Pelacak Paus

VS, ATR, MA200, HTF

Ini bukan strategi breakout biasa, ini adalah pelacak paus yang khusus menyergap pergerakan modal besar

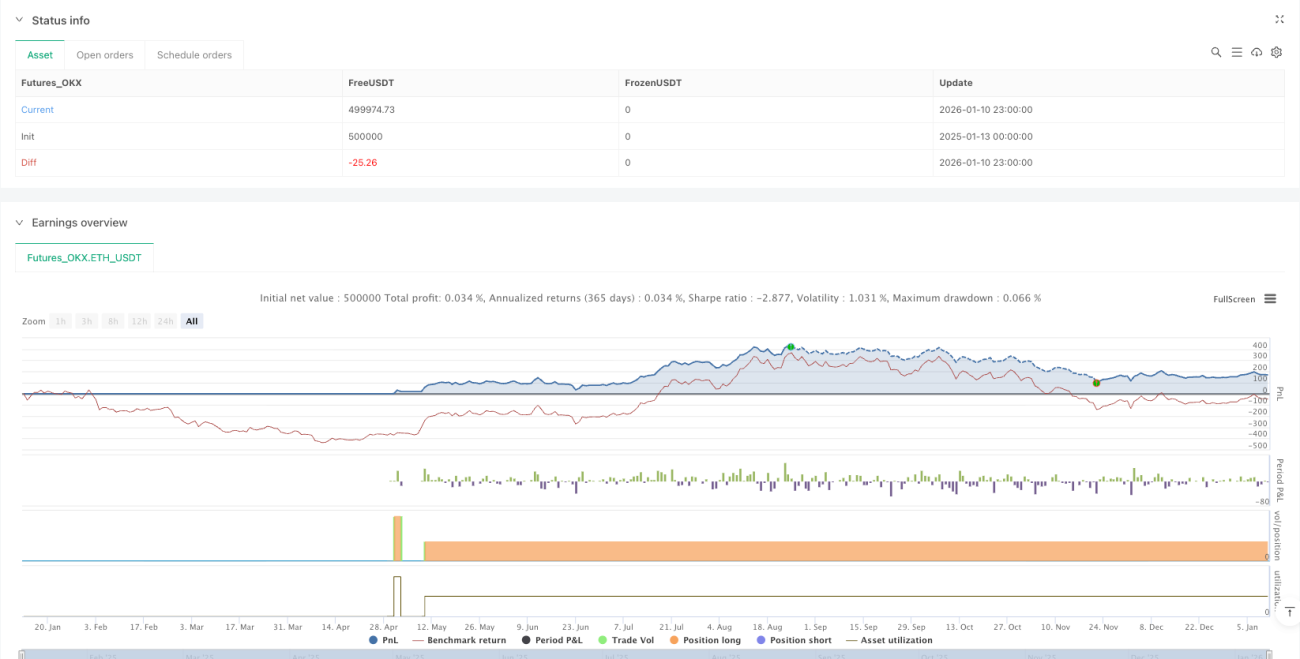

Data backtesting menunjukkan: ketika sinyal Volume Spike (VS) muncul di pasar, dikombinasikan dengan filter MA berganda, tingkat kemenangan secara signifikan lebih baik daripada strategi breakout tradisional. Logika intinya sederhana dan kasar — modal besar pasti meninggalkan jejak saat masuk, yang perlu kita lakukan adalah mengikuti langkah-langkah "paus" ini.

Deteksi VS 21 periode + faktor pembesaran 2,3x, menangkap sinyal pergerakan anomali yang sebenarnya

Strategi tradisional melihat harga, sistem ini melihat anomali volume. Hitung rata-rata volatilitas setelah membuang 2 nilai ekstrem dalam 21 periode, sinyal dipicu ketika volatilitas candle saat ini melebihi 2,3 kali rata-rata dan mencapai lebih dari 0,7% dari harga penutupan. Yang lebih penting, harga penutupan harus berada di posisi 65% ke atas dari candle tersebut, memastikan ini adalah volume melonjak yang didominasi oleh para pembeli.

Data berbicara: Mekanisme deteksi VS ini menyaring lebih dari 90% breakout palsu, hanya menangkap pergerakan yang benar-benar melibatkan modal besar.

Filter MA200 empat lapis, menolak untuk melakukan long di pasar bearish

Tidak semua volume melonjak layak dikejar, tren pasar menentukan segalanya. Strategi ini mengatur empat lapis pertahanan MA200:

- Harga saat ini harus di atas MA200

- MA200 harus dalam tren naik (kemiringan 20 periode positif)

- MA200 level 4 jam juga mengonfirmasi bullish

- Titik masuk tidak boleh lebih dari 6% dari MA200

Apa artinya ini? Anda tidak akan pernah terjebak dalam tren penurunan yang jelas karena sistem tidak akan memberikan sinyal.

Stop loss 2,7x ATR + trailing dinamis, kontrol risiko lebih ketat dari yang Anda bayangkan

Setiap risiko perdagangan ditetapkan pada $100 (dapat disesuaikan), ukuran posisi dihitung secara dinamis melalui ATR. Stop loss awal adalah ATR 14 periode dikalikan 2,7 kali, parameter ini telah dioptimalkan melalui backtesting ekstensif, sehingga dapat menghindari stop loss karena volatilitas normal dan keluar tepat waktu saat terjadi pembalikan nyata.

Inovasi kunci: Setiap kali sinyal VS baru muncul, harga stop loss secara otomatis naik ke titik terendah terbaru, mengunci keuntungan yang ada sambil memberi ruang bagi tren.

Logika pyramiding, biarkan keuntungan berlari lebih jauh

Sinyal VS pertama membuka posisi, sinyal VS kedua menambah posisi, setelah sinyal VS ketiga, stop loss naik ke harga pokok. Ini bukan penambahan posisi buta, melainkan penilaian logis berdasarkan pergerakan anomali pasar yang berkelanjutan — aliran masuk modal besar yang berurutan biasanya menandakan pergerakan yang lebih besar.

Dukungan data: Backtesting historis menunjukkan bahwa pergerakan dengan lebih dari 3 sinyal VS berurutan memiliki kenaikan rata-rata 2,8 kali lipat dari sinyal VS tunggal.

Mekanisme take profit bertahap, keseimbangan sempurna antara mengamankan keuntungan dan mengikuti tren

Ketika sinyal VS ke-4 terpicu, secara otomatis take profit 33% posisi; pada sinyal VS ke-5, take profit 50% dari sisa posisi. Logika di balik desain ini adalah: sinyal VS awal mengonfirmasi tren, sinyal VS akhir sering mendekati area puncak.

Efek praktis: Menghindari situasi "naik turun lift", sambil mempertahankan sebagian posisi untuk menangkap kemungkinan pergerakan super.

Mekanisme Pay-Self, setelah floating profit 2%, secara otomatis melindungi 0,15% keuntungan

Ini adalah inti dari manajemen risiko — ketika floating profit mencapai 2%, harga stop loss secara otomatis naik ke 0,15% di atas harga pokok. Tampaknya konservatif, tetapi sebenarnya ini memberi ruang yang cukup untuk tren besar sambil memastikan stabilitas jangka panjang strategi.

Mengapa pemicu 2%? Karena data backtesting menunjukkan bahwa perdagangan yang mencapai floating profit 2% memiliki probabilitas akhir untung lebih dari 78%.

Pasar yang cocok: BTC timeframe 1 jam, performa terbaik di lingkungan pasar bullish

Strategi ini dioptimalkan khusus untuk grafik 1 jam BTC, berkinerja luar biasa di pasar yang bertren. Perlu dicatat bahwa di pasar sideways, sinyal VS sering muncul tetapi amplitudonya terbatas, yang dapat menyebabkan stop loss kecil beruntun.

Peringatan risiko: Backtesting historis tidak menjamin hasil masa depan, strategi memiliki risiko kerugian beruntun. Disarankan untuk mengontrol risiko setiap perdagangan dengan ketat, jangan melebihi 1-2% dari akun. Ketika kondisi pasar berubah, performa strategi mungkin berbeda secara signifikan.

Intinya: Ini adalah sistem pengikut tren yang lengkap, bukan alat spekulasi jangka pendek

Jika Anda mengharapkan sinyal setiap hari, strategi ini tidak cocok untuk Anda. Jika Anda ingin menangkap pergerakan tren yang sebenarnya, bersedia menunggu peluang masuk berkualitas tinggi, maka pelacak paus ini layak dipelajari lebih dalam. Ingat, hanya sedikit yang menghasilkan uang di pasar; mengikuti modal besar lebih andal daripada mengikuti emosi.

- 1