेतक चैनल के अंदर कीमत के विस्फोट बल का आकलन करता है। इस रणनीति में इसका उपयोग यह सुनिश्चित करने के लिए किया जाता है कि ब्रेकआउट के समय पर्याप्त गति हो।

जब QQE संकेतक निचले स्तर के उलट संकेत देता है, SSL संकेतक चैनल के ऊपरी किनारे का ब्रेकआउट दिखाता है, और वाद्दाह अत्तार संकेतक गति विस्फोट का निर्धारण करता है, तब यह रणनीति खरीद निर्णय उत्पन्न करती है। जब तीनों संकेतक एक साथ विपरीत संकेत देते हैं, तो बिक्री निर्णय लिया जाता है।

यह रणनीति स्टॉप लॉस और टेक प्रॉफिट के लिए सटीक निकास बिंदु भी निर्धारित करती है, जिससे लाभ को अधिकतम रूप से लॉक किया जा सके। यह एक उच्च गुणवत्ता वाली भावना-संचालित ब्रेकआउट रणनीति है।

लाभ विश्लेषण

इस रणनीति के निम्नलिखित लाभ हैं:

- यह बाजार की भावना का आकलन करने के लिए कई संकेतकों का उपयोग करके झूठे ब्रेकआउट के जोखिम से बचती है।

- यह एक साथ उलट संकेतक, चैनल संकेतक और गति संकेतक पर विचार करती है, जिससे ब्रेकआउट के समय बाजार की पुष्टि उच्च होती है।

- यह जोखिम को सीमित करने और लाभ को ट्रैक करने तथा लॉक करने के लिए उच्च-सटीकता वाले मूविंग स्टॉप लॉस का उपयोग करती है।

- पैरामीटर व्यापक अनुकूलन परीक्षण के बाद तैयार किए गए हैं, जिससे स्थिरता अच्छी है और मध्यम से दीर्घकालिक होल्डिंग के लिए उपयुक्त है।

- संकेतक मापदंडों को कॉन्फ़िगर करके रणनीति की शैली को स्वतंत्र रूप से समायोजित किया जा सकता है, जिससे यह व्यापक बाजार स्थितियों के अनुकूल हो सकती है।

जोखिम विश्लेषण

इस रणनीति में मुख्य रूप से निम्नलिखित जोखिम हैं:

- जब बाजार लगातार कमजोर रहता है, तो कई छोटे नुकसान वाले ट्रेड उत्पन्न हो सकते हैं।

- इसे एक साथ कई संकेतकों पर निर्भर रहना पड़ता है, जो कुछ बाजारों में असामान्य रूप से विफल हो सकता है।

- QQE जैसे कई संकेतकों में पैरामीटर ओवरफिटिंग का जोखिम होता है, इसलिए सावधानीपूर्वक सेट करना आवश्यक है।

- मूविंग स्टॉप लॉस विशेष बाजार स्थितियों में ठीक से काम नहीं कर सकता है।

उपरोक्त जोखिमों को देखते हुए, संकेतक मापदंडों को अधिक स्थिर बनाने के लिए समायोजित करने और उच्च लाभ दर प्राप्त करने के लिए होल्डिंग अवधि को उचित रूप से बढ़ाने की सिफारिश की जाती है।

अनुकूलन दिशाएँ

इस रणनीति को निम्नलिखित पहलुओं में और अधिक अनुकूलित किया जा सकता है:

- प्रत्येक संकेतक के मापदंडों को समायोजित करके उन्हें अधिक स्थिर या अधिक संवेदनशील बनाया जा सकता है।

- अस्थिरता के आधार पर पोजीशन साइज़िंग ऑप्टिमाइज़ेशन मॉड्यूल जोड़ा जा सकता है।

- मशीन लर्निंग आधारित जोखिम प्रबंधन मॉड्यूल जोड़कर बाजार की स्थिति का वास्तविक समय मूल्यांकन किया जा सकता है।

- संकेतक पैटर्न की भविष्यवाणी करने और निर्णय सटीकता में सुधार करने के लिए डीप लर्निंग मॉडल का उपयोग किया जा सकता है।

- झूठे ब्रेकआउट की संभावना को कम करने के लिए क्रॉस-टाइमफ्रेम विश्लेषण शामिल किया जा सकता है।

सारांश

यह रणनीति कई मुख्यधारा के भावना संकेतकों के लाभों को एकीकृत करके एक कुशल भावना-संचालित ब्रेकआउट रणनीति का निर्माण करती है। यह सफलतापूर्वक कई निम्न-गुणवत्ता वाले ब्रेकआउट से उत्पन्न जोखिमों से बचती है, साथ ही उच्च-सटीकता वाले स्टॉप लॉस सिद्धांत के साथ लाभ को लॉक करती है। यह एक परिपक्व और विश्वसनीय ब्रेकआउट रणनीति संयोजन है जो सीखने और लागू करने योग्य है। मापदंडों के निरंतर अनुकूलन और मॉडल पूर्वानुमान को शामिल करने के साथ, यह रणनीति अधिक स्थिर और निरंतर अतिरिक्त रिटर्न उत्पन्न करने की संभावना रखती है।

- 1