Strategi Pengikut Tren Berbasis Multi-Indikator

Ikhtisar

Strategi ini mengidentifikasi tren dengan menggabungkan beberapa indikator dan menetapkan trailing stop loss untuk mengunci keuntungan. Terutama menggunakan Bollinger Bands, RSI, ADX, dan indikator lainnya untuk menentukan waktu masuk, serta ATR dan Bollinger Bands untuk stop loss.

Prinsip Strategi

Indikator utama strategi adalah Bollinger Bands, RSI, dan ADX. Ketika harga mendekati pita bawah Bollinger Bands dan RSI di bawah 30, kondisi dianggap oversold dan dilakukan long (beli). Ketika harga mendekati pita atas Bollinger Bands dan RSI di atas 70, kondisi dianggap overbought dan dilakukan short (jual). Selain itu, jika ADX di atas 25, maka dianggap tren telah terbentuk, sehingga sinyal long/short menjadi lebih efektif.

Setelah posisi dibuka, strategi menggunakan indikator ATR dan batas atas/bawah Bollinger Bands untuk stop loss. Secara rinci, ATR digunakan untuk menentukan jarak maksimum stop loss; ketika harga menyentuh titik stop loss maksimum, maka posisi ditutup. Batas atas/bawah Bollinger Bands digunakan untuk menetapkan titik trailing stop loss, yang diperbarui secara real-time sesuai pergerakan harga.

Analisis Keunggulan

Strategi ini menggabungkan beberapa indikator untuk mengidentifikasi tren secara efektif, serta menggunakan mekanisme stop loss untuk mengunci keuntungan dan mengurangi risiko kerugian. Ini termasuk strategi yang cukup stabil. Keunggulan spesifiknya adalah:

- Menggunakan Bollinger Bands untuk mengidentifikasi kondisi overbought/oversold, sehingga dapat mendeteksi peluang reversal.

- Menggabungkan indikator RSI dapat meningkatkan akurasi sinyal.

- Indikator ADX memastikan arah trading sesuai dengan tren yang terbentuk.

- Trailing stop loss dengan ATR dan Bollinger Bands dapat memaksimalkan penguncian keuntungan.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

- Dengan banyak indikator, pengaturan parameter mudah mengalami overfitting.

- Ketika rentang Bollinger Bands terlalu lebar, sinyal overbought/oversold menjadi kurang efektif.

- Trailing stop loss yang tidak tepat dapat menyebabkan kerugian membesar.

Untuk mengatasi risiko ini, langkah-langkah berikut dapat diambil:

- Mengoptimalkan parameter dengan berbagai kombinasi untuk mencegah overfitting.

- Menyesuaikan parameter Bollinger Bands sesuai dengan volatilitas pasar.

- Menguji parameter jarak stop loss untuk memastikan dapat menahan fluktuasi normal.

Arah Optimasi

Strategi ini juga dapat dioptimalkan dari beberapa arah berikut:

- Menambahkan pengaturan ukuran posisi berdasarkan pengali stop loss.

- Menambahkan modul manajemen uang untuk mengontrol secara ketat jumlah kerugian per transaksi.

- Menguji indikator stop loss lainnya seperti DMI, Envelope, dll.

- Menambahkan model machine learning untuk memperkirakan probabilitas tren guna meningkatkan performa.

Kesimpulan

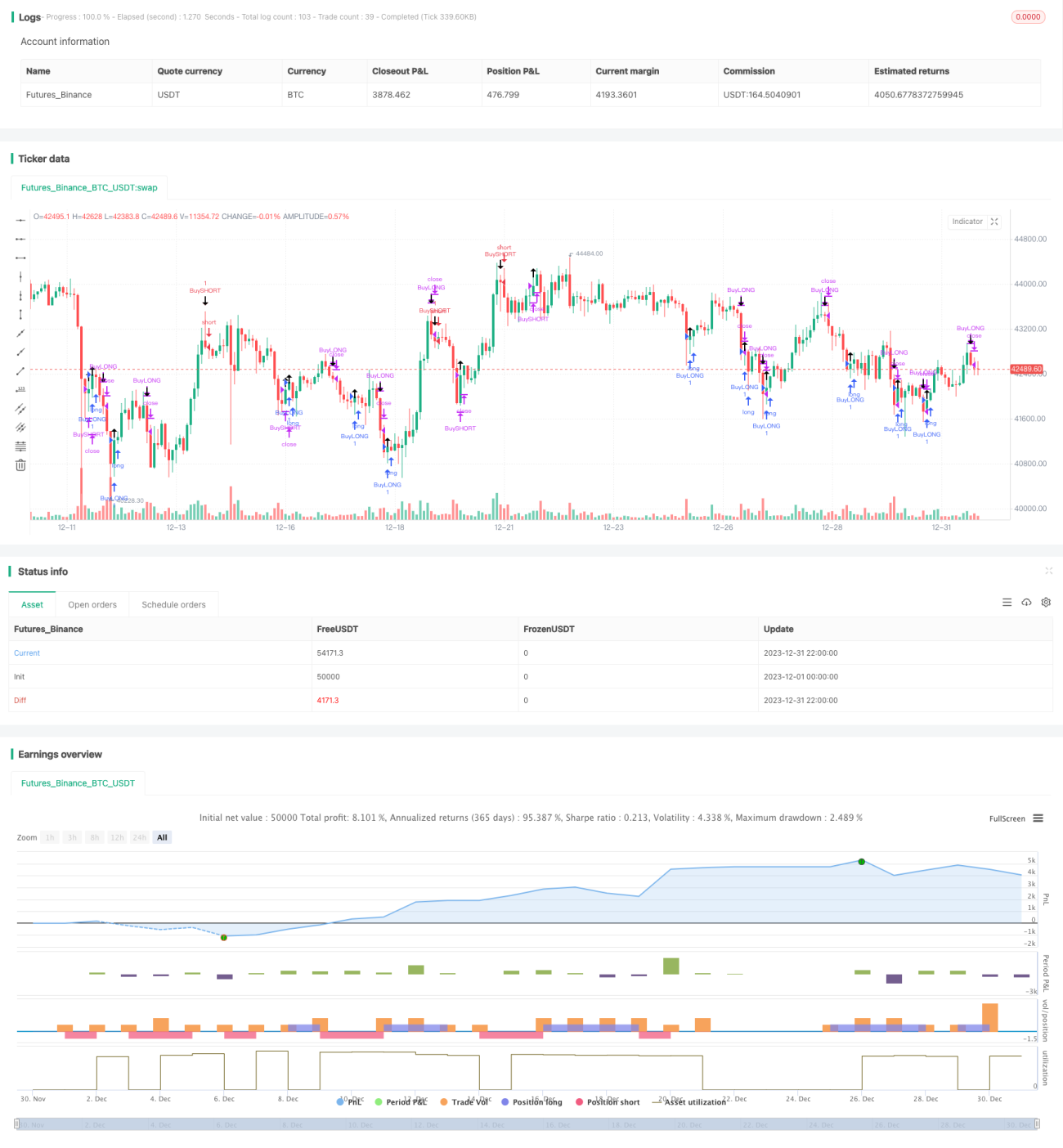

Secara keseluruhan, strategi ini adalah strategi mengikuti tren yang relatif stabil. Dengan menggunakan beberapa indikator untuk menentukan arah tren dan menerapkan langkah-langkah stop loss untuk mengendalikan risiko, strategi ini dapat menghasilkan tingkat pengembalian yang cukup baik. Kami juga telah mengusulkan beberapa arah optimasi; jika dioptimalkan lebih lanjut, hasil yang lebih baik dapat dicapai.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1