매일 얽히는 분심선 퀀트 전략

개요

일일 꼬임 분산선 정량 전략은 이동평균선과 최고최저가 지표를 기반으로 한 단기 퀀트 트레이딩 전략입니다. SSL 혼합 지표의 EXIT 화살표를 활용하여 매수/매도 시점을 판단하고, QQE 지표로 필터링하며, ATR 지표를 사용하여 손절가와 분할 매수 가격을 계산합니다. 이 전략은 시장 변동성에 민감하고 리스크 관리에 엄격한 투자자에게 적합합니다.

전략 원리

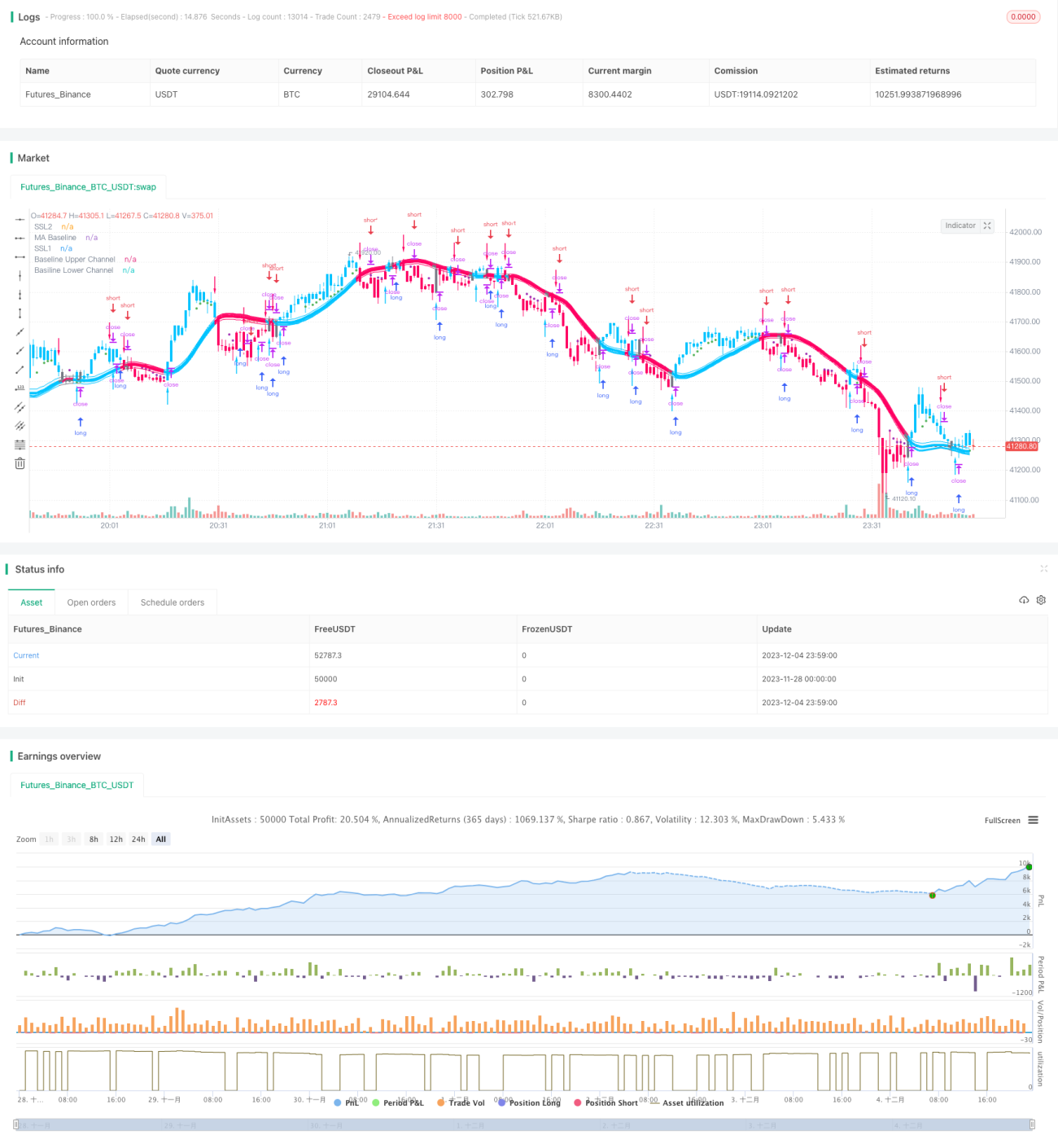

이 전략은 SSL 혼합 지표의 EXIT 화살표를 사용하여 매수/매도 진입점을 판단합니다. EXIT 화살표 위쪽은 EXIT 고점, 아래쪽은 EXIT 저점입니다. 종가가 EXIT 고점에서 아래로 교차하면 매도 신호가 발생하고, 종가가 EXIT 저점에서 위로 교차하면 매수 신호가 발생합니다.

신호의 신뢰성을 높이기 위해 이 전략은 QQE 지표를 보조 필터 조건으로 도입합니다. EXIT 화살표에서 발생한 신호는 QQE 지표가 같은 방향일 때만 실행됩니다.

리스크를 통제하기 위해 이 전략은 배수 ATR 지표를 사용하여 손절가와 분할 매수 가격을 계산합니다. 공포(short) 손절가는 종가 + ATR×1.8, 롱(long) 손절가는 종가 - ATR×1.8입니다. 3회에 걸쳐 분할 매수하며, 각 회차 매수 금액은 초기 금액의 10%이며, 매수 가격은 각각 종가 - ATR×0.1, 종가 - ATR×0.3, 종가 - ATR×0.7입니다.

각 회차 매수마다 개별 손절이 설정되며, 첫 번째 회차의 20% 포지션은 손절가에 도달하면 손절되고 나머지 포지션은 계속 보유됩니다.

전략 장점

- EXIT 화살표를 통해 수익을 얻고 신속하게 손절하여 리스크를 효과적으로 통제합니다.

- QQE 지표 필터링으로 신호의 정확도를 높입니다.

- ATR 지표를 활용하여 시장 변동성에 따라 손절가와 매수 가격을 계산하므로 리스크 관리가 더 정밀합니다.

- 분할 매수를 통해 추세 수익을 충분히 포착합니다.

전략 리스크

- 수익 포지션이 부분 손절에 도달하면 나머지 포지션이 추가 손절 위험에 노출될 수 있습니다. 전체 이익실현 또는 주식 본질의 펀더멘털 기반 이익실현을 고려할 수 있습니다.

- EXIT 화살표와 QQE 지표의 시장 변동성에 대한 민감도가 달라 상충되는 신호가 발생할 수 있으므로, 매개변수를 조정하여 신호 충돌을 줄여야 합니다.

- 지나치게 공격적인 분할 매수는 추격 매수/패닉 매도 상황을 초래할 수 있습니다. 상황을 신중히 판단하고 레버리지 수준을 낮춰야 합니다.

최적화 방향

- 주식 본질의 펀더멘털 지표(예: 장부가비율, PER, 배당수익률 등)를 결합하여 합리적인 이익실현 가격을 설정합니다.

- QQE 지표의 매개변수를 조정하여 EXIT 화살표에서 발생하는 신호와 일관성을 유지합니다.

- 시장 과열도에 따라 분할 매수 비율을 낮추고, 변동장에서는 분할 매수를 줄입니다.

- 최대 낙폭, 손익비 등의 지표를 바탕으로 최적의 매개변수 조합을 테스트합니다.

요약

이 전략은 SSL 혼합 지표의 EXIT 화살표를 신호 핵심으로 삼고, QQE 지표와 ATR 지표를 필터링 및 손절에 활용합니다. 분할 매수를 통해 수익을 확대합니다. 시장의 단기 추세를 추적하는 데 적합한 단기 퀀트 전략입니다. 이 전략은 낙폭 통제 및 리스크 관리 능력을 갖추고 있지만, 신호 충돌, 추격 매수/패닉 매도 등의 리스크에 주의해야 합니다. 주식 펀더멘털에 기반한 이익실현 방법을 결합하고 시장 변동성을 판단하여 분할 매수 비율을 더 신중하게 조정한다면, 이 전략의 수익 공간은 더욱 커질 것입니다.

- 1