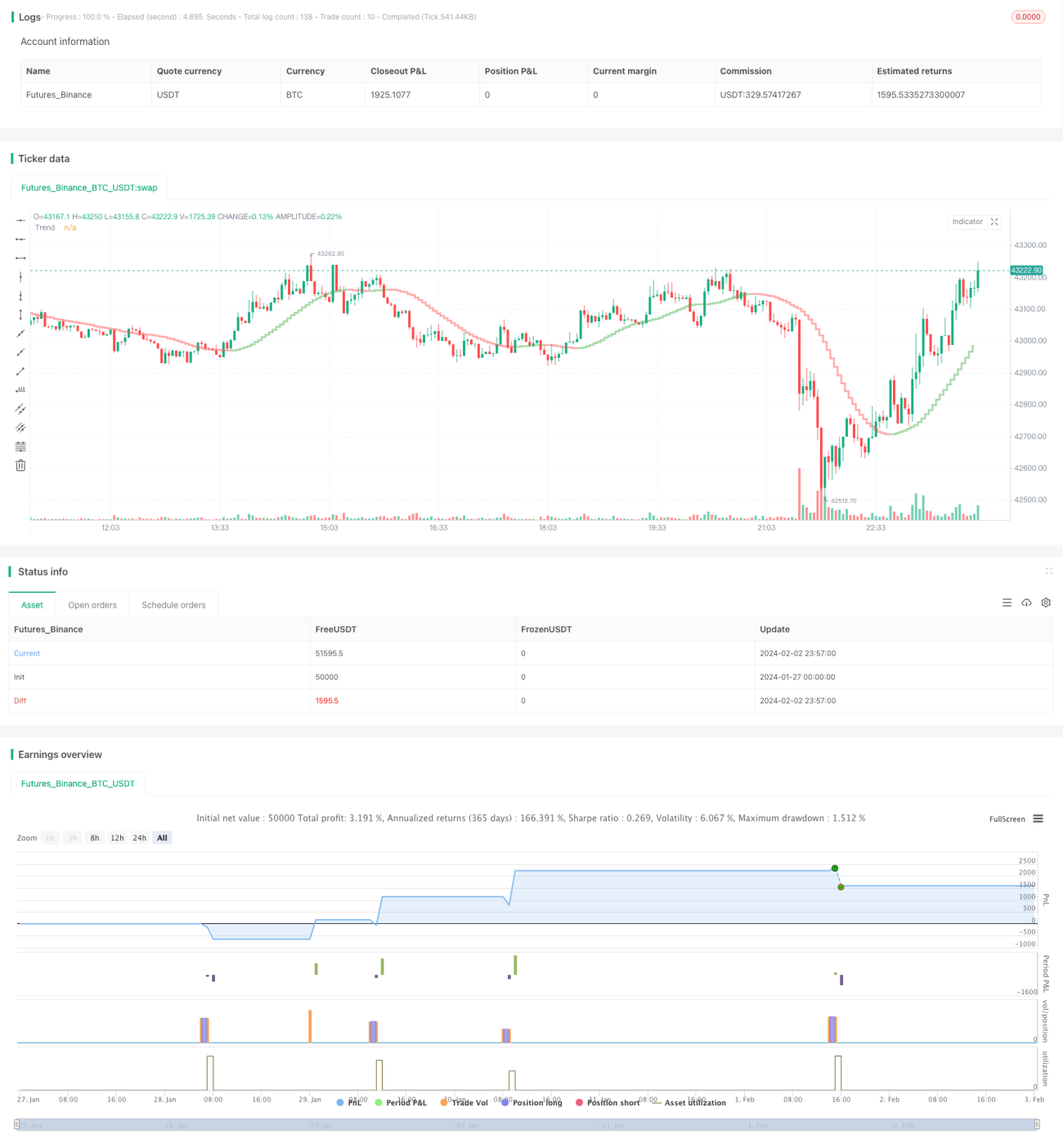

백테스트 구간 Coral Trend 지표 기반 리플 전략

개요

본 전략은 LazyBear의 Coral Trend 지표를 사용하여 가격 추세 방향을 판단하고, Coral Trend 지표 방향의 반전을 식별하여 잠재적인 진입 지점을 찾습니다. 가짜 돌파를 걸러내기 위해 본 전략은 ADX 지표 또는 Absolute Strength Histogram과 HawkEye Volume 지표의 조합을 확인 지표로 사용하여 보다 신뢰할 수 있는 진입을 구현합니다.

Exit 메커니즘은 최근 N개 봉의 최고가/최저가에 설정 가능한 위험 보상 비율을 곱하여 손절가와 이익 실현가를 설정합니다.

전략 원리

Coral Trend 지표를 기반으로 큰 추세 방향을 판단한 후, 지표 색상이 동일하게 유지되는 동안 가격이 반대 방향으로 작은 되돌림(pullback)이 발생합니다. 이때 되돌림이 끝나고 가격이 다시 Coral Trend가 지시하는 주 추세 방향으로 돌아간다면 좋은 진입时机로 간주할 수 있습니다.

진입 조건은 다음과 같습니다:

-

Coral Trend 지표 방향이 거래 방향과 일치(롱=초록, 숏=빨강)

-

이전 가격이 Coral Trend 지표를 완전히 돌파한 이후(마지막 봉의 고점이 모두 Coral Trend 선 위) 적어도 1개 봉의 저점이 모두 Coral Trend 지표 위(롱) 또는 고점이 모두 Coral Trend 지표 아래(숏)에 있어야 함

-

반대 방향으로 작은 되돌림(당겨짐)이 발생하며, 이 되돌림 과정에서 종가가 계속 Coral Trend의 반대쪽에 유지됨

-

작은 되돌림이 끝난 후, 종가가 다시 Coral Trend가 지시하는 주 추세 방향으로 돌아옴

위 조건이 주요 조건입니다. 동시에 전략은 ADX 지표 또는 Absolute Strength Histogram과 HawkEye Volume 지표를 진입 확인 조건으로 사용합니다.

ADX 지표는 값이 20보다 크고 최근 1개 봉이 상승해야 합니다. 또한 DI의 초록선과 빨간선 순서가 거래 방향과 일치해야 합니다.

Absolute Strength Histogram은 색상이 거래 방향과 일치해야 하며(롱=파랑, 숏=빨강), HawkEye Volume도 색상이 거래 방향과 일치해야 합니다(롱=초록, 숏=빨강).

Exit 메커니즘은 최근 N개 봉의 최고가 또는 최저가에 위험 보상 비율을 곱하여 손절가와 이익 실현가를 설정합니다. N값과 위험 보상 비율은 매개변수로 설정 가능합니다.

장점 분석

본 전략의 가장 큰 장점은 Coral Trend 지표로 주 추세 방향을 판단한 후, 그 반전을 식별하여 진입 기회를 포착함으로써 비추세 시장에서의 표류를 피할 수 있다는 점입니다. 동시에 확인 지표를 사용하여 많은 가짜 돌파를 걸러내어 진입 성공률을 높일 수 있습니다.

또한 본 전략은 손절폭 설정 및 위험 노출 비율 통제를 포함한 완전한 위험 관리 메커니즘을 제공하여, 개별 거래에서 손실이 발생하더라도 전체 자금에 큰 충격을 주지 않습니다.

위험 분석

본 전략의 가장 큰 위험은 지표를 사용한 진입 판단으로 인해 매개변수 설정만으로 자동으로 수익을 낼 수 있다는 착각을 불러일으킬 수 있다는 점입니다. 실제로 매개변수 최적화와 규칙 설정은 바닥 가격 변동 패턴을 결합하고 지표와 가격의 연동 효과를 직관적으로 판단해야만 자신의 거래 스타일과 종목에 더 적합한 설정을 할 수 있습니다.

또한 손절가와 이익 실현가의 설정도 적절해야 합니다. 너무 큰 이익 실현 배수는 이익 실현 이탈을 불가능하게 만들 수 있고, 너무 작은 손절가는 위험을 과도하게 만듭니다. 이는 종목별 변동성 정도와 개인의 위험 감내 능력에 따라 설정해야 합니다.

최적화 방향

본 전략의 최적화 방향은 다음과 같습니다:

-

Coral Trend 지표의 매개변수를 조정하여 다양한 종목의 가격 변동에 더 민감하게 반응하도록 함

-

KDJ, MACD 등 다양한 확인 지표 또는 지표 조합을 시도하여 진입 신호의 정확도를 높임

-

종목별 변동성 정도에 따라 손절가와 이익 실현가 계산 방식을 조정하여 더 나은 위험 관리 구현

-

자금 관리 모듈 추가: 포지션 수량에 따라 단일 주문량을 조정하여 전체 손실을 효과적으로 통제

-

거래 시간 제어 모듈 추가: 특정 시간대에만 전략이 작동하도록 하여 급변동 기간의 손실 방지

요약

본 전략은 먼저 Coral Trend를 사용하여 가격의 중장기 추세를 판단하고, 그 반전을 판단하고 확인 신호로 가짜 돌파를 걸러내어 비교적 신뢰할 수 있는 추세 추종 전략을 구축했습니다. 또한 완벽한 위험 관리 설정으로 장기간 운영하면서 자금이 안정적으로 유지됩니다. 추가적인 매개변수 및 모듈 최적화를 통해 더 많은 종목에 적응하고 더 나은 안정성과 수익성을 가질 것으로 기대됩니다.

- 1