双方向グリッド・ローソク足追跡取引戦略

1

Follow

1802

Followers

概要

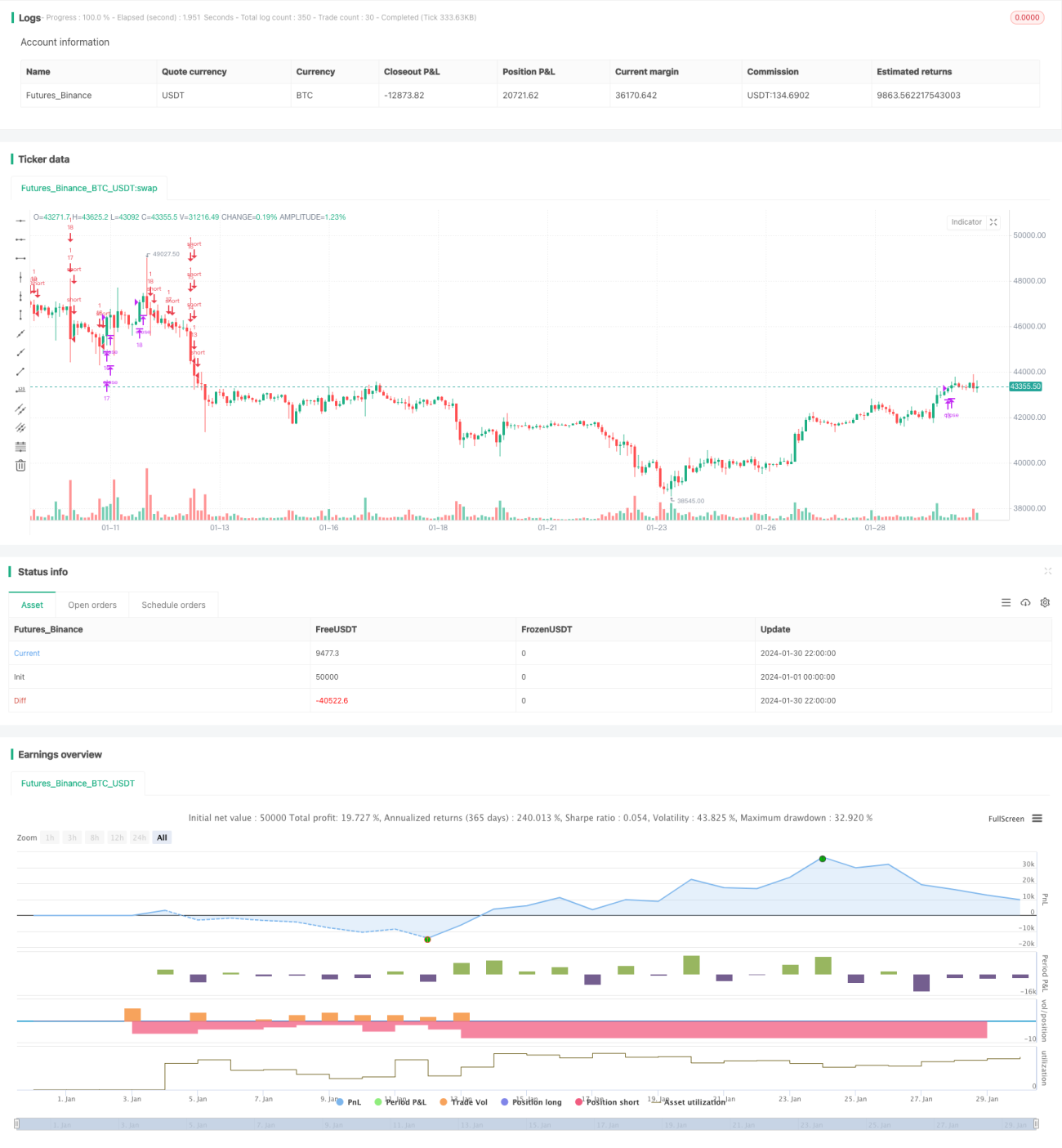

本戦略は、ローソク足のリアルタイム変化に基づく双方向追跡グリッド取引戦略です。強気相場と弱気相場の両方で安定した利益を得ることができます。

戦略の原理

-

ユーザーが設定したグリッド数に基づいて、価格グリッド区間と各グリッド価格を自動計算します。

-

価格がグリッド価格を突破した場合、固定数量で買い建てを行います。価格がグリッド価格を下回った場合、買いポジションを決済し、売り建てを行います。

-

これにより、価格がグリッド区間内で変動する際に、価格変動を追跡して利益を得ることができます。

優位性分析

-

適切なグリッド区間を自動計算するため、手動でサポート・レジスタンスを決定する必要がありません。

-

双方向取引により、相場変動の多い市場環境にも適応できます。

-

固定建玉数量により、リスク管理が容易です。

-

コードは直感的で簡潔であり、理解や修正が容易です。

リスク分析

-

相場の急激な変動により損失が拡大する可能性があります。

-

取引手数料の累積も最終的な利益に影響を与えます。

-

グリッド数を適切に設定する必要があり、グリッド数が多すぎると取引回数が増える一方で1回あたりの利益が限定的になります。

最適化の方向性

-

ストップロス戦略を追加し、損失拡大を防止します。

-

グリッド数を動的に調整する機能を追加します。

-

レバレッジの導入を検討し、取引量を拡大します。

まとめ

本戦略は全体的な考え方が明確かつ簡潔であり、双方向追跡グリッド取引により安定した収益を得ることを目指しますが、一定の取引リスクも存在します。継続的な最適化により、より良い結果が期待できます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1