Mikrofon Rosak dan Strategi Purata Bergerak Pelbagai Jangka Masa

Gambaran Keseluruhan

Strategi ini menggabungkan penggunaan indikator MACD (Moving Average Convergence Divergence) dan purata bergerak pelbagai jangka masa untuk membentuk strategi dagangan dua arah (panjang dan pendek) yang memanfaatkan isyarat arah aliran dan pembalikan arah aliran. Strategi ini dapat memperoleh keuntungan tambahan dalam pasaran yang sedang dalam arah aliran, di samping merebut peluang pembalikan.

Prinsip Strategi

-

Menggunakan dua set kombinasi EMA (Exponential Moving Average) dengan tempoh berbeza sebagai penapis pelbagai jangka masa untuk menentukan arah kenaikan atau penurunan: EMA pantas 15 minit di atas EMA perlahan 1 jam adalah penapis kenaikan (bullish filter), manakala EMA pantas 15 minit di bawah EMA perlahan 1 jam adalah penapis penurunan (bearish filter).

-

Apabila divergens MACD dikesan (divergens antara histogram dan harga), kemungkinan pembalikan akan berlaku.

-

Apabila penapis kenaikan aktif (bullish filter) dan divergens kenaikan (bullish divergence) dikesan (harga mencapai paras tinggi baharu tetapi MACD tidak mencapai paras tinggi baharu), tunggu MACD melintasi ke atas garis sifar, kemudian buka posisi panjang (long). Apabila penapis penurunan aktif (bearish filter) dan divergens penurunan (bearish divergence) dikesan (harga mencapai paras rendah baharu tetapi MACD tidak mencapai paras rendah baharu), tunggu MACD melintasi ke bawah garis sifar, kemudian buka posisi pendek (short).

-

Kaedah henti rugi (stop loss) adalah henti rugi menjejak (trailing stop loss) yang dikira berdasarkan julat pergerakan harga tertinggi dan terendah. Ambil untung (take profit) adalah gandaan tertentu daripada henti rugi.

-

Apabila histogram MACD melintasi garis sifar, posisi akan ditutup.

Analisis Kelebihan

-

Gabungan EMA pelbagai jangka masa dapat menilai arah aliran utama (trend) pada jangka masa yang lebih besar, mengelakkan dagangan menentang arah aliran.

-

Divergens MACD dapat menangkap peluang pembalikan harga, sesuai untuk strategi pembalikan.

-

Henti rugi menjejak dinamik dapat mengunci keuntungan dan mengelakkan kerugian yang lebih besar.

-

Jarak ambil untung yang dikira berdasarkan henti rugi dapat memberikan pulangan yang dijangkakan.

Analisis Risiko

-

Kombinasi EMA sebagai penilis mungkin tersilap dalam menentukan arah semasa fasa pengumpulan (sideways/consolidation).

-

Pemulihan selepas divergens MACD mungkin tidak mencukupi untuk meraih keuntungan.

-

Penetapan jarak henti rugi yang tidak sesuai mungkin terlalu longgar atau terlalu ketat.

-

Ruang pembalikan yang tidak mencukupi menyebabkan keuntungan terhad.

-

Masa masuk semasa pembalikan perlu tepat; terlampau awal atau terlambat boleh mengakibatkan kerugian.

Hala Tuju Pengoptimuman

-

Uji kombinasi parameter EMA yang berbeza untuk mendapatkan penentuan arah aliran yang lebih tepat.

-

Cuba laraskan parameter MACD kepada kombinasi yang lebih sensitif.

-

Uji nisbah henti rugi dan ambil untung yang berbeza.

-

Tambah syarat penapisan tambahan untuk mengelakkan perangkap pemulihan palsu. Contohnya, tambah penilaian arah aliran global menggunakan EMA jangka masa yang lebih tinggi.

-

Optimumkan syarat pengesahan kemasukan pembalikan untuk memastikan pembalikan sudah cukup matang.

Kesimpulan

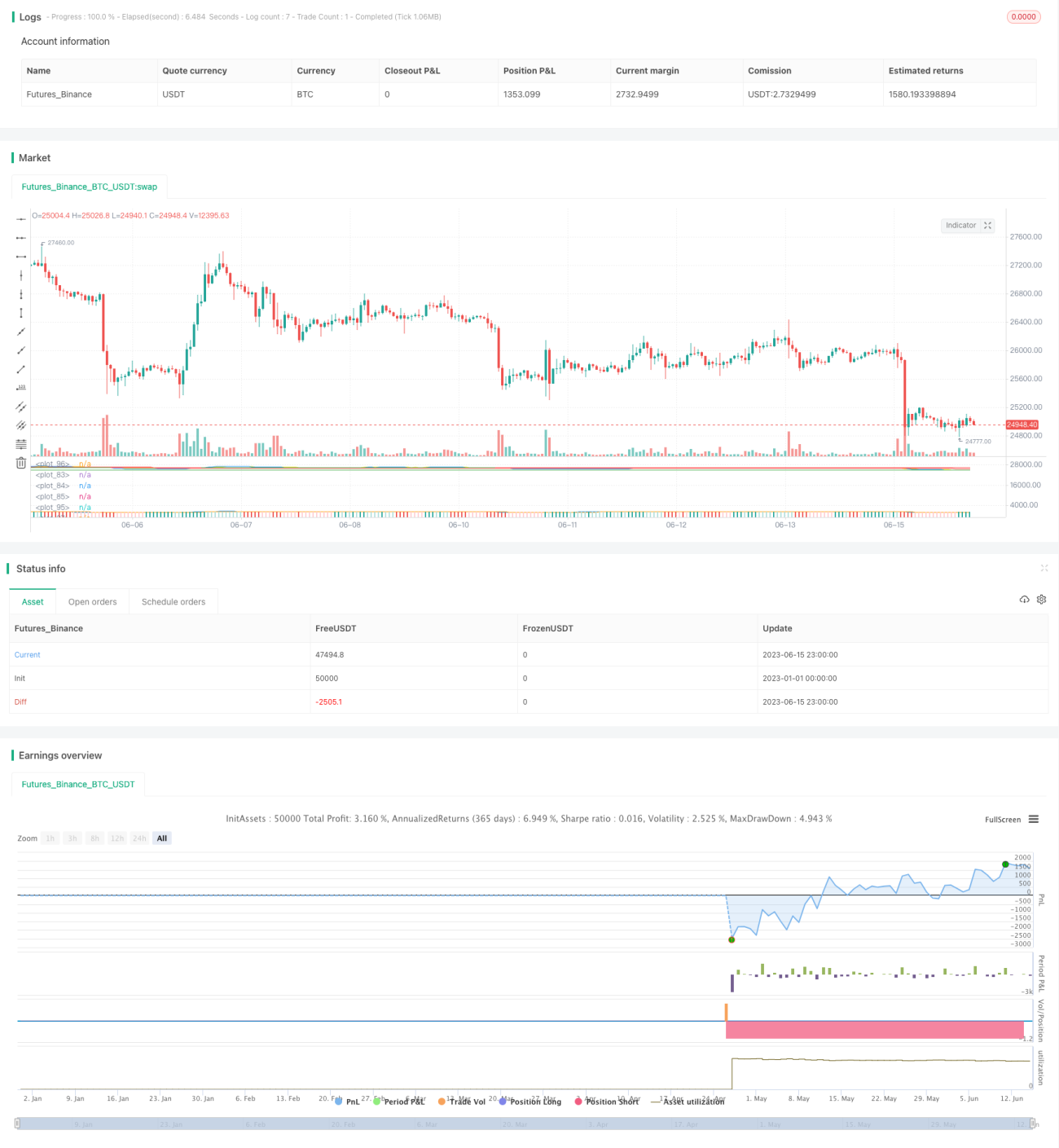

Strategi ini mengintegrasikan penapisan arah aliran, isyarat pembalikan arah aliran, dan pengurusan henti rugi serta ambil untung dinamik, membolehkan ia mengikuti arah aliran utama dan juga merebut peluang pembalikan. Dengan melaraskan parameter dan mengoptimumkan syarat penapisan, strategi ini dapat menyesuaikan diri dengan pelbagai persekitaran pasaran dan memperoleh keuntungan yang stabil dalam keadaan terkawal risiko. Strategi ini mempunyai nilai kebolehgunaan dan praktikal yang tertentu, serta merupakan contoh tipikal penggabungan pelbagai jangka masa dan indikator.

- 1