SARに基づくトレンドフォロー型クオンツ戦略

概要

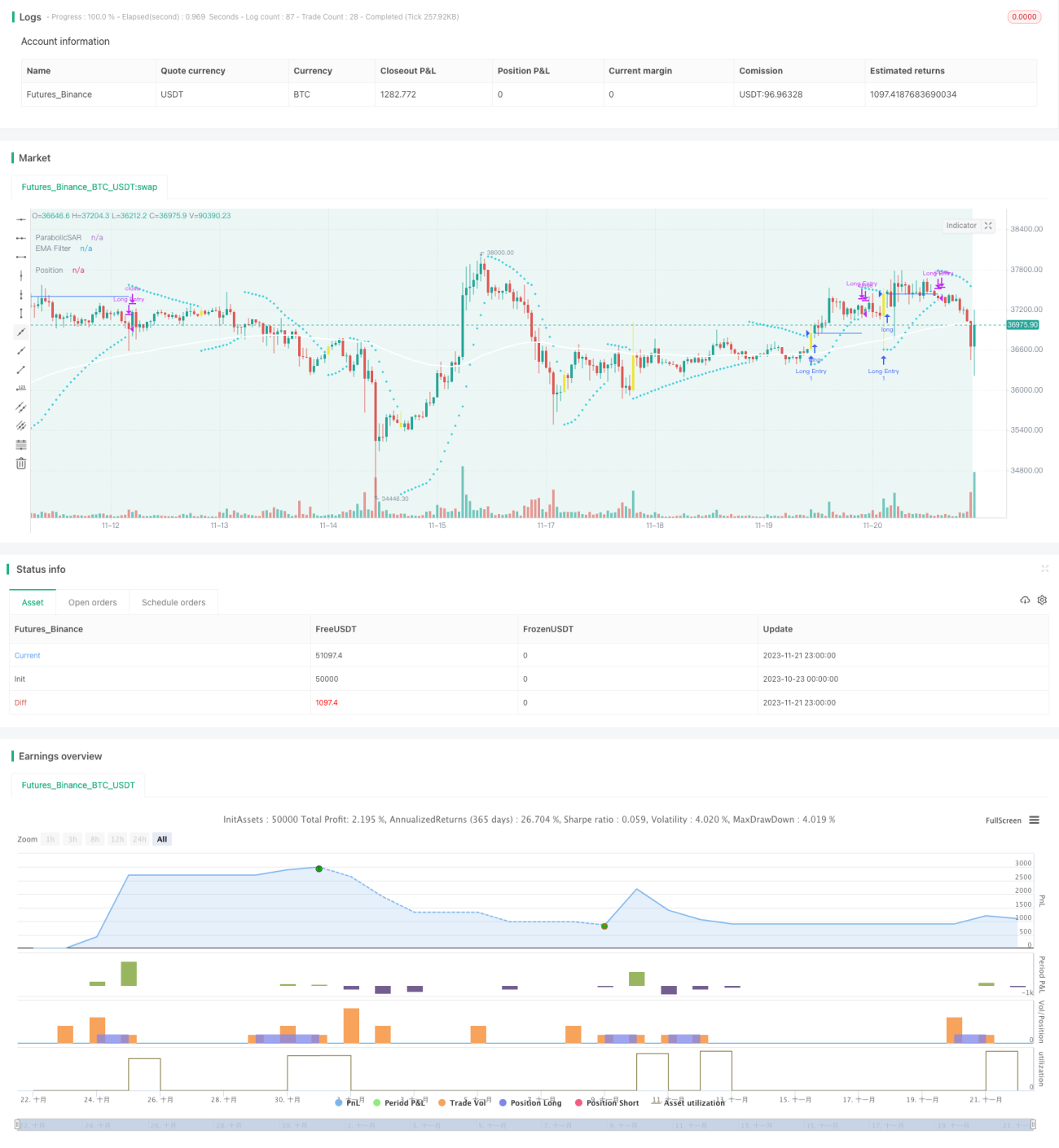

投機ギャップ戦略は、トレンド追従型の定量取引戦略です。SAR平滑曲線を主要な取引シグナルとして使用し、EMA、スクイーズモメンタム、ボラティリティオシレーターなどの複数のフィルターを補助的に活用します。SARパラメータを設定することでトレンド反転ポイントを識別し、低リスクのトレンド追従を実現します。これは中長期投資に非常に適した戦略です。

戦略の原理

この戦略は、パラボリックSARを主要な取引シグナル指標として使用します。SARは価格トレンドの反転ポイントを効果的に判断でき、SARの符号が変化した場合、トレンドが転換したことを意味します。この戦略は通常、SARが反転したときに買いまたは売りのシグナルを発します。

また、この戦略にはSARブレイクアウトオプションも用意されています。つまり、SARが完全に反転する前に、価格が最後のSAR値を突破した場合にシグナルを発生させます。これにより、戦略の感度をさらに高めることができます。

偽のシグナルをフィルタリングするために、この戦略にはEMA、スクイーズモメンタム、ボラティリティオシレーターの3つの補助フィルターが導入されています。これらは単独でも組み合わせても使用でき、価格トレンドと取引シグナルの信頼性を確認します。

最後に、戦略は固定ストップロス、固定テイクプロフィット、リスクリワード比率ストップロスという3つのストップロス・テイクプロフィット方法を提供します。これにより、戦略はさまざまなタイプの取引銘柄の特性に柔軟に対応できます。

優位性分析

-

SARは価格トレンドの反転を正確に判断し、新しい価格トレンドを迅速に捉えることができ、中長期のトレンド追従に適しています。

-

複数のフィルター設定により、偽のブレイクアウトの確率を低減し、シグナルの信頼性を高めます。

-

設定が簡単で柔軟であり、異なる取引銘柄に合わせてパラメータをカスタマイズできます。

-

複数のテイクプロフィット・ストップロス方法を提供し、リスクリターンのバランスを追求できます。

-

取引ボットに直接接続でき、自動取引を実現できます。

リスク分析

-

トレンドのない市場では、偽のシグナルや無効な取引が増える可能性があります。

-

SARパラメータの設定が不適切だと、シグナル判断の正確性に影響を与えます。

-

トレンド追従戦略として、大幅なレンジ相場ではストップロスラインに達しやすくなります。

上記のリスクに対しては、SARパラメータやフィルターパラメータを適宜調整し、無効な取引の確率を低減できます。また、ストップロスの制限を適度に緩め、より大きな相場変動に耐えることもできます。

最適化の方向性

-

SARパラメータの最適化。過去のバックテストデータを使用してSARのステップサイズと増分パラメータを最適化し、より安定した効率的な取引戦略を得ることができます。

-

トレンド判断指標の導入。戦略にMACD、DMIなどの補助判断指標を追加し、トレンドの判断能力を向上させます。

-

リスクリワード比の最適化。固定テイクプロフィット・ストップロスのパーセンテージとリスクリワード比率パラメータを調整し、より高いリスクを適切に負担してより高いリターンを得ます。

-

外貨ペアの追加。現在の戦略は暗号通貨取引のみをサポートしていますが、外国為替、商品、証券市場の銘柄に拡張することができます。

まとめ

投機ギャップ戦略は、非常に実用的なトレンド追従型の定量戦略です。応答性が高く、シグナル判断は信頼性が高く、ストップロス・テイクプロフィット管理により長期的な安定した収益を得ることができます。適切なパラメータとルールの最適化により、戦略の効率をさらに向上させることができます。これは長期的に使用する価値のある高効率な定量戦略です。

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1