Hull移動平均線均勢追跡戦略

概要

均勢追跡戦略は、ハル移動平均線を主要なエントリー指標として使用し、価格トレンドの方向性を判断します。同時に、この戦略は基準線や確認指標などの他の複数の指標を組み合わせ、価格トレンドを検証し、偽シグナルをフィルタリングします。エントリー後は、平均真実レンジ(ATR)を使用して動的なストップロスを計算し、トレンドに追随して利益を獲得します。

戦略の原理

均勢追跡戦略の中核はハル移動平均線です。ハル移動平均線は価格変動に対してより敏感であり、トレンド方向を効果的に判断できます。価格がハル線を上抜けた場合、上昇トレンドの形成が確認され買いポジションを取ります。価格がハル線を下抜けた場合、下降トレンドの形成が確認され売りポジションを取ります。

さらに、この戦略では、長期・短期トレンドを判断するための基準線指標と、偽のブレイクアウトをフィルタリングするための確認指標も導入されています。基準線と確認指標の両方がトレンド方向を検証した場合にのみ、取引シグナルが発動されます。

エントリー後は、ATRとハルEMAを用いて計算された平均真実レンジに基づきストップロス水準を設定します。トレンドが継続するにつれて、ストップロスラインも徐々に上方/下方にシフトし、トレンド利益を確定します。

優位性分析

均勢追跡戦略は、トレンド判断とリスク管理の利点を組み合わせ、トレンド相場で良好な収益を得ることができます。固定ストップロス戦略と比較して、移動ストップロスによってトレンドに追随し、市場の通常の変動によるストップロスを回避できます。

複数の指標を組み合わせることで、市場の変化に対する感度が高まり、偽シグナルを効果的にフィルタリングできます。また、この戦略は調整可能な複数のパラメータを提供しており、ユーザーは自身の市場判断に基づいて最適化できます。

リスク分析

この戦略は主にトレンド指標に依存しているため、レンジ相場では誤ったシグナルやストップロスが発生しやすくなります。また、複数指標の組み合わせにより、指標間で矛盾が生じる可能性もあります。パラメータ設定が不適切な場合、戦略のパフォーマンスが低下する恐れがあります。

対策としては、指標に乖離が生じた場合に取引を一時停止する追加判断モジュールを戦略に組み込むことや、複数の指標の判断結果を総合する投票メカニズムを採用することが考えられます。パラメータ設定に関しては、バックテストによる最適化手法を用いて最適なパラメータを見つけることができます。

最適化の方向性

均勢追跡戦略は、以下の方向で最適化が可能です。

- ボラティリティモジュールなどの判断モジュールを追加し、高ボラティリティ時には取引を一時停止する。

- 機械学習モジュールを追加し、機械学習アルゴリズムを使用して指標の重みを判断する。

- 指標パラメータを最適化し、最適なパラメータの組み合わせを見つける。

- 移動ストップロスのアルゴリズムを最適化し、ストップロスがトレンドにより良く追随できるようにする。

- ストップロスの違反防止や動的なポジション調整などのリスク管理モジュールを追加する。

まとめ

均勢追跡戦略は、全体的に見て優れたトレンドフォロー戦略です。トレンド判断と動的ストップロスをうまく組み合わせ、トレンドに追随して効果的に利益を獲得できます。さらなる最適化により、より良い戦略パフォーマンスが期待できます。本戦略は、定量取引戦略の構築における優れた参考事例となります。

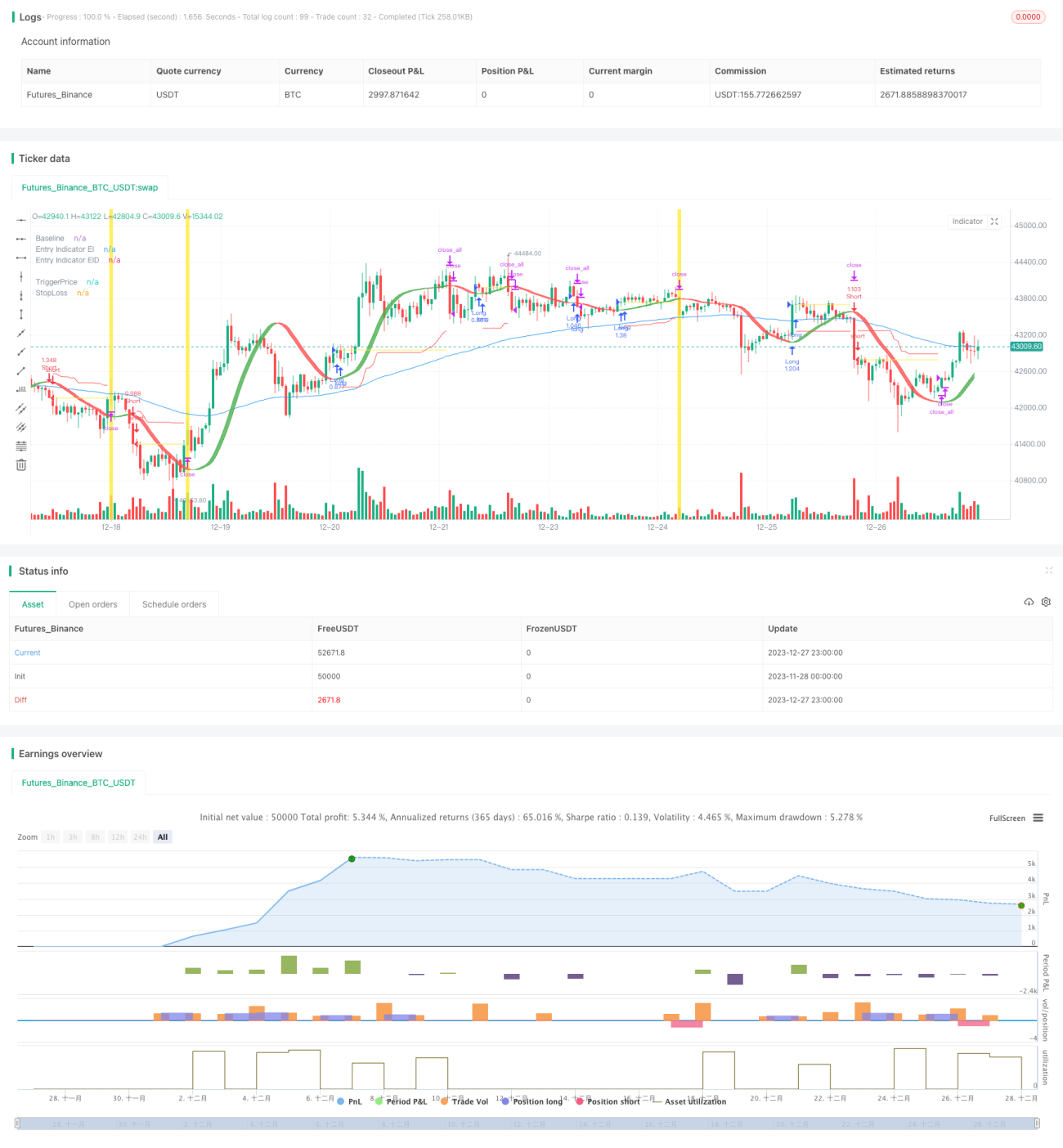

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1