गतिशील ग्रिड व्यापार रणनीति

1

Follow

1802

Followers

सिंहावलोकन

यह रणनीति मूल्य सीमा के भीतर कई समानांतर खरीद और बिक्री ऑर्डर सेट करके ग्रिड ट्रेडिंग को लागू करती है, तथा बाजार की अस्थिरता के अनुसार ग्रिड सीमा और रेखाओं को समायोजित करके लाभ प्राप्त करती है।

रणनीति सिद्धांत

- ग्रिड की ऊपरी और निचली सीमा निर्धारित करें, जिसे मैन्युअल रूप से सेट किया जा सकता है या हाल के समय की उच्च-निम्न कीमतों के आधार पर स्वचालित रूप से गणना की जा सकती है।

- निर्धारित ग्रिड संख्या के अनुसार ग्रिड अंतराल की चौड़ाई की गणना करें।

- संबंधित संख्या में ग्रिड लाइन मूल्यों की एक सरणी उत्पन्न करें।

- जब कीमत किसी ग्रिड लाइन से नीचे होती है, तो उस लाइन के नीचे लॉन्ग पोजीशन खोलें; जब कीमत किसी ग्रिड लाइन से ऊपर होती है, तो उस लाइन के ऊपर शॉर्ट पोजीशन बंद करें।

- ग्रिड की ऊपरी और निचली सीमा, अंतराल की चौड़ाई और ग्रिड लाइन मूल्यों को गतिशील रूप से समायोजित करें ताकि वे बाजार में बदलाव के अनुकूल हो सकें।

लाभ विश्लेषण

- साइडवेज और अस्थिर बाजारों में स्थिर लाभ प्राप्त किया जा सकता है, यह एकतरफा बाजार प्रवृत्तियों से प्रभावित नहीं होता।

- मैन्युअल सेटिंग और स्वचालित गणना दोनों का समर्थन करता है, जिससे अनुकूलन क्षमता अधिक होती है।

- ग्रिड संख्या, ग्रिड चौड़ाई और ऑर्डर आकार को समायोजित करके लाभ को अनुकूलित किया जा सकता है।

- इसमें अंतर्निहित पोजीशन नियंत्रण है, जो जोखिम को नियंत्रित कर सकता है।

- ग्रिड रेंज के गतिशील समायोजन का समर्थन करता है, जिससे रणनीति में मजबूत अनुकूलन क्षमता होती है।

जोखिम विश्लेषण

- महत्वपूर्ण ट्रेंड मूवमेंट की स्थिति में बड़ा नुकसान हो सकता है।

- ग्रिड संख्या और पोजीशन आकार का अनुचित सेटिंग जोखिम को बढ़ा सकता है।

- चरम बाजार स्थितियों में ग्रिड रेंज की स्वचालित गणना विफल हो सकती है।

जोखिम समाधान:

- ग्रिड मापदंडों को अनुकूलित करें और कुल पोजीशन को सख्ती से नियंत्रित करें।

- बड़े बाजार आंदोलनों से पहले रणनीति बंद करें।

- प्रवृत्ति संकेतकों के साथ बाजार की स्थितियों का आकलन करें और आवश्यक होने पर रणनीति बंद करें।

अनुकूलन दिशा

- बाजार विशेषताओं और पूंजी आकार के अनुसार सर्वोत्तम ग्रिड संख्या चुनें।

- ग्रिड स्वचालित गणना मापदंडों को अनुकूलित करने के लिए विभिन्न समय सीमाओं का परीक्षण करें।

- अधिक स्थिर लाभ प्राप्त करने के लिए ऑर्डर आकार गणना विधि को अनुकूलित करें।

- बड़े बाजार आंदोलनों का पता लगाने के लिए अन्य संकेतकों के साथ संयोजन करें और रणनीति बंद करने की शर्तें निर्धारित करें।

सारांश

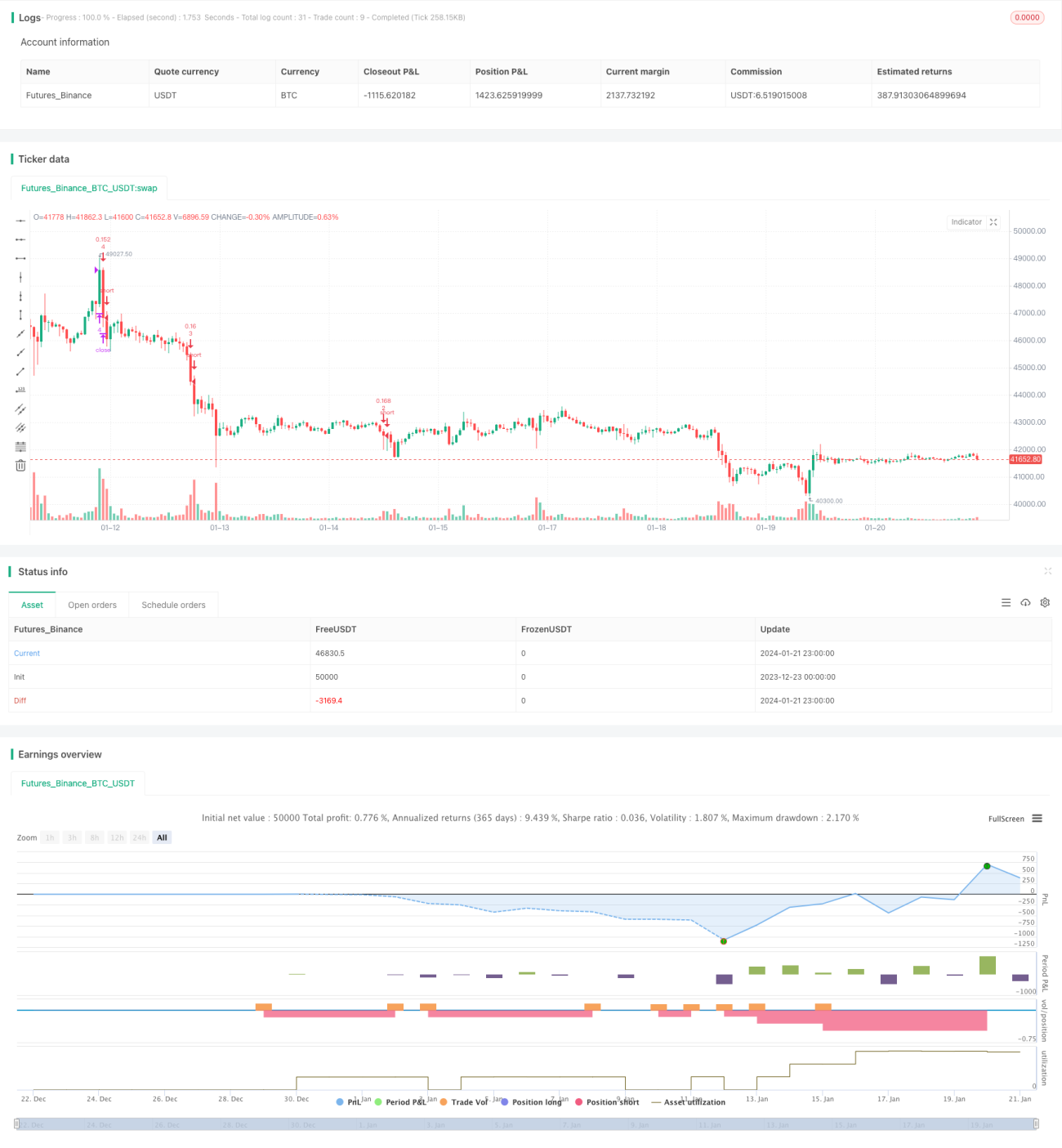

यह गतिशील ग्रिड ट्रेडिंग रणनीति ग्रिड रेंज मापदंडों को गतिशील रूप से समायोजित करके बाजार में बदलावों के अनुकूल होती है, जिससे साइडवेज और अस्थिर बाजारों में लाभ प्राप्त होता है। साथ ही, उचित पोजीशन नियंत्रण से जोखिम को प्रबंधित किया जा सकता है। ग्रिड मापदंडों को अनुकूलित करके और प्रवृत्ति संकेतकों को शामिल करके रणनीति की स्थिरता को और बढ़ाया जा सकता है।

Source

Pine

/*backtest

start: 2023-12-23 00:00:00

end: 2024-01-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("sarasa srinivasa kumar", overlay=true, pyramiding=14, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.1)

i_autoBounds = input(group="Grid Bounds", title="Use Auto Bounds?", defval=true, type=input.bool) // calculate upper and lower bound of the grid automatically? This will theorhetically be less profitable, but will certainly require less attention

i_boundSrc = input(group="Grid Bounds", title="(Auto) Bound Source", defval="Hi & Low", options=["Hi & Low", "Average"]) // should bounds of the auto grid be calculated from recent High & Low, or from a Simple Moving AverageStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1