Strategi Robot Tersuai Boleh Skala HTF MACD MFI Tidak Melukis Semula

Gambaran Keseluruhan

Strategi ini adalah strategi gabungan indikator MACD dan MFI yang tidak melukis semula dan sangat boleh disesuaikan, sesuai untuk robot dagangan algoritma. Ia menggabungkan indikator trend dan indikator momentum, dan menghasilkan isyarat dagangan melalui pelbagai penapis.

Prinsip Strategi

Strategi ini menggunakan indikator MACD untuk menilai arah trend pasaran. MACD ialah indikator momentum jenis pengesanan trend, yang diperoleh dengan menolak purata bergerak perlahan daripada purata bergerak pantas untuk mendapatkan histogram MACD, dan kemudian menggunakan purata bergerak eksponen MACD untuk mendapatkan garis isyarat. Apabila garis cepat menembusi ke atas garis perlahan, ia adalah isyarat beli; apabila menembusi ke bawah, ia adalah isyarat jual.

Selain itu, strategi ini juga menggunakan indikator MFI untuk menilai keadaan terlebih beli atau terlebih jual pasaran. Indikator MFI menggabungkan maklumat harga dan volum, dengan nilai berayun antara 0 hingga 100. MFI di bawah 20 adalah zon terlebih jual, manakala di atas 80 adalah zon terlebih beli.

Untuk menapis isyarat palsu, strategi ini turut menambah penapis trend dan penapis RSI. Apabila harga berada dalam trend menaik dan RSI kurang daripada ambang yang ditetapkan, isyarat beli dihasilkan.

Kelebihan Strategi

- Menggabungkan pelbagai indikator untuk menilai keadaan pasaran secara menyeluruh, meningkatkan kadar kemenangan

- Menambah mekanisme penapis untuk mengelakkan isyarat palsu, mengurangkan dagangan yang tidak perlu

- Pelbagai parameter dan penapis boleh dikonfigurasikan sendiri, sesuai untuk instrumen dan pilihan dagangan yang berbeza

- Boleh digunakan untuk dagangan manual, atau disambungkan ke robot algoritma untuk dagangan berprogram

Risiko Strategi dan Penyelesaian

-

Penetapan parameter indikator yang tidak sesuai mudah menghasilkan isyarat palsu

-

Boleh menguji parameter yang berbeza untuk memilih kombinasi parameter yang optimum

-

Parameter tidak universal untuk pelbagai instrumen, perlu diuji dan dioptimumkan secara berasingan

-

Kekerapan dagangan mungkin terlalu tinggi, meningkatkan kos dagangan dan risiko slippage

-

Boleh melaraskan penapis untuk mengurangkan kekerapan dagangan

-

Semasa dagangan sebenar, perhatikan kawalan kos

Arah Pengoptimuman Strategi

- Menguji tempoh data yang lebih panjang untuk menilai kestabilan parameter

- Mencuba kombinasi parameter indikator yang berbeza

- Mengoptimumkan pemberat indikator untuk meningkatkan kestabilan strategi

- Menambah lebih banyak penapis untuk mengurangkan dagangan yang tidak perlu

Kesimpulan

Strategi ini adalah strategi pengesanan trend yang sangat boleh disesuaikan, menggabungkan indikator trend dan momentum untuk menilai keadaan pasaran, dan menggunakan mekanisme penapis dengan berkesan untuk mengawal risiko. Ia boleh digunakan untuk dagangan manual, atau disambungkan ke robot algoritma untuk merealisasikan dagangan berprogram dengan automasi yang tinggi. Ia merupakan sistem strategi yang layak untuk penjejakan dan pengoptimuman jangka panjang.

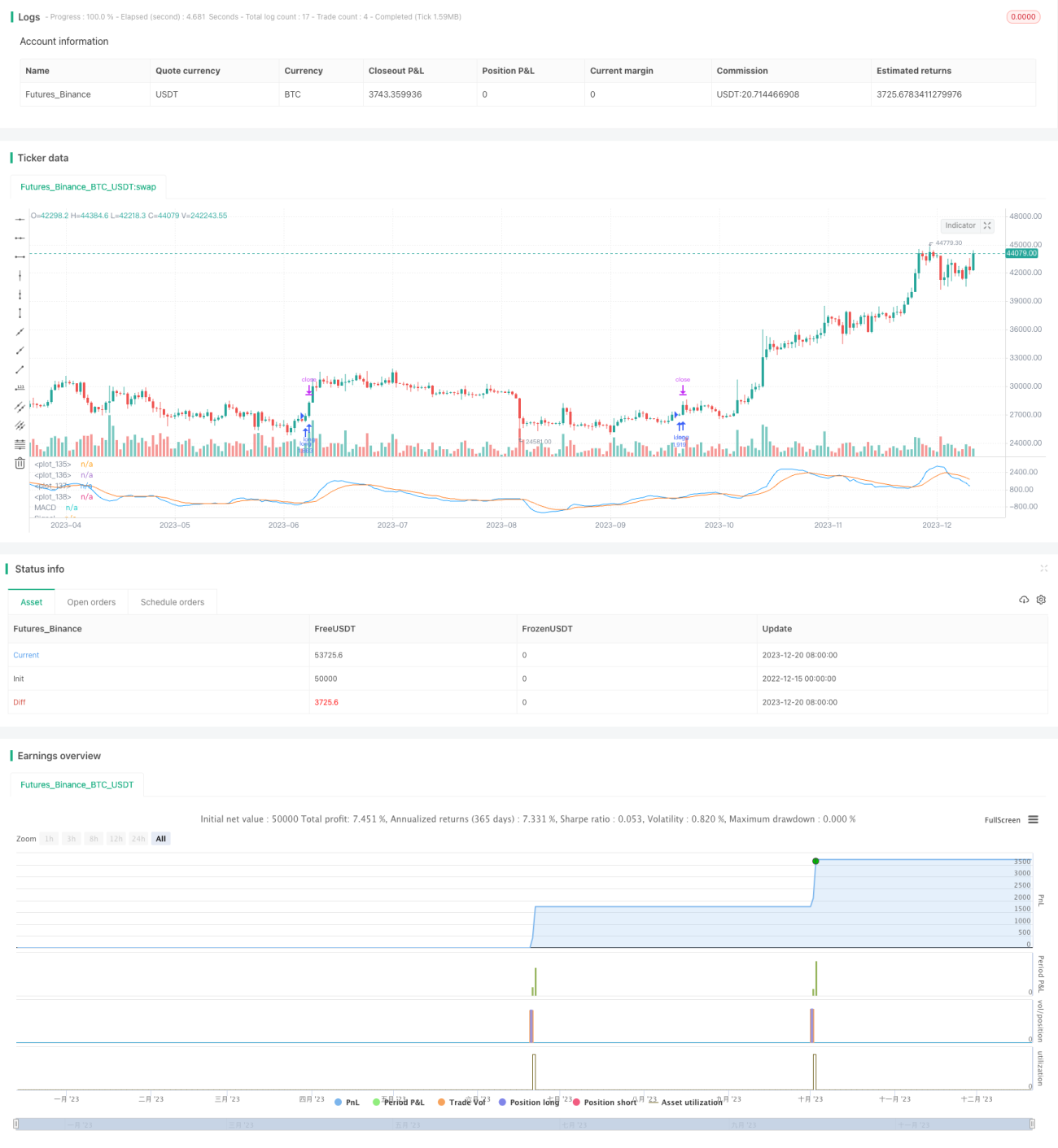

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1