Strategi Trading Indikator MACD Multi-Period

Gambaran Umum

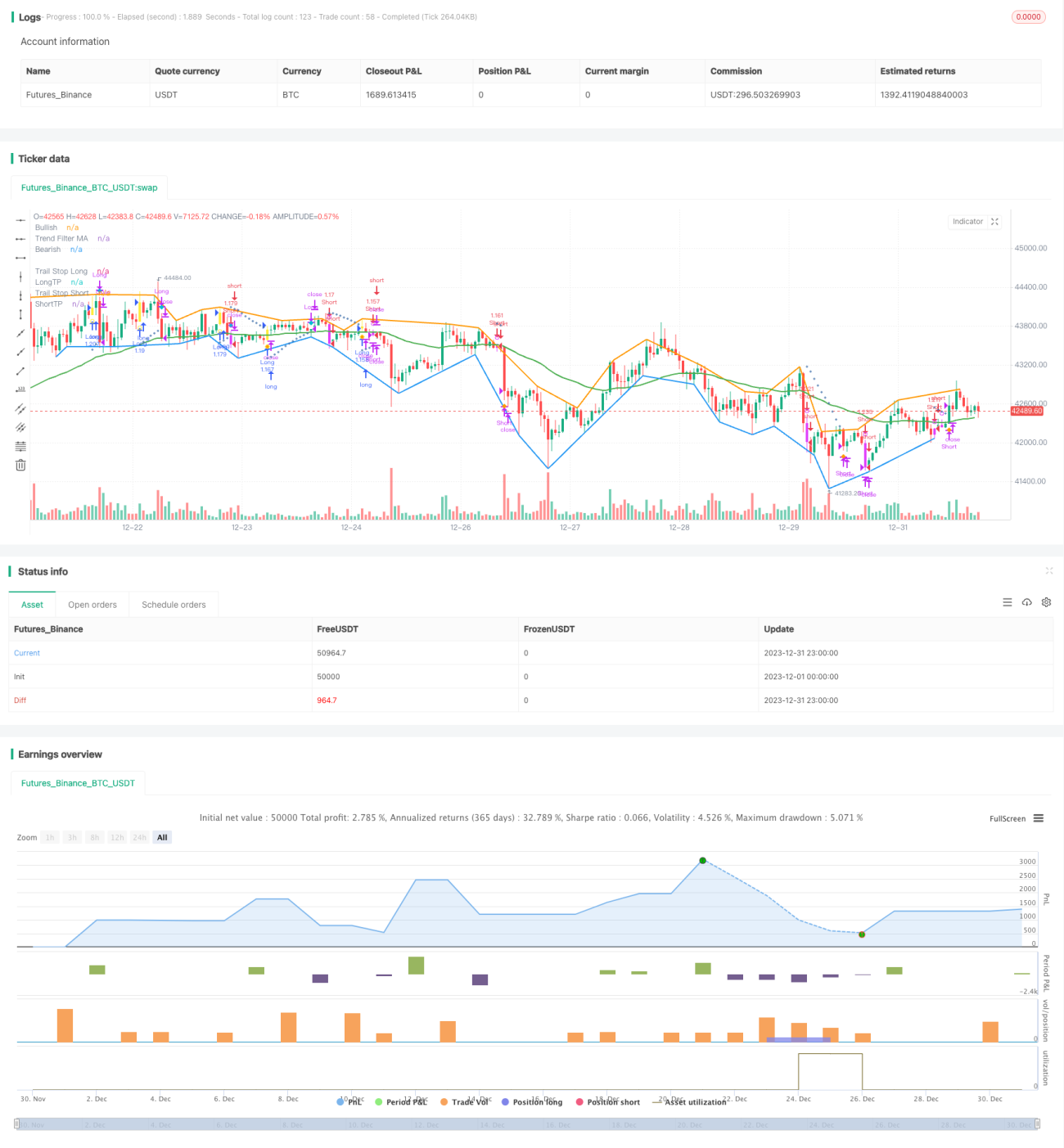

Strategi ini didasarkan pada indikator MACD klasik, sekaligus menggabungkan berbagai bantuan penilaian seperti indikator penentu tren, metode stop loss, dan metode take profit, membentuk strategi trading mengikuti tren yang relatif lengkap. Strategi ini dapat digunakan untuk mata uang kripto, forex, dan perdagangan saham.

Prinsip Strategi

-

Penilaian Indikator MACD

- Selisih antara EMA periode FASTLENGTH dan EMA periode SLOWLENGTH membentuk histogram MACD

- EMA periode MACDLENGTH memperhalus histogram MACD membentuk garis MACD

- Histogram MACD menembus sumbu 0 menghasilkan sinyal beli/jual

-

Penentuan Tren

- ADX: Indikator Rata-rata Arah, menentukan apakah ada tren

- MA: Rata-rata Bergerak, harga di atas/bawah MA membentuk tren

- SAR: Parabolic SAR, pergerakan SAR di atas/bawah harga menentukan tren

-

Metode Stop Loss

- Stop Loss Persentase ATR: Mengatur stop loss persentase berdasarkan faktor ATR

- Stop Loss SAR: Parabolic SAR digunakan sebagai stop loss setelah masuk posisi

-

Metode Take Profit

- Jarak Take Profit Tetap ATR: Mengatur jarak take profit tetap berdasarkan faktor ATR

- Take Profit Persentase: Mengatur jarak take profit dalam persentase

-

Stop Loss Waktu

- Dapat diatur untuk stop loss setelah sejumlah bar tertentu

Analisis Keunggulan

-

Berbagai Bantuan Penilaian

- Menggabungkan penentuan tren dan support/resistance, dapat mengurangi sinyal palsu

- Stop loss ATR/SAR, mengontrol risiko dengan lebih menyeluruh

-

Konfigurasi Fleksibel

- Dapat memilih apakah akan menggunakan filter tren

- Dapat memilih stop loss ATR atau SAR

- Dapat memilih take profit ATR atau standar

- Parameter dapat dikonfigurasi secara fleksibel

-

Menyediakan Analisis Divergensi

- Menampilkan divergensi positif/negatif historis

- Menyediakan petunjuk teks

-

Memudahkan Optimasi dan Penyesuaian

- Strategi ini memiliki banyak parameter yang dapat dikonfigurasi

- Dapat dengan mudah menguji berbagai kombinasi variabel

Analisis Risiko

-

Parameter yang Tidak Tepat Dapat Memperbesar Kerugian

- Pengaturan parameter ATR dan SAR yang tidak tepat dapat menyebabkan stop loss terlalu dini

- Rasio take profit yang terlalu besar dapat menyebabkan take profit terlalu dini

-

Risiko Kegagalan Penentuan Tren

- Parameter indikator tren yang tidak tepat dapat menyebabkan kesalahan penentuan

- Peristiwa tak terduga dapat mempengaruhi kegagalan penentuan tren

-

Risiko Stop Loss Waktu

- Mengatur stop loss waktu tetap memiliki risiko kerugian

Arah Optimasi

- Menyesuaikan parameter ATR dan SAR untuk membuat stop loss lebih halus

- Menguji periode MA yang berbeda untuk mengoptimalkan penentuan tren

- Menguji penyesuaian rasio take profit untuk mengoptimalkan tingkat pengembalian

- Menggabungkan indikator volatilitas untuk mengoptimalkan parameter

Kesimpulan

Strategi ini mempertimbangkan berbagai sudut seperti penentuan tren, stop loss/take profit, identifikasi divergensi, dll., membentuk strategi trading mata uang kripto yang relatif komprehensif. Ini menggabungkan keunggulan indikator MACD, menambahkan filter tren untuk menghindari kesalahan trading; menambahkan stop loss ATR/SAR untuk mengontrol risiko dengan lebih baik; identifikasi divergensi memberikan referensi tambahan. Berbagai parameter yang dapat dikonfigurasi memudahkan pengujian dan optimasi. Secara keseluruhan, strategi ini dapat menjadi contoh yang baik untuk penelitian strategi mata uang kripto.

- 1