Strategi Mengikut Arah Aliran Berasaskan kNN

Gambaran Keseluruhan

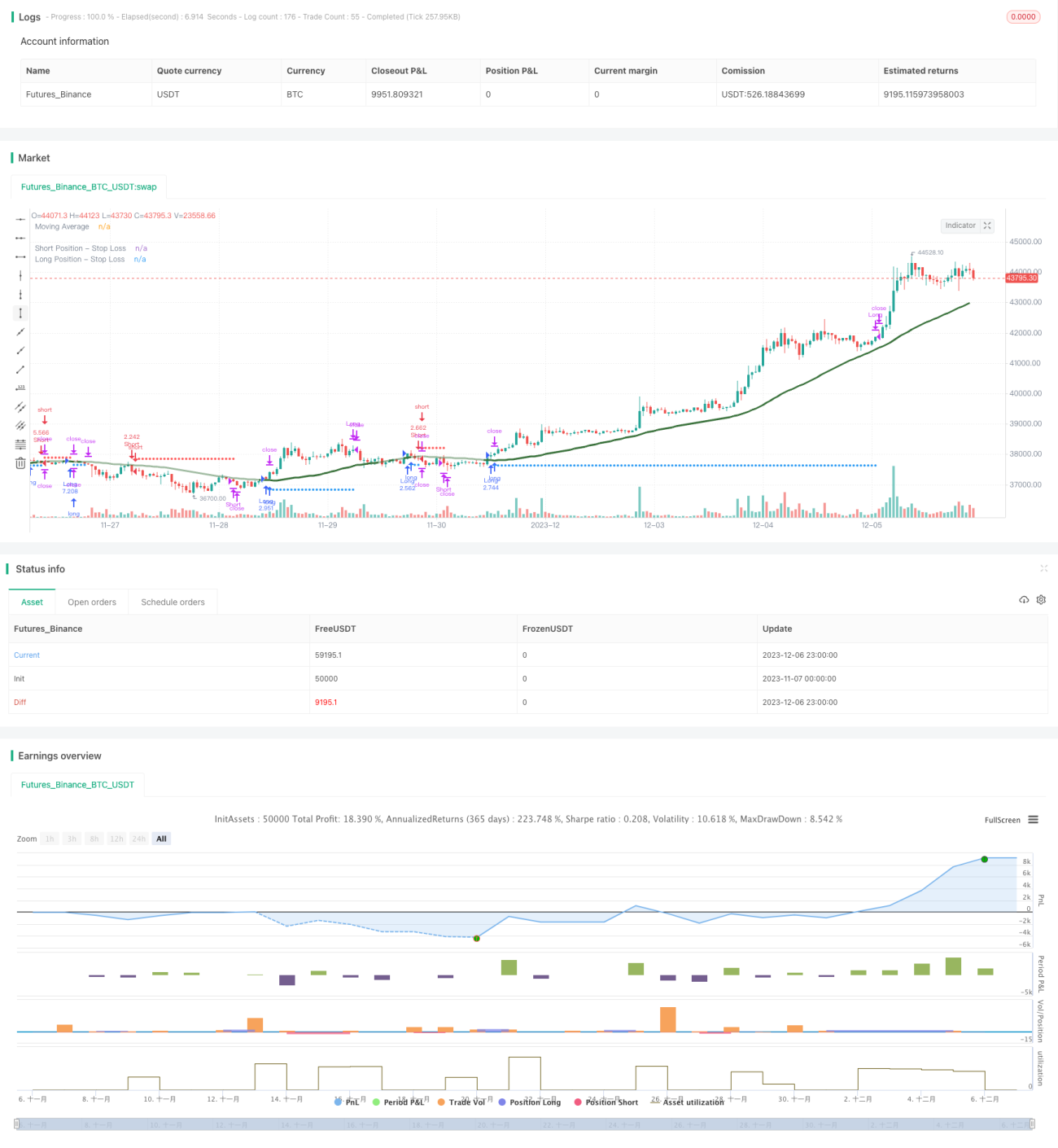

Strategi ini menggunakan algoritma pembelajaran mesin kNN (k-Nearest Neighbors) untuk meramal arah aliran pasaran dan menghasilkan isyarat beli (panjang) dan jual (pendek) berdasarkan ramalan tersebut. Strategi ini mengambil kira pelbagai faktor seperti data sejarah, penunjuk teknikal, dan melatih model kNN untuk mendapatkan ciri pasaran secara dinamik, membolehkan pelaksanaan perdagangan ikut arah aliran secara automatik.

Prinsip Strategi

-

Kumpul data latihan: mengumpul siri masa seperti harga tutup sejarah, volum dagangan, serta penunjuk teknikal seperti RSI, CCI.

-

Prapemprosesan data: menormalkan nilai penunjuk ke dalam julat 0-100.

-

Latih model kNN: masukkan dua ciri dalam model kNN semasa, hitung jarak Euclidean antara vektor ciri ini dengan vektor ciri sejarah, pilih k sampel sejarah terdekat, dan kira taburan label (panjang atau pendek) bagi k sampel tersebut.

-

Dapatkan ramalan: ramalkan arah aliran pasaran semasa berdasarkan label k sampel jiran terdekat. Jika ramalan adalah panjang, hasilkan isyarat posisi beli; jika ramalan adalah pendek, hasilkan isyarat posisi jual.

-

Gunakan penapis seperti henti rugi, kawalan saiz posisi, purata bergerak untuk melaksanakan dagangan.

Kelebihan Strategi

-

Menggunakan algoritma pembelajaran mesin untuk mengenal pasti corak teknikal secara automatik tanpa campur tangan manusia.

-

Boleh memilih penunjuk teknikal yang berbeza secara fleksibel sebagai ciri model dan mengoptimumkan strategi secara masa nyata.

-

Mengintegrasikan mekanisme kawalan risiko yang ketat seperti henti rugi dan pengurusan saiz posisi.

-

Mempersembahkan garis henti rugi secara visual, jelas dan intuitif.

Risiko dan Penyelesaian

-

Ramalan pembelajaran mesin mungkin menghasilkan isyarat palsu. Pilih nilai k, vektor ciri, dan julat masa sampel yang sesuai untuk mengoptimumkan model.

-

Dagangan sebelah pihak (satu arah) mempunyai risiko yang berpotensi. Boleh tambah kebenaran dagangan dua hala dalam kod untuk menghapuskan bug.

-

Penetapan parameter yang tidak sesuai boleh menyebabkan dagangan berlebihan. Laraskan parameter seperti saiz posisi dan kekerapan dagangan dengan sewajarnya.

Arah Pengoptimuman

-

Uji pelbagai jenis penunjuk teknikal sebagai ciri input kNN.

-

Cuba kaedah pengukuran jarak lain, seperti jarak Manhattan.

-

Gunakan jarak sampel atau kualiti klasifikasi untuk melaraskan saiz posisi.

-

Tambah pembahagian set latihan dan set ujian untuk melaksanakan pengoptimuman bergulir.

Ringkasan

Strategi ini menggunakan algoritma kNN klasik untuk meramal arah aliran pasaran dan menjalankan dagangan ikut arah aliran berdasarkan isyarat ramalan. Strategi ini mempunyai ciri parameter boleh laras dan risiko terkawal, menyediakan penyelesaian dagangan automatik yang berkesan kepada pengguna. Pengguna boleh meningkatkan prestasi strategi dengan melaraskan kombinasi penunjuk teknikal dan mengoptimumkan hiperparameter model secara berterusan.

- 1