Versi Python dari Strategi Hedge Bollinger Intertemporal Commodity Futures (Hanya untuk tujuan kajian)

Penulis:Kebaikan, Dicipta: 2020-06-20 10:52:34, Dikemas kini: 2023-10-31 21:05:21

Strategi arbitraj intertemporal yang telah ditulis sebelum ini memerlukan input manual spread lindung nilai untuk membuka dan menutup kedudukan. menilai perbezaan harga adalah lebih subjektif. Dalam artikel ini, kita akan menukar strategi lindung nilai sebelumnya kepada strategi menggunakan penunjuk BOLL untuk membuka dan menutup kedudukan.

class Hedge:

'Hedging control class'

def __init__(self, q, e, initAccount, symbolA, symbolB, maPeriod, atrRatio, opAmount):

self.q = q

self.initAccount = initAccount

self.status = 0

self.symbolA = symbolA

self.symbolB = symbolB

self.e = e

self.isBusy = False

self.maPeriod = maPeriod

self.atrRatio = atrRatio

self.opAmount = opAmount

self.records = []

self.preBarTime = 0

def poll(self):

if (self.isBusy or not exchange.IO("status")) or not ext.IsTrading(self.symbolA):

Sleep(1000)

return

insDetailA = exchange.SetContractType(self.symbolA)

if not insDetailA:

return

recordsA = exchange.GetRecords()

if not recordsA:

return

insDetailB = exchange.SetContractType(self.symbolB)

if not insDetailB:

return

recordsB = exchange.GetRecords()

if not recordsB:

return

# Calculate the spread price K line

if recordsA[-1]["Time"] != recordsB[-1]["Time"]:

return

minL = min(len(recordsA), len(recordsB))

rA = recordsA.copy()

rB = recordsB.copy()

rA.reverse()

rB.reverse()

count = 0

arrDiff = []

for i in range(minL):

arrDiff.append(rB[i]["Close"] - rA[i]["Close"])

arrDiff.reverse()

if len(arrDiff) < self.maPeriod:

return

# Calculate Bollinger Bands indicator

boll = TA.BOLL(arrDiff, self.maPeriod, self.atrRatio)

ext.PlotLine("upper trail", boll[0][-2], recordsA[-2]["Time"])

ext.PlotLine("middle trail", boll[1][-2], recordsA[-2]["Time"])

ext.PlotLine("lower trail", boll[2][-2], recordsA[-2]["Time"])

ext.PlotLine("Closing price spread", arrDiff[-2], recordsA[-2]["Time"])

LogStatus(_D(), "upper trail:", boll[0][-1], "\n", "middle trail:", boll[1][-1], "\n", "lower trail:", boll[2][-1], "\n", "Current closing price spread:", arrDiff[-1])

action = 0

# Signal trigger

if self.status == 0:

if arrDiff[-1] > boll[0][-1]:

Log("Open position A buy B sell", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 2

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A buy B sell", "Positive")

elif arrDiff[-1] < boll[2][-1]:

Log("Open position A sell B buy", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 1

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A sell B buy", "Negative")

elif self.status == 1 and arrDiff[-1] > boll[1][-1]:

Log("Close position A buy B sell", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 2

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A buy B sell", "Close Negative")

elif self.status == 2 and arrDiff[-1] < boll[1][-1]:

Log("Close position A sell B buy", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 1

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A sell B buy", "Close Positive")

# Execute specific instructions

if action == 0:

return

self.isBusy = True

tasks = []

if action == 1:

tasks.append([self.symbolA, "sell" if self.status == 0 else "closebuy"])

tasks.append([self.symbolB, "buy" if self.status == 0 else "closesell"])

elif action == 2:

tasks.append([self.symbolA, "buy" if self.status == 0 else "closesell"])

tasks.append([self.symbolB, "sell" if self.status == 0 else "closebuy"])

def callBack(task, ret):

def callBack(task, ret):

self.isBusy = False

if task["action"] == "sell":

self.status = 2

elif task["action"] == "buy":

self.status = 1

else:

self.status = 0

account = _C(exchange.GetAccount)

LogProfit(account["Balance"] - self.initAccount["Balance"], account)

self.q.pushTask(self.e, tasks[1][0], tasks[1][1], self.opAmount, callBack)

self.q.pushTask(self.e, tasks[0][0], tasks[0][1], self.opAmount, callBack)

def main():

SetErrorFilter("ready|login|timeout")

Log("Connecting to the trading server...")

while not exchange.IO("status"):

Sleep(1000)

Log("Successfully connected to the trading server")

initAccount = _C(exchange.GetAccount)

Log(initAccount)

def callBack(task, ret):

Log(task["desc"], "success" if ret else "failure")

q = ext.NewTaskQueue(callBack)

p = ext.NewPositionManager()

if CoverAll:

Log("Start closing all remaining positions...")

p.CoverAll()

Log("Operation complete")

t = Hedge(q, exchange, initAccount, SA, SB, MAPeriod, ATRRatio, OpAmount)

while True:

q.poll()

t.poll()

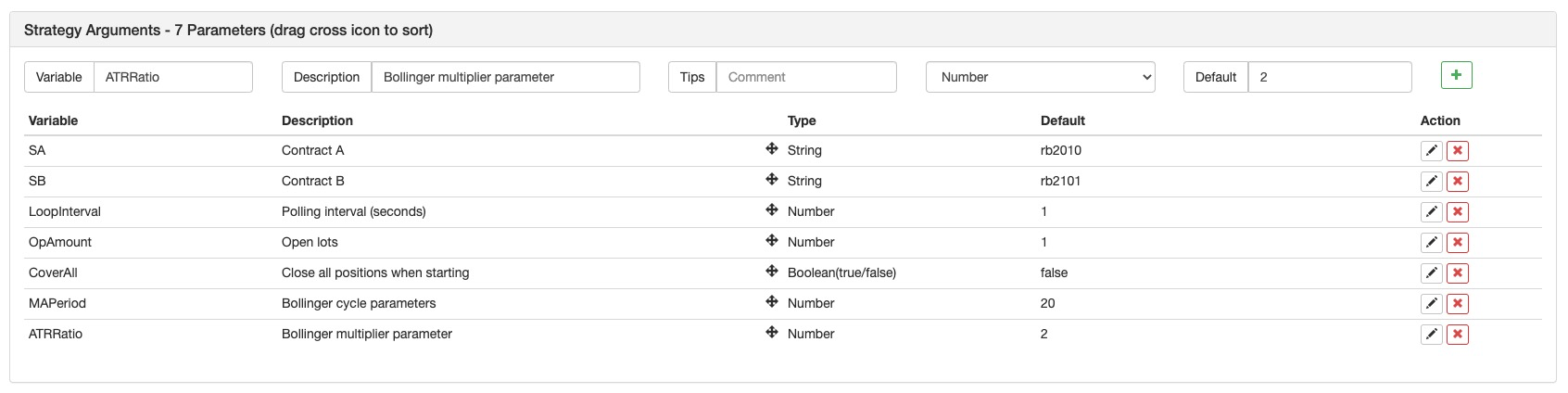

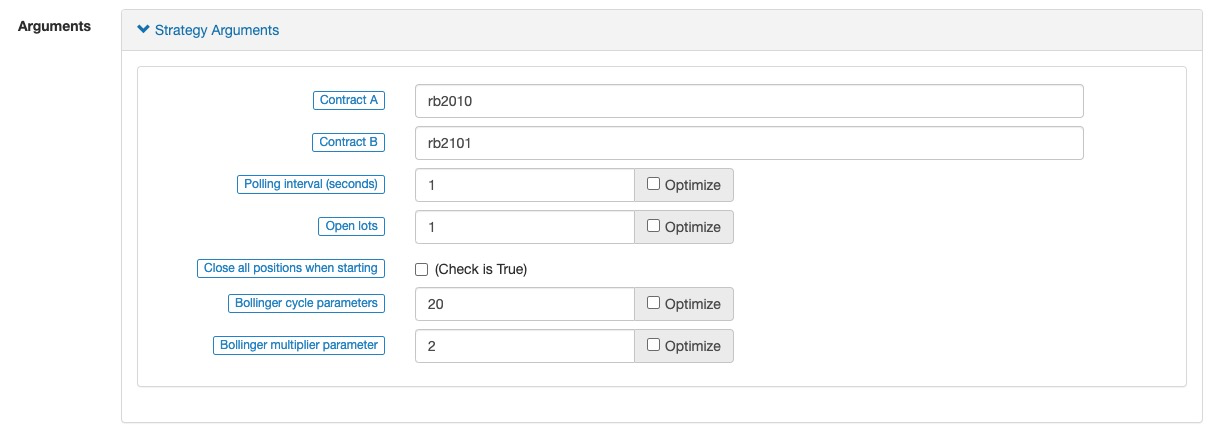

Tetapan parameter strategi:

Rangka strategi keseluruhan pada dasarnya sama denganVersi Python strategi lindung nilai intertemporal niaga hadapan komoditi, kecuali bahawa parameter penunjuk BOLL yang sepadan ditambahkan. Apabila strategi berjalan, data K-line kedua-dua kontrak diperoleh, dan kemudian perbezaan harga dikira untuk mengira spread.TA.BOLLfungsi untuk mengira Bollinger Bands. Apabila penyebaran melebihi rel atas Bollinger Band

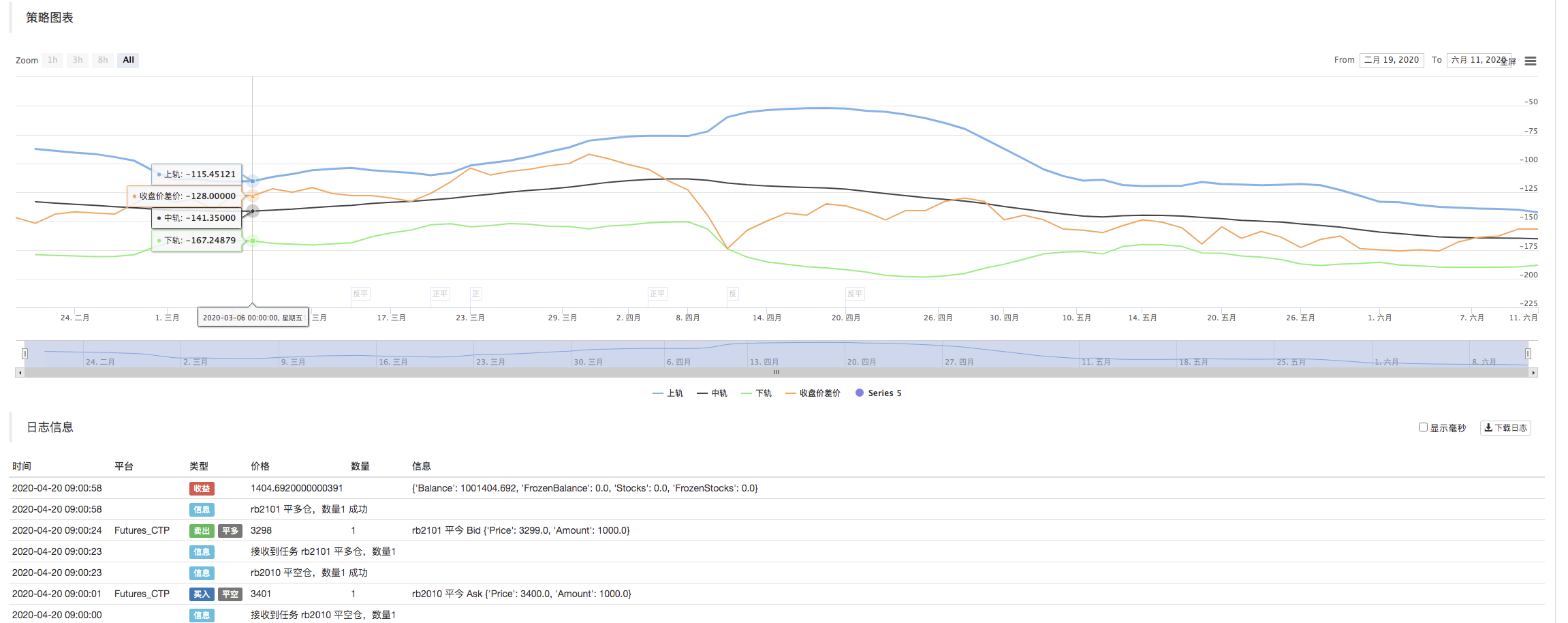

Ujian belakang:

Artikel ini digunakan terutamanya untuk tujuan kajian sahaja. Strategi lengkap:https://www.fmz.com/strategy/213826

- Menjelajah FMZ: Amalan Protokol Komunikasi Antara Strategi Dagangan Langsung

- Menjelajah FMZ: Strategi Perdagangan, Praktik Protokol Komunikasi Antar-Tandakan

- Menjelajah FMZ: Aplikasi Baru Tombol Bar Status (Bahagian 1)

- Meneroka FMZ: Aplikasi baru untuk butang status

- Pengenalan kepada Kod Sumber Strategi Dagangan Pasangan Mata Wang Digital dan API Terkini Platform FMZ

- Sumber dan API terkini untuk platform FMZ

- Penjelasan terperinci mengenai Strategi Perdagangan Pasangan Mata Wang Digital

- FMZ Quant & OKX: Bagaimana Orang Biasa Menguasai Perdagangan Kuantitatif?

- Strategi perdagangan pasangan mata wang digital terperinci

- Penjelasan terperinci FMZ Quant API Peningkatan: Meningkatkan Pengalaman Reka Bentuk Strategi

- Penjelasan terperinci mengenai ciri-ciri baru parameter antara muka strategi dan kawalan interaktif