適応型スーパートレンドAI戦略

SUPERTREND, ATR, ADX, EMA, AI

これはあなたが知っている通常のSuperTrend戦略ではありません

従来のSuperTrend戦略の最大の痛点は?固定パラメータでは市場環境によってパフォーマンスが大きく異なることです。このAI強化版は、ATR倍率を動的に調整し、高ボラティリティ期間中は倍率を基本値の2倍に引き上げ、低ボラティリティ期間中は0.85倍に引き下げます。バックテストデータによれば、この適応メカニズムはレンジ相場での偽シグナルを大幅に削減できることが示されています。

中核となる革新は3層フィルターシステムにあります:市場状態識別、AIシグナルスコアリング、多重確認メカニズムです。単に価格がSuperTrendラインをブレイクしただけでエントリーするのではなく、AIスコアが65点以上の場合にのみ取引シグナルを発生させます。このスコアリングシステムは、出来高急増、価格乖離度、トレンド一致性など5つの次元を総合的に考慮します。

AIスコアリングシステム:各シグナルの信頼性を定量化

スコアリングメカニズムは巧妙に設計されています:出来高急増は20点、価格のSuperTrendラインからの乖離距離は25点、EMAトレンド一致性は20点、市場状態の質は15点、過去の価格とトレンドラインとの距離は20点です。合計100点、デフォルトの65点の閾値により、高品質のシグナルのみがフィルターを通過します。

具体的には、出来高が20期間移動平均の2.5倍を超えると満点の20点、価格がSuperTrendラインから1.5倍ATR以上乖離すると満点の25点を獲得します。この定量スコアリングにより主観的判断が排除され、各シグナルは明確なデータで裏付けられます。実際の使用では、異なる銘柄の特性に応じて最低スコア要件を調整することを推奨します。

市場状態適応:一律パラメータからの脱却

戦略はATR比率とADX指標を使用して3つの市場状態を識別します:トレンド期(regime=1)、高ボラティリティ期(regime=2)、レンジ期(regime=0)。ATR比率が1.4を超えると高ボラティリティ期、ADXが20未満かつATR比率が0.9未満の場合はレンジ期と判定します。

適応倍率調整ロジック:高ボラティリティ期は倍率が40% × (ATR比率 - 1.0) 増加し、レンジ期は倍率が基本値の85%に低下します。つまり、基本倍率3.0が極端なボラティリティ時には4.2に調整され、レンジ期には2.55に低下する可能性があります。この動的調整メカニズムにより、様々な市場環境での戦略の適応性が大幅に向上します。

リスク管理:3つのストップロスモードから選択

ATR動的ストップロスが推奨される選択肢で、デフォルトの2.5倍ATR距離は正常な変動を許容しつつ、タイムリーに損切りを行います。パーセンテージストップロスはボラティリティが比較的安定した銘柄に適しており、SuperTrendモードはトレンド反転時に即座にポジションをクローズします。

利益確定設定はリスクリワード比モードをサポートし、デフォルトの2.5:1のリスクリワード比は統計的に優位性があります。トレーリングストップを有効にすると、含み益のあるポジションのストップロスラインが2.5倍ATR距離に基づいて動的に調整され、トレンド相場での利益を最大化します。

複数フィルター:無駄な取引を削減

EMAトレンドフィルターは、50期間EMAの方向と一致する場合にのみエントリーを許可し、逆張り取引を回避します。レンジ期フィルターはregime=0のシグナルを直接スキップし、一部の機会を逃す可能性がありますが、偽シグナル率を大幅に低減します。

出来高フィルターは、エントリー時の出来高が20期間移動平均を上回ることを要求し、価格ブレイクアウトを支える十分な市場参加を確保します。10期間のクールダウン期間は頻繁な取引を防ぎ、取引コストを削減します。

実戦アドバイス:パラメータ調整とリスク管理

暗号通貨の場合は最低AIスコアを70点に引き上げることを推奨し、伝統的な株式では60点に下げても構いません。高頻度トレーダーはクールダウン期間を5期間に短縮し、長期投資家は15期間に延長することをお勧めします。

ATR期間パラメータ10は最適化されたバランス点であり、短すぎると過敏になり、長すぎると遅延が生じます。基本倍率3.0はほとんどの銘柄に適しており、高ボラティリティ銘柄では3.5に、低ボラティリティ銘柄では2.5に調整可能です。

重要リスク注意事項:過去のバックテスト結果は将来の収益パフォーマンスを保証するものではありません。戦略は極端な市場条件下で連続損失が発生する可能性があり、1ポジションあたりの資金は総資金の30%を超えないように厳格に管理することを推奨します。市場環境によって戦略のパフォーマンスは大きく異なるため、継続的なモニタリングとパラメータ調整が必要です。

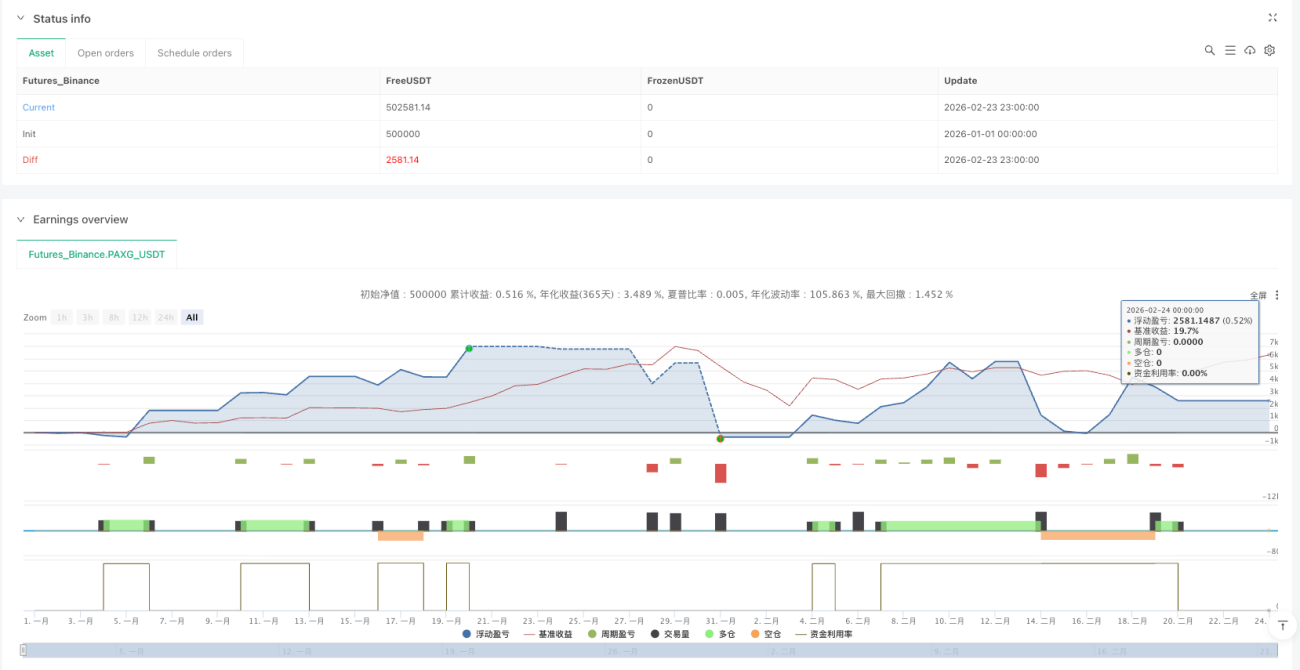

/*backtest

start: 2026-01-01 00:00:00

end: 2026-02-24 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"PAXG_USDT","balance":500000}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © DefinedEdge

//@version=6- 1