三重移動平均線とMACDの組合せ定量戦略

1

Follow

1802

Followers

概要

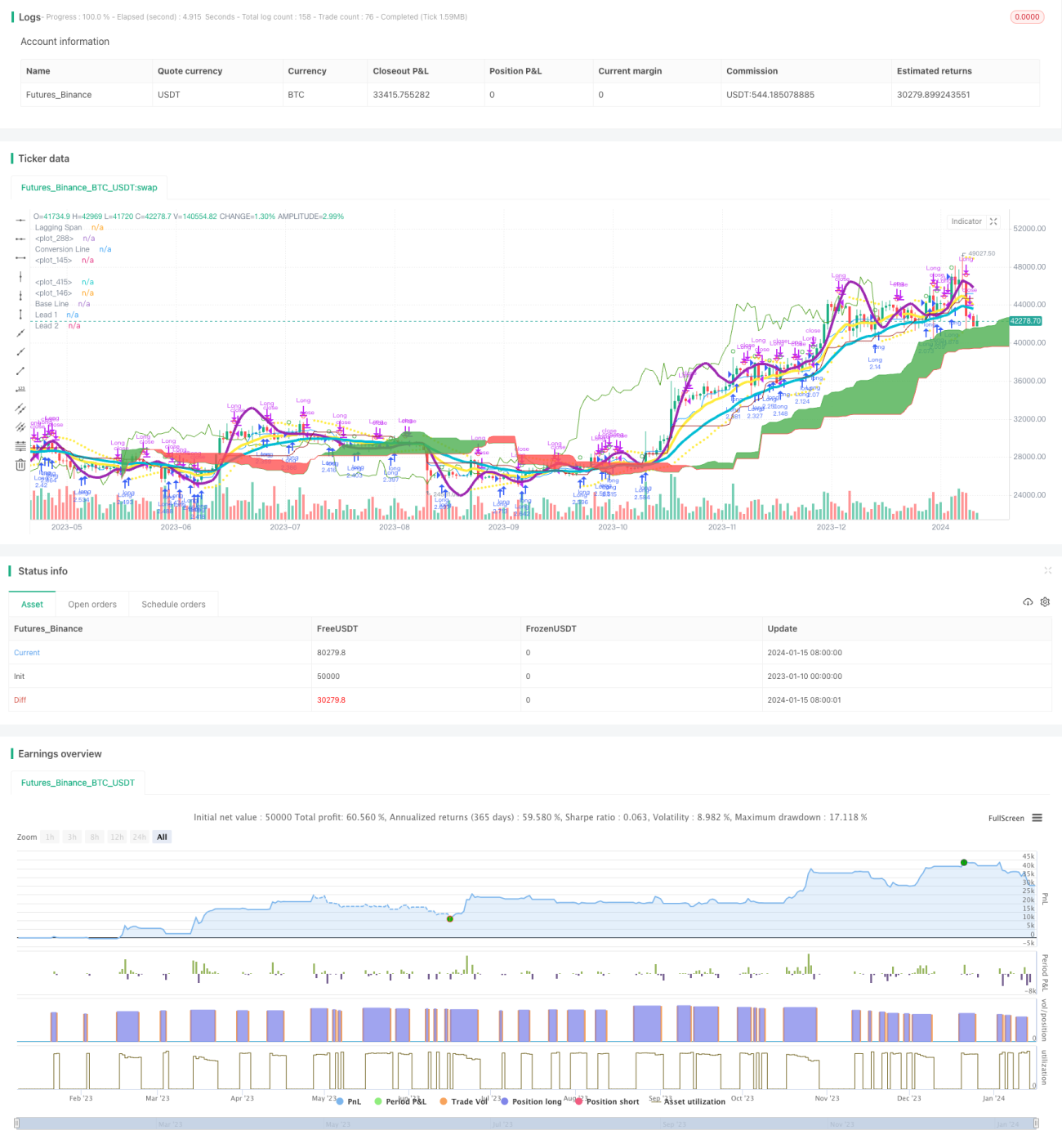

本戦略は、トリプル移動平均線とMACD指標を組み合わせて使用することで、比較的安定かつ信頼性の高い定量取引戦略を開発したものです。この戦略は、将来発生する可能性のあるトレンドを捉えることを目的としており、特に中長期のポジション保有に適しています。

戦略の原理

本戦略は、主にトリプル移動平均線とMACD指標の組み合わせに基づいています。

まず、期間がそれぞれ3、7、2のトリプル指数移動平均線を使用します。これら3本の移動平均線は、短期から長期へと移行する移動平均システムを構築し、将来のトレンド方向を判断するために使用します。短期の移動平均線が長期の移動平均線を上回った場合が買いシグナル、短期の移動平均線が長期の移動平均線を下回った場合が売りシグナルとなります。

次に、本戦略では同時に期間パラメータが3と7のMACD指標も使用します。MACDのメインラインがシグナルラインを上回った場合が買いシグナル、下回った場合が売りシグナルとなります。

2つの指標を組み合わせて使用することで、単一の指標による誤ったシグナルを複数回発生させることを回避し、戦略の安定性を向上させます。

戦略の優位性

- 二重指標によるフィルタリングにより、シグナルの品質が向上

- パラメータは複数回のテストと最適化を経ており、安定かつ信頼性がある

- トリプル移動平均システムを採用することで、市場のノイズを効果的にフィルタリングし、将来のトレンドを判断できる

- MACD指標のパラメータ設定が比較的速いため、短期的なチャンスを素早く捉えられる

戦略のリスク

- 一定のドローダウンや連続損失のリスクがある

- 市場に明確なトレンドがない場合、本戦略では誤った取引が多く発生する

- MACD指標は誤ったシグナルを発生しやすいため、移動平均線指標と組み合わせて使用する必要がある

解決策:

- 適切なストップロス戦略を採用し、最大ドローダウンを抑制する

- マーケット状態が明らかに無トレンドの場合、取引頻度を減らす

- MACDパラメータを最適化し、他の指標と組み合わせて使用する

戦略の最適化方向

- 移動平均線とMACDのパラメータをテスト・最適化し、最適な組み合わせを見つける

- KDJ、VRSIなどの補助指標を追加し、誤ったシグナルを回避する

- 機械学習モデルを組み込んでマーケット状態を判断し、動的な調整を実現する

- ストップロス戦略と組み合わせ、最適なストップロスポイントを設定する

まとめ

本戦略は、移動平均線とMACDの組み合わせにより、安定したトレンド捕捉を実現しました。その戦略の優位性は指標の組み合わせ使用にあり、誤ったシグナルを効果的に削減し、良好な戦略効果を得られます。次のステップとして、パラメータ最適化、ストップロス戦略の導入、動的調整などを通じて本戦略をさらに改良し、中長期の機会を探すための効果的なツールとします。

Source

Pine

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1