Strategi mengikuti tren yang sekuat batu

Ringkasan

Strategi ini didasarkan pada kombinasi SSL Hybrid Channel, QQE Modified, dan indikator Vada Ata Blast, mewujudkan strategi pelacakan tren yang kokoh. Strategi ini dapat menghasilkan keuntungan yang stabil pada mata uang kripto besar seperti BTC dan ETH, cocok untuk operasi jangka menengah dan panjang.

Prinsip Strategi

Logika Masuk

Kondisi masuk posisi long:

- Harga penutupan di atas garis dasar SSL Hybrid Channel

- Warna indikator QQE Modified berubah menjadi biru

- Indikator Vada Ata Blast berwarna hijau

Kondisi masuk posisi short:

- Harga penutupan di bawah garis dasar SSL Hybrid Channel

- Warna indikator QQE Modified berubah menjadi merah

- Indikator Vada Ata Blast berwarna merah

Logika Keluar

Kondisi keluar posisi long:

- Warna indikator QQE Modified berubah menjadi merah

Kondisi keluar posisi short:

- Warna indikator QQE Modified berubah menjadi biru

Analisis Keunggulan

Strategi ini memiliki keunggulan sebagai berikut:

- Kombinasi tiga indikator memastikan akurasi dan stabilitas sinyal trading.

- Garis dasar SSL Channel dan indikator QQE Modified secara efektif dapat menangkap arah tren.

- Indikator Vada Ata Blast selanjutnya memverifikasi sinyal trading, menghindari false breakout.

- Struktur kode jelas, mudah dipahami dan dimodifikasi.

- Dilengkapi dengan mekanisme stop loss, take profit, dan manajemen risiko yang lengkap, dapat mengendalikan risiko secara efektif.

- Pada jangka waktu yang lebih panjang (seperti 1 jam, 4 jam), kinerja backtesting sangat baik.

Analisis Risiko

Strategi ini juga memiliki risiko sebagai berikut:

- Pada jangka waktu pendek (seperti 5 menit), hasil backtesting kurang baik.

- Di pasar yang berfluktuasi besar, stop loss mungkin sering terpicu.

- Pada beberapa mata uang kripto tertentu, hasil backtesting mungkin tidak memuaskan.

Untuk mengatasi risiko ini, dapat diambil langkah-langkah berikut:

- Hanya digunakan untuk operasi jangka menengah dan panjang, tidak cocok untuk jangka pendek.

- Longgarkan rentang stop loss secara tepat, hindari stop loss yang terlalu sering.

- Uji lebih banyak instrumen, temukan mata uang kripto yang sesuai dengan karakteristik strategi ini.

Arah Optimasi

Strategi ini juga dapat dioptimalkan dari aspek-aspek berikut:

- Uji pengaturan parameter yang berbeda, temukan kombinasi terbaik.

- Tambahkan elemen pembelajaran mesin, membuat strategi lebih adaptif.

- Gabungkan indikator sentimen dan faktor lainnya untuk meningkatkan stabilitas sistem secara keseluruhan.

- Pelajari karakteristik industri, sesuaikan parameter, agar strategi berlaku untuk industri tertentu.

- Tambahkan modul trading algoritmik, gunakan order terprogram, tingkatkan imbal hasil.

Kesimpulan

Secara keseluruhan, strategi ini layak direkomendasikan. Strategi ini stabil, mudah dipahami, dan dilengkapi dengan sistem manajemen risiko yang lengkap. Pada instrumen dan jangka waktu yang tepat, dapat memperoleh keuntungan yang baik. Melalui optimasi dan penyesuaian yang berkelanjutan, strategi ini dapat menjadi alat investasi kuantitatif yang efisien.

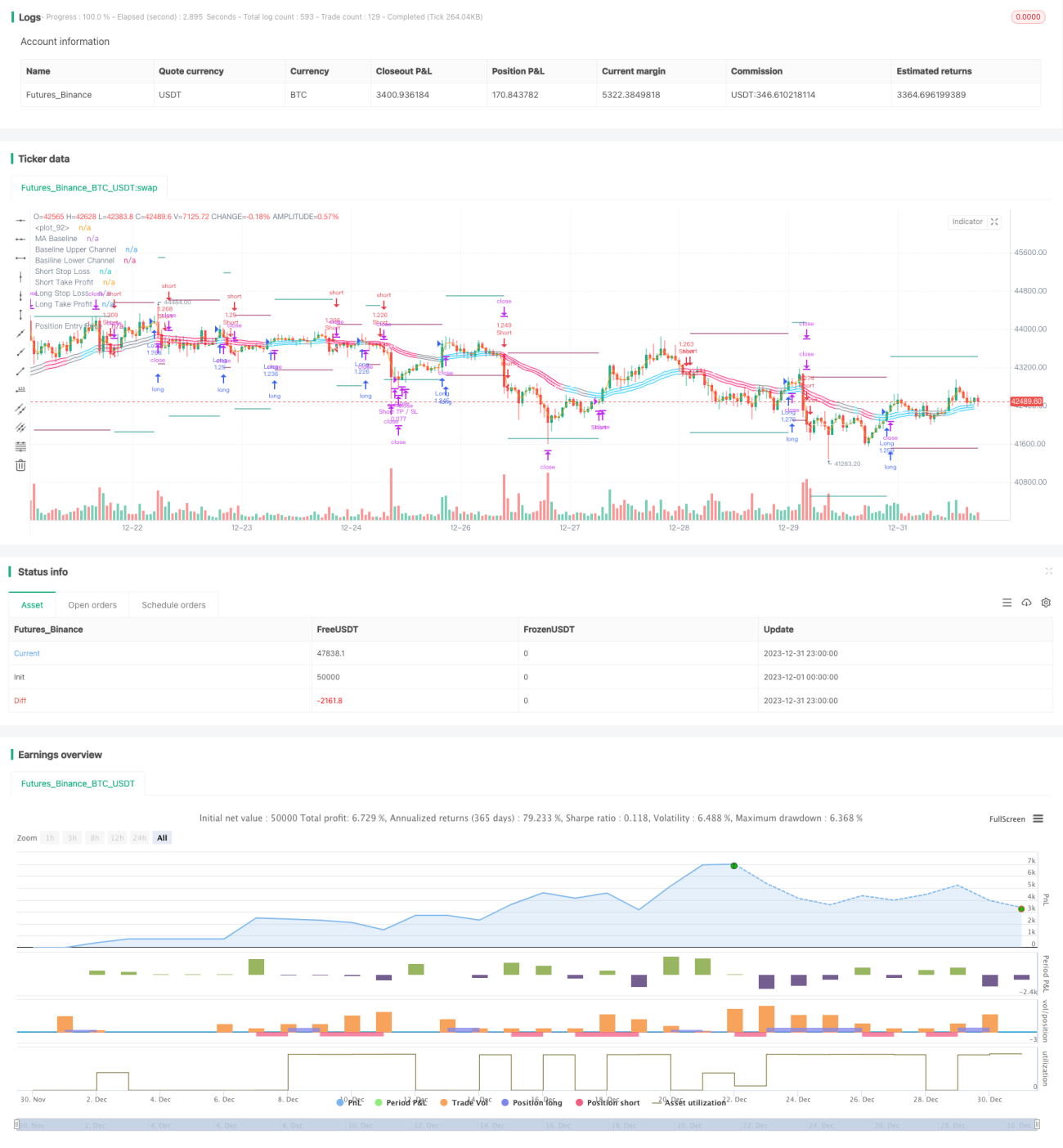

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1