간편하고 나쁜 계약망

저자:노보, 날짜: 2021-11-18 17:28:35태그:

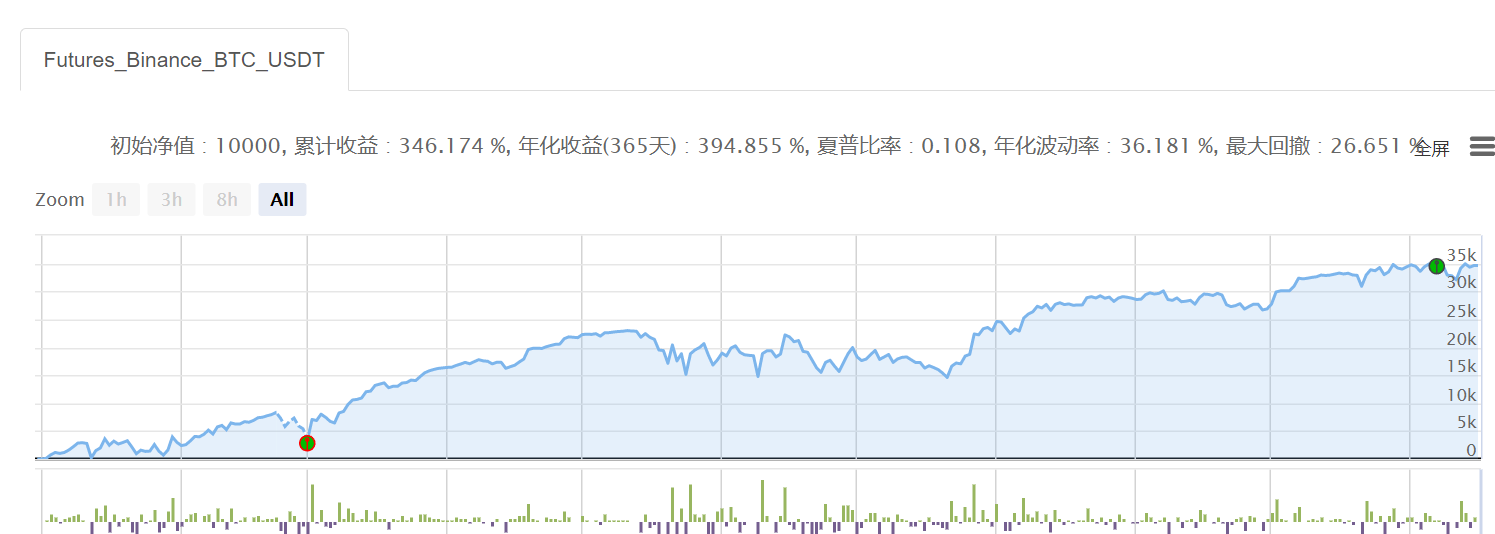

매개 변수는 매우 간단합니다. 예를 들어 BTC로, 많은 지역으로 평평한 하위 입장을 더 많이, 개방된 지역으로 평평한 하위 입장을 더 많이, 반복적으로 돌아갑니다.

분명히, 장기적으로, 어떤 복잡한 모델도 뇌 없는 격자에서 실행될 수 없습니다.

부의 암호는 뇌가 없는 네트워크 + 뇌가 없는

'''backtest

start: 2021-01-01 00:00:00

end: 2021-11-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":2500}]

args: [["H",30],["n1",0.001],["grid",300],["xia",50000]]

'''

def CancelPendingOrders():

orders = _C(exchanges[0].GetOrders)

if len(orders)>0:

for j in range(len(orders)):

exchanges[0].CancelOrder(orders[j].Id, orders[j])

j=j+1

def main():

exchange.SetContractType('swap')

exchange.SetMarginLevel(M)

currency=exchange.GetCurrency()

if _G('buyp') and _G('sellp'):

buyp=_G('buyp')

sellp=_G('sellp')

Log('读取网格价格')

else:

ticker=exchange.GetTicker()

buyp=ticker["Last"]-grid

sellp=ticker["Last"]+grid

_G('buyp',buyp)

_G('sellp',sellp)

Log('网格数据初始化')

while True:

account=exchange.GetAccount()

ticker=exchange.GetTicker()

position=exchange.GetPosition()

orders=exchange.GetOrders()

if len(position)==0:

if ticker["Last"]>shang:

exchange.SetDirection('sell')

exchange.Sell(-1,n1*H)

Log(currency,'到达开空区域,买入空头底仓')

else:

exchange.SetDirection('buy')

exchange.Buy(-1,n1*H)

Log(currency,'到达开多区域,买入多头底仓')

if len(position)==1:

if position[0]["Type"]==1:

if ticker["Last"]<xia:

Log(currency,'空单全部止盈反手')

exchange.SetDirection('closesell')

exchange.Buy(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('sell')

exchange.Sell(sellp,n1)

exchange.SetDirection('closesell')

exchange.Buy(buyp,n1)

if len(orders)==1:

if orders[0]["Type"]==1: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

if orders[0]["Type"]==0:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if position[0]["Type"]==0:

if ticker["Last"]>float(shang):

Log(currency,'多单全部止盈反手')

exchange.SetDirection('closebuy')

exchange.Sell(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('buy')

exchange.Buy(buyp,n1)

exchange.SetDirection('closebuy')

exchange.Sell(sellp,n1)

if len(orders)==1:

if orders[0]["Type"]==0: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if orders[0]["Type"]==1:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

더 많은

- 熊

币牛 U의 균형 전략 - 디지털 화폐 선물 다종양 ATR 전략 (교육)

- USDT를 계약 계좌에서 현금/자금 계좌로 전환합니다 (OKEX, Binance 동시 지원)

- 비엔인 거래 단말기 자금 이동 도구

- 계좌에 있는 모든 주문이 표시됩니다.

- 바이안은 손동작으로 거래소를 열었습니다.

- HttpQuery를 통해 Binance K줄 데이터를 직접 가져옵니다.

- 디지털 화폐 현금 다품질 양평선 전략 (교육)

- 주요 거래소 자본금 요금 집계

- 디지털 통화 선물 쌍평선 전환점 전략 (교육)

- 현금 지수 균형 전략 v1.1 (한동안 실행되었으나 현재 버그가 있는 것으로 추정되며, 사용되지 않아서 수정해야 합니다)

- 币usdt 계약의 전체 통화 이름을 얻으십시오

- 바이오안 웹소켓 가입 영구 계약 시장 정보

- 冲币安 신상금 개시

- 다른 사람들이 폭동을 일으키면 반대쪽으로 돌립니다.

- 자동으로 비트코인 상속계약 거래 정밀도 & 최소 오픈 포지션u (버린 포지션) 를 얻는다

- 상속 계약 1채 시장 평형

- 현금 균형 전략 - 0.0.1v

- 비안안 계약 격자 - 0.0.2v

- 지수 헤딩 (

로 현장) 0.0.1

메크스민for는 회전 문법 문제입니다.

가벼운 구름트레이스백 (most recent call last) 을 요청하는 데 오류가 발생했습니다. 어떻게 해야 할지 모르겠어요. 감사합니다.

가벼운 구름JS로 글을 쓸 수 있다면 더 좋을 것 같아요 O ((

가벼운 구름좋습니다. 감사합니다.

노보이 문제를 풀기 위해