Strategi Perdagangan Berayun Tiga Corak

Gambaran Keseluruhan

Strategi dagangan ayunan tiga corak adalah strategi dagangan jangka pendek berdasarkan gabungan beberapa penunjuk teknikal. Strategi ini menggabungkan penunjuk Super Trend, purata bergerak hibrid SSL dan penunjuk QQE yang diperbaiki untuk membentuk isyarat dagangan yang stabil. Ia sesuai untuk instrumen dagangan yang mempunyai turun naik tinggi seperti mata wang kripto dan saham, terutamanya selepas tempoh penembusan.

Prinsip

Isyarat Masuk

Masuk kedudukan panjang:

- Super Trend bertukar daripada menurun kepada menaik

- Harga penutup menembusi ke atas garisan atas purata bergerak hibrid SSL

- QQE yang diperbaiki berwarna biru (menaik)

Masuk kedudukan pendek:

- Super Trend bertukar daripada menaik kepada menurun

- Harga penutup menembusi ke bawah garisan bawah purata bergerak hibrid SSL

- QQE yang diperbaiki berwarna merah (menurun)

Isyarat Keluar

Keluar kedudukan panjang: Super Trend bertukar daripada menaik kepada menurun

Keluar kedudukan pendek: Super Trend bertukar daripada menurun kepada menaik

Henti Rugi

Boleh memilih henti rugi peratusan, henti rugi ATR atau henti rugi berdasarkan harga tertinggi/terendah terkini

Ambil Untung

Boleh menetapkan nisbah pulangan ambil untung, harga ambil untung dikira secara automatik

Pengurusan Modal

Pilihan sama ada menggunakan logik pengurusan modal untuk mengawal saiz kedudukan

Carta

- Melukis garisan Super Trend, saluran purata bergerak hibrid SSL

- Pilihan untuk melukis purata bergerak EMA

- Melukis garisan masuk, henti rugi dan ambil untung untuk kedudukan panjang dan pendek

- Melukis label masuk untuk kedudukan panjang dan pendek

Kelebihan

- Gabungan pelbagai penunjuk membentuk isyarat dagangan yang stabil

Menggabungkan penunjuk Super Trend, purata bergerak hibrid SSL dan QQE yang diperbaiki, penunjuk yang berbeza saling mengesahkan, dapat menapis penembusan palsu dan membentuk isyarat dagangan berkualiti tinggi.

- Sesuai untuk dagangan ayunan bagi instrumen yang turun naik tinggi

Strategi menggunakan kaedah dagangan jangka pendek, memberi tumpuan kepada menangkap pergerakan harga jangka sederhana dan pendek. Super Trend dapat mengesan arah aliran harga dengan berkesan, manakala purata bergerak hibrid SSL dapat mengenal pasti tahap sokongan dan rintangan dengan jelas. Gabungan kedua-duanya boleh menjana keuntungan dalam pasaran yang berayun.

- Pelbagai pilihan henti rugi dan ambil untung

Henti rugi boleh dipilih berdasarkan peratusan, nilai ATR atau harga ekstrem terkini. Ambil untung boleh menetapkan nisbah pulangan. Pengurusan modal boleh mengawal saiz kedudukan. Pengguna boleh menggabungkan secara bebas mengikut ciri instrumen dan profil risiko.

- Carta yang jelas

Carta strategi dilukis dengan jelas, memaparkan garisan henti rugi dan ambil untung secara visual. Tanda garis masuk memudahkan pengenalpastian isyarat dagangan.

Risiko dan Pengoptimuman

- Mungkin berlaku kerugian kecil

Oleh kerana menggunakan dagangan jangka pendek, kerugian kecil akibat ayunan biasa tidak dapat dielakkan sepenuhnya. Longgaran henti rugi yang sesuai dan pengoptimuman logik pengurusan modal boleh dilakukan.

- Risiko penembusan palsu

Apabila harga menunjukkan penembusan palsu, isyarat yang salah mungkin terbentuk. Boleh menguji EMA dengan tempoh yang berbeza untuk menapis penembusan palsu, atau mengoptimumkan parameter penunjuk pengesanan arah aliran.

- Risiko kegagalan penunjuk asas

Jika penunjuk asas gagal, pelbagai isyarat salah akan muncul. Perlu mengesahkan keberkesanan penunjuk secara berkala dan menyesuaikan jika masalah dikesan.

- Mengoptimumkan tempoh ujian balik

Tempoh ujian balik semasa adalah jangka masa tetap, tidak dapat menyesuaikan dengan kitaran pasaran yang berbeza bagi instrumen. Disarankan untuk mengoptimumkan kepada tempoh dagangan utama kontrak yang sepadan.

- Mengoptimumkan kesesuaian instrumen

Boleh melaraskan parameter strategi secara halus mengikut ciri data instrumen yang berbeza untuk meningkatkan kadar kemenangan kedudukan panjang dan pendek. Disarankan menggunakan kaedah pengoptimuman langkah demi langkah untuk membandingkan kesan parameter yang berbeza terhadap strategi.

Kesimpulan

Strategi ini menggunakan gabungan pelbagai penunjuk untuk membentuk isyarat dagangan, dapat menapis penembusan palsu dengan berkesan dan sesuai untuk mata wang kripto dan saham individu yang mempunyai turun naik tinggi. Pada masa yang sama, ia menawarkan pelbagai pilihan henti rugi dan ambil untung untuk dipilih, memberikan fleksibiliti. Secara keseluruhan, strategi ini membentuk isyarat dagangan yang stabil dan boleh memperoleh pulangan yang baik dalam pasaran ayunan jangka sederhana dan pendek. Dengan pengoptimuman lanjut, parameter boleh disesuaikan untuk instrumen dagangan yang berbeza, meningkatkan faktor keuntungan strategi. Strategi ini merupakan sistem dagangan yang cekap dan patut dikaji secara mendalam.

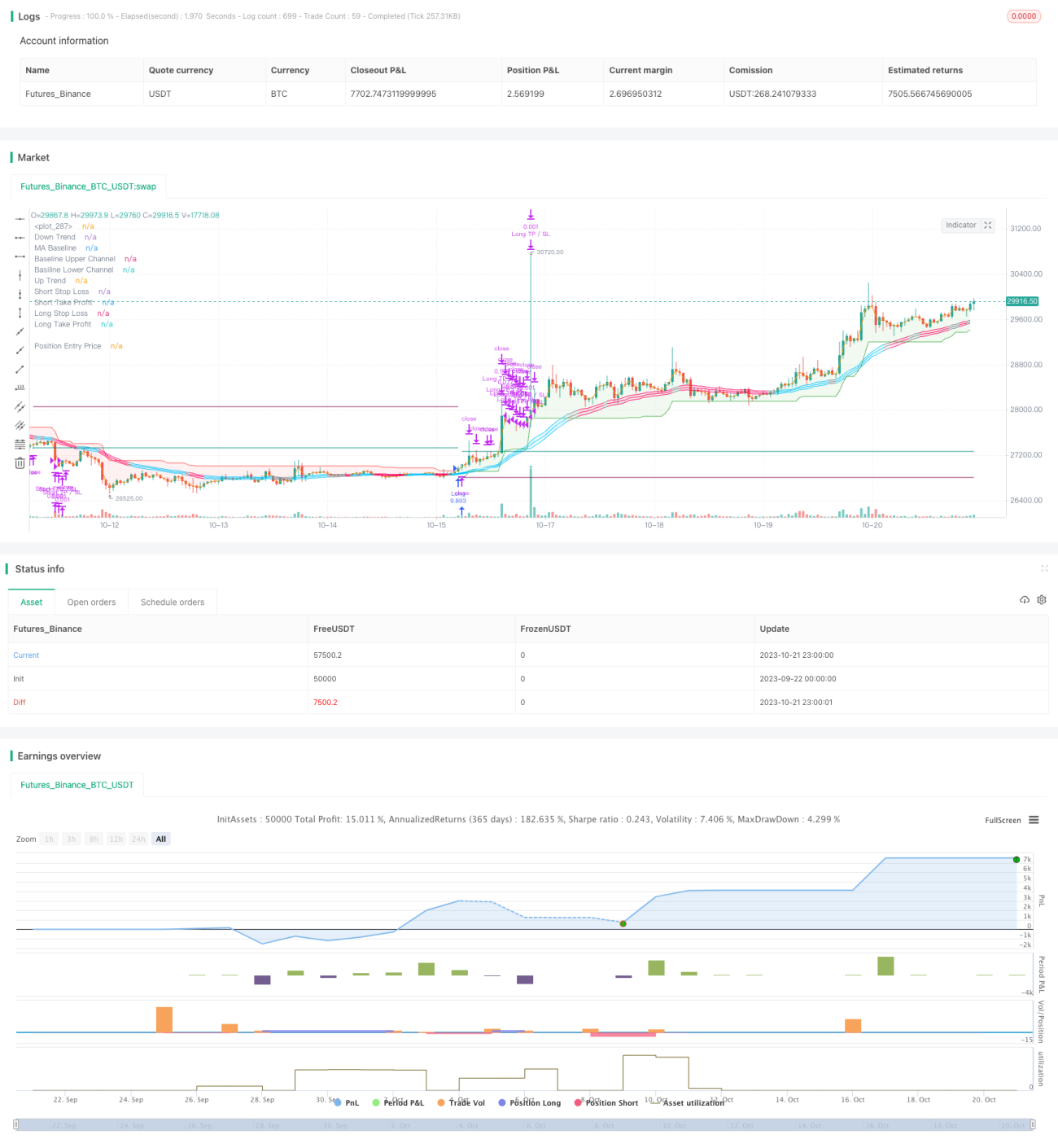

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1