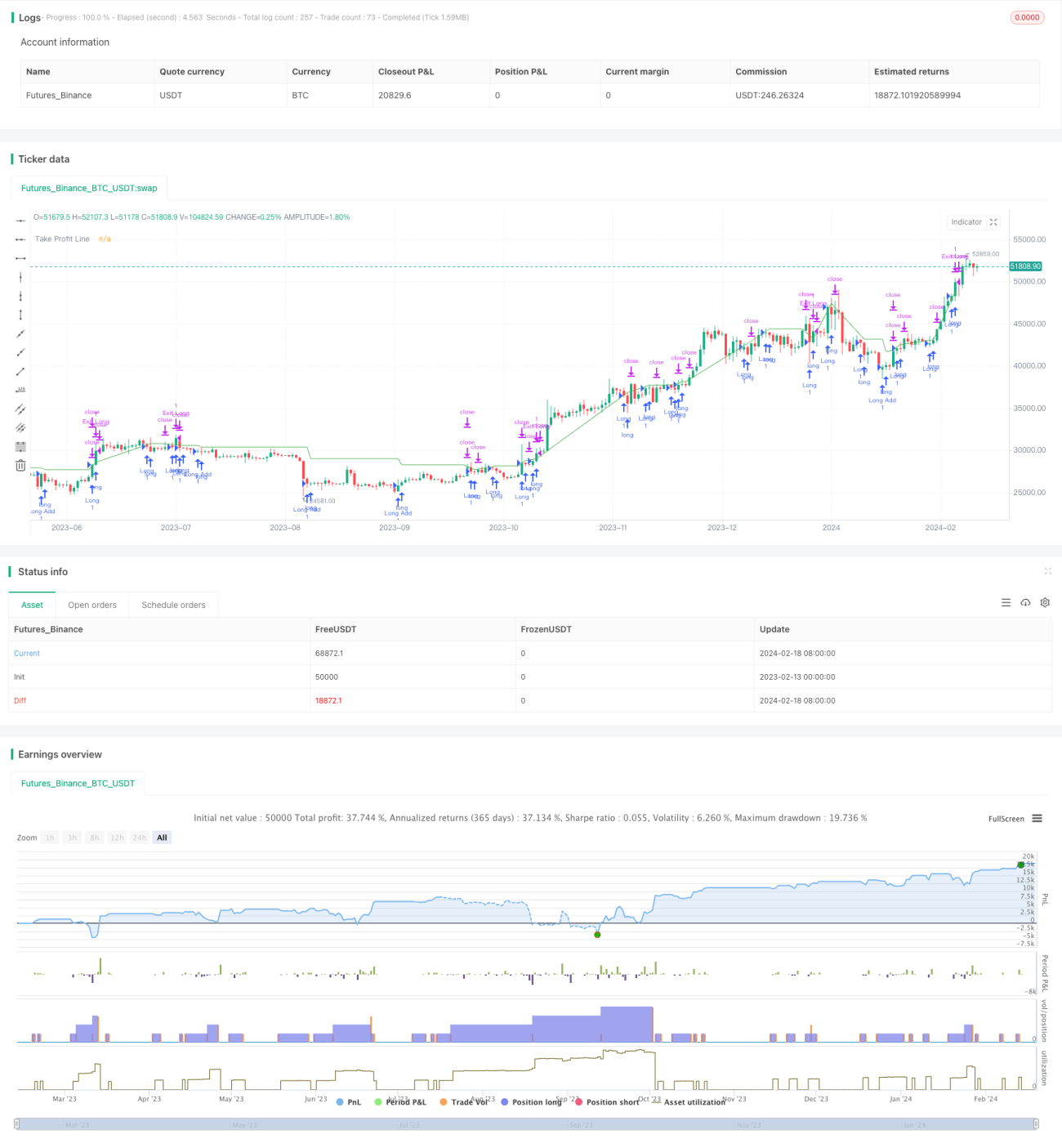

Strategi perdagangan kuantitatif berdasarkan beberapa faktor

Ikhtisar

Strategi ini menggunakan beberapa indikator teknikal seperti RSI, MACD, OBV, CCI, CMF, MFI, dan VWMACD secara terpadu untuk mendeteksi divergensi antara harga dan volume, guna mengidentifikasi potensi peluang masuk. Strategi ini juga menggabungkan indikator deteksi user dip, yang menghasilkan sinyal perdagangan ketika kondisi volatilitas tinggi dan kedalaman atau VFI terpenuhi. Strategi ini hanya mengambil posisi long (membeli), dan membangun posisi secara bertahap dengan trailing stop.

Prinsip Strategi

-

Menghitung indikator RSI, MACD, OBV, CCI, CMF, MFI, dan VWMACD, lalu mendeteksi divergensi antara masing-masing indikator dengan harga historis menggunakan metode regresi linear adaptif. Ketika indikator mencapai titik terendah baru namun harga tidak mengikuti penurunan tersebut, sinyal beli akan dikeluarkan.

-

Berdasarkan ambang volatilitas dan ambang persentase kedalaman yang diinput oleh pengguna, digabungkan dengan filter indikator VFI, sinyal akan dikeluarkan pada candle yang memenuhi kondisi volatilitas tinggi dan uji kedalaman.

-

Setelah posisi long awal diambil, jika harga turun di bawah persentase tertentu dari harga long terakhir (dapat dikonfigurasi), maka posisi long akan ditambah kembali.

-

Menggunakan trailing stop, posisi akan ditutup ketika mencapai rasio take profit yang dikonfigurasi.

Analisis Kelebihan

-

Kombinasi multi-faktor, menggabungkan indikator harga dan volume untuk meningkatkan keandalan sinyal.

-

Metode regresi linear adaptif mendeteksi divergensi, menghindari subjektivitas penilaian manual.

-

Menggabungkan indikator volatilitas dan kedalaman/VFI membantu menemukan peluang pembalikan.

-

Penambahan posisi secara bertahap saat penurunan harga memanfaatkan koreksi, dan trailing take profit membantu mengunci keuntungan.

Analisis Risiko

-

Penilaian kombinasi multi-faktor cukup kompleks, efektivitas optimasi parameter dan deteksi divergensi dapat mempengaruhi kinerja aktual.

-

Risiko posisi satu arah (long saja) tinggi, jika analisis salah dapat menyebabkan kerugian besar.

-

Dalam mode penambahan posisi berulang, kerugian juga akan membesar, perlu pengaturan posisi yang hati-hati.

-

Perlu memperhatikan pengaruh biaya transaksi terhadap keuntungan aktual.

Arah Optimasi

-

Menguji berbagai kombinasi parameter dan efek indikator, memilih konfigurasi terbaik.

-

Menambahkan strategi stop loss untuk mengendalikan kerugian per transaksi dan maksimal.

-

Mempertimbangkan peluang perdagangan dua arah untuk menyebarkan risiko.

-

Menggabungkan metode pembelajaran mesin untuk mengoptimalkan parameter secara otomatis.

Kesimpulan

Strategi ini menggabungkan berbagai indikator teknikal untuk mengidentifikasi titik masuk, sekaligus menggunakan kondisi yang ditentukan pengguna dan indikator VFI untuk menyaring sinyal palsu. Strategi ini terus menambah posisi saat harga koreksi (averaging up), berguna untuk menangkap peluang dalam tren. Namun juga menghadapi risiko kesalahan analisis dan posisi satu arah, perlu optimasi parameter indikator, strategi stop loss, dll. untuk mengurangi risiko dan meningkatkan potensi keuntungan.

- 1