तीन कैंडलस्टिक रिवर्सल ट्रेंड रणनीति

अवलोकन

थ्री कैंडल रिवर्सल ट्रेंड स्ट्रैटेजी एक अल्पकालिक ट्रेडिंग रणनीति है जो लगातार तीन हरी या लाल मोमबत्तियों की पहचान करती है, और उसके बाद एक एन्गल्फिंग कैंडल के माध्यम से अल्पकालिक प्रवृत्ति के उलट होने का निर्णय लेती है। यह रणनीति कई तकनीकी संकेतकों का उपयोग करके प्रवेश के अवसरों को फ़िल्टर करती है। यह 1:3 के स्टॉप-लॉस और टेक-प्रॉफिट अनुपात पर काम करती है, जो अतिरिक्त रिटर्न प्राप्त करने में सहायक है।

रणनीति का सिद्धांत

इस रणनीति का मुख्य तर्क लगातार तीन हरी या लाल मोमबत्तियों की कैंडलस्टिक पैटर्न की पहचान करना है, जो आमतौर पर अल्पकालिक प्रवृत्ति के उलट होने का संकेत देता है। जब तीन लाल मोमबत्तियों का पता चलता है, तो अगली एन्गल्फिंग हरी मोमबत्ती आने पर लॉन्ग में जाएं; इसके विपरीत, जब तीन हरी मोमबत्तियों का पता चलता है, तो अगली एन्गल्फिंग लाल मोमबत्ती आने पर शॉर्ट में जाएं। इससे अल्पकालिक प्रवृत्ति के उलट होने के अवसर को समय पर पकड़ा जा सकता है।

इसके अतिरिक्त, रणनीति में प्रवेश को फ़िल्टर करने के लिए कई तकनीकी संकेतक शामिल किए गए हैं। दो अलग-अलग पैरामीटर सेटिंग वाली SMA मूविंग एवरेज का उपयोग किया जाता है, और केवल तब प्रवेश पर विचार किया जाता है जब तेज़ रेखा धीमी रेखा को पार करती है। इसके अलावा, रैखिक प्रतिगमन संकेतक के माध्यम से बाजार की साइडवे और ट्रेंडिंग स्थिति का आकलन किया जाता है, और केवल ट्रेंडिंग स्थिति में ही ट्रेड किया जाता है। रणनीति में एक स्विच भी प्रदान किया गया है जो यह तय करता है कि क्या मूविंग एवरेज के गोल्डन क्रॉस होने पर कैंडलस्टिक पैटर्न के साथ प्रवेश किया जाए। इन संकेतकों के समग्र आकलन से अधिकांश शोर को फ़िल्टर किया जा सकता है और प्रवेश की सटीकता में सुधार होता है।

स्टॉप-लॉस और टेक-प्रॉफिट सेटिंग में, रणनीति में जोखिम-इनाम अनुपात कम से कम 1:3 होना आवश्यक है। हाल के N मोमबत्तियों के उतार-चढ़ाव की सीमा के ATR संकेतक की गणना करके, उतार-चढ़ाव के प्रतिशत के साथ स्टॉप-लॉस स्तर निर्धारित किया जाता है, और फिर टेक-प्रॉफिट स्तर की गणना की जाती है। इस तरह एक निश्चित जोखिम उठाते हुए उचित अतिरिक्त रिटर्न प्राप्त किया जा सकता है।

रणनीति के लाभ

थ्री कैंडल रिवर्सल ट्रेंड स्ट्रैटेजी के निम्नलिखित लाभ हैं:

- अल्पकालिक प्रवृत्ति के उलट बिंदु को पहचानना और समय पर अवसर पकड़ना

- विभिन्न संकेतकों द्वारा फ़िल्टरिंग से प्रवेश सटीकता में सुधार

- स्टॉप-लॉस और टेक-प्रॉफिट तंत्र उचित, जोखिम-इनाम अनुपात संतुलित

- सरल पैरामीटर सेटिंग, समझने और संचालन में आसान

रणनीति में जोखिम

इस रणनीति में कुछ जोखिम भी हैं जिन पर ध्यान देने की आवश्यकता है:

- अल्पकालिक उलटाव दीर्घकालिक प्रवृत्ति के उलट का प्रतिनिधित्व नहीं कर सकता, उच्च समय सीमा की प्रवृत्ति पर ध्यान देना आवश्यक है। लंबी अवधि की मूविंग एवरेज को फ़िल्टर के रूप में सेट किया जा सकता है।

- एकल कैंडलस्टिक पैटर्न सिग्नल गलत हो सकता है, अन्य सहायक संकेतों को शामिल करने पर विचार किया जा सकता है।

- स्टॉप-लॉस सेटिंग बहुत आशावादी हो सकती है, स्टॉप-लॉस सीमा को उचित रूप से कड़ा किया जा सकता है।

- बैकटेस्ट डेटा अपर्याप्त हो सकता है, लाइव प्रदर्शन में कुछ अनिश्चितता हो सकती है।

रणनीति में सुधार की दिशाएँ

इस रणनीति को निम्नलिखित दिशाओं में सुधारा जा सकता है:

- मूविंग एवरेज और रैखिक प्रतिगमन मापदंडों को समायोजित करें, प्रवृत्ति स्थिति के आकलन के प्रभाव को अनुकूलित करें

- स्टोचैस्टिक जैसे अन्य सहायक संकेतक जोड़ें, सिग्नल की सटीकता में सुधार करें

- ATR मापदंडों और स्टॉप-लॉस आयाम मापदंडों की सेटिंग को अनुकूलित करें, जोखिम और रिटर्न को संतुलित करें

- ट्रेंड ब्रेकआउट ट्रैकिंग तंत्र जोड़ें, लाभ क्षमता बढ़ाएं

- अधिक कड़ी मनी मैनेजमेंट रणनीति बनाएं, ट्रेड जोखिम को नियंत्रित करें

सारांश

कुल मिलाकर, थ्री कैंडल रिवर्सल ट्रेंड स्ट्रैटेजी एक सरल मूल्य पैटर्न और कई सहायक संकेतकों के निर्णय का उपयोग करके, उचित जोखिम-इनाम संतुलन के आधार पर एक अल्पकालिक ट्रेडिंग रणनीति है। यह कम जटिलता के साथ अच्छा प्रदर्शन प्रदान करती है, और निवेशकों के लिए ध्यान देने और परीक्षण करने योग्य है। इसमें सुधार के लिए कई अवसर भी हैं। पैरामीटर ऑप्टिमाइज़ेशन और नियमों को जोड़कर, यह एक स्थिर और कुशल मात्रात्मक ट्रेडिंग रणनीति के रूप में विकसित हो सकती है।

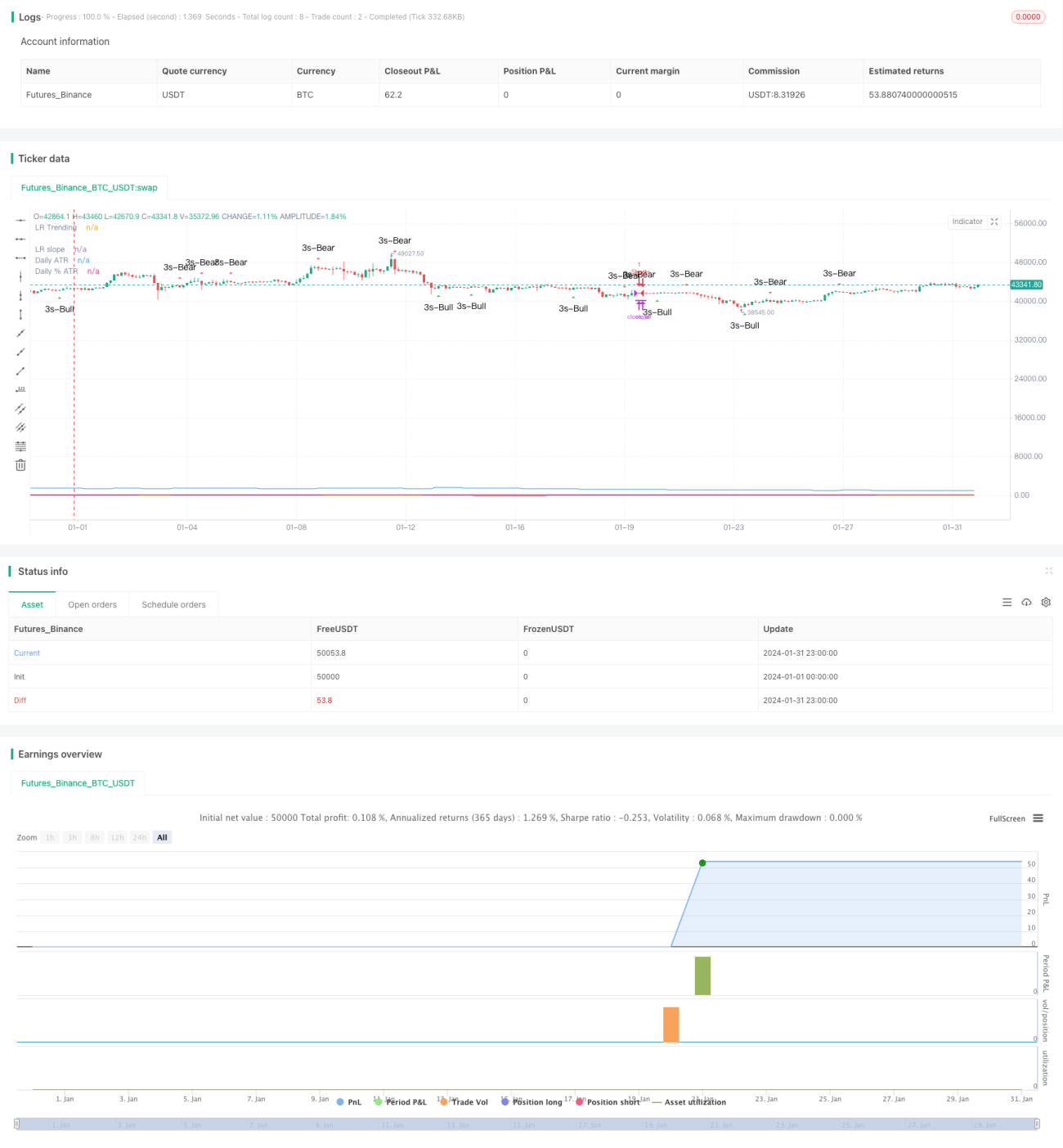

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1