Strategi Perdagangan Kuantitatif Berasaskan Penapis Trend Dwi

Gambaran Keseluruhan

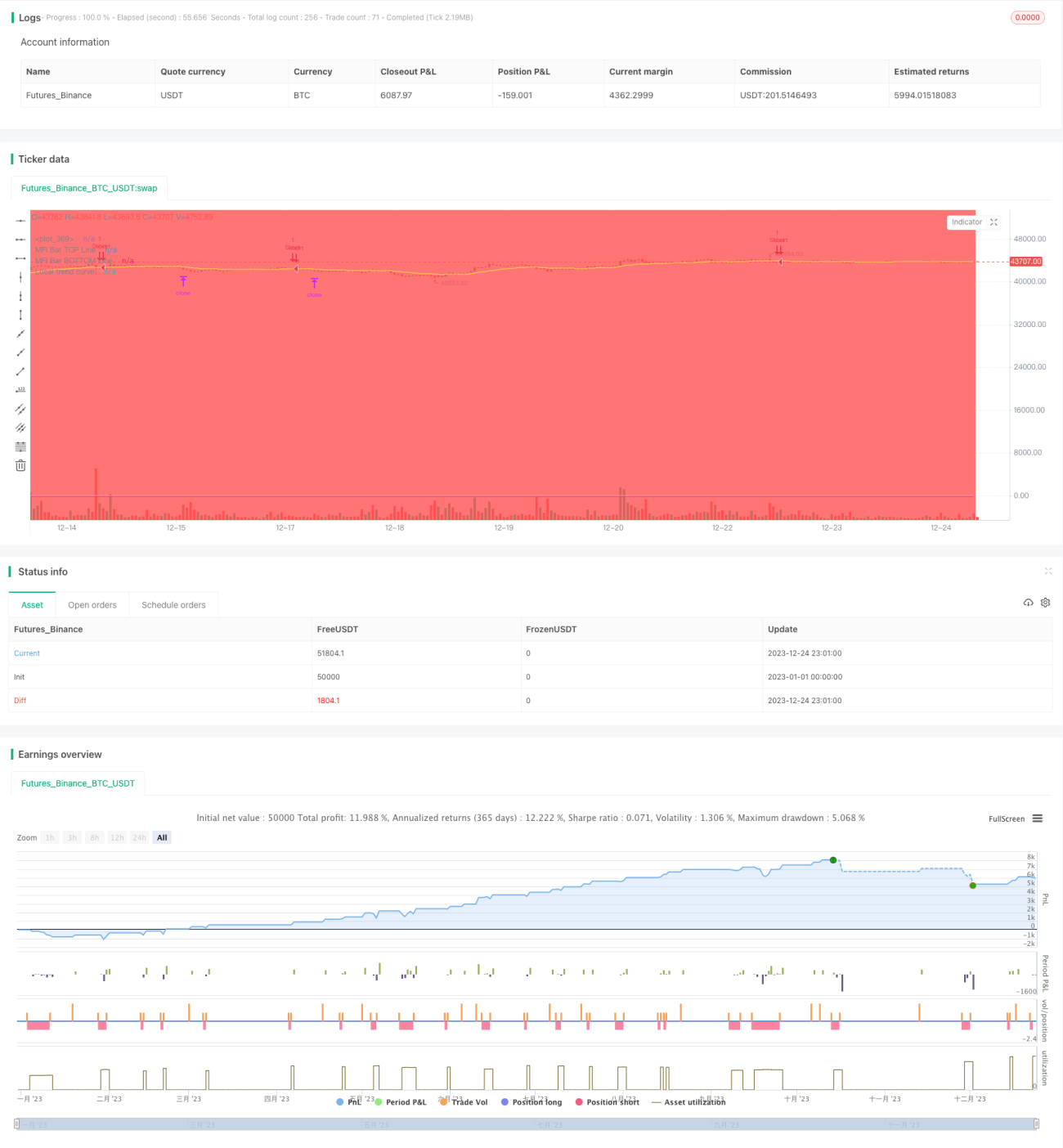

Ini adalah strategi perdagangan kuantitatif yang menggunakan dua penapis arah aliran. Strategi ini menggabungkan penapis arah aliran global dan penapis arah aliran tempatan, memastikan hanya membuka kedudukan apabila arah aliran adalah betul. Selain itu, strategi ini menetapkan beberapa syarat penapisan lain seperti penapis RSI, penapis harga, penapis kecerunan, dan lain-lain untuk meningkatkan lagi kebolehpercayaan isyarat perdagangan. Dari segi keluar, strategi ini telah menetapkan harga henti rugi dan harga ambil untung. Secara keseluruhan, ini adalah strategi perdagangan kuantitatif yang stabil dan tepat.

Prinsip Strategi

Logik teras strategi ini berdasarkan penapis arah aliran berganda. Penapis arah aliran global menggunakan EMA jangka panjang untuk menilai arah aliran keseluruhan pasaran, manakala penapis arah aliran tempatan menggunakan EMA jangka pendek untuk menilai arah aliran tempatan. Kedudukan hanya dibuka apabila kedua-duanya bersetuju dengan arah aliran.

Secara khusus, strategi ini mengira garis EMA BTCUSDT untuk menentukan sama ada pasaran keseluruhan berada dalam arah aliran menaik atau menurun - ini adalah penapis arah aliran global. Pada masa yang sama, strategi mengira garis EMA kontrak ini untuk menentukan arah aliran pasaran tempatan - ini adalah penapis arah aliran tempatan. Apabila kedua-duanya bersetuju dengan arah aliran, digabungkan dengan beberapa penapis bantuan lain, strategi akan menghasilkan isyarat perdagangan dan menetapkan harga ambil untung dan henti rugi sebelum membuka kedudukan.

Selepas menentukan isyarat perdagangan, strategi akan segera membuka kedudukan. Pada masa yang sama, strategi telah menetapkan harga ambil untung dan harga henti rugi. Apabila harga mencapai ambil untung atau henti rugi, strategi akan secara automatik menutup kedudukan.

Analisis Kelebihan

Ini adalah strategi perdagangan kuantitatif yang stabil dan boleh dipercayai, dengan kelebihan utama:

-

Menggunakan mekanisme penapis arah aliran berganda, yang dapat menapis kebanyakan isyarat palsu, menjadikan isyarat perdagangan lebih boleh dipercayai dan tepat.

-

Menggabungkan beberapa penapis bantuan seperti penapis RSI, penapis harga, dan lain-lain, meningkatkan lagi kualiti isyarat.

-

Mengira secara automatik harga ambil untung dan henti rugi, tanpa perlu pemantauan manual, mengurangkan risiko perdagangan.

-

Parameter strategi boleh disesuaikan, sesuai untuk lebih banyak instrumen perdagangan, dengan kebolehsuaian yang kuat.

-

Logik strategi jelas dan mudah difahami, memudahkan pengoptimuman dan penambahbaikan, dengan ruang pengembangan yang luas.

Analisis Risiko

Walaupun strategi ini mempunyai banyak kelebihan, ia masih mempunyai risiko perdagangan tertentu, terutamanya tertumpu pada:

-

Ketepatan masa masuk yang tidak tepat dari penapis arah aliran berganda. Boleh dioptimumkan dengan melaraskan parameter penapis.

-

Penetapan harga ambil untung dan henti rugi yang tidak tepat, mungkin menyebabkan ambil untung atau henti rugi terlalu awal. Boleh diuji dengan kombinasi parameter yang berbeza untuk mencari penyelesaian optimum.

-

Pemilihan instrumen perdagangan dan jangka masa yang tidak sesuai boleh menyebabkan strategi tidak berkesan. Disyorkan untuk melakukan penalaan dan ujian parameter secara berasingan untuk setiap instrumen perdagangan.

-

Terdapat risiko overfitting. Perlu diuji dalam lebih banyak persekitaran pasaran untuk memastikan keteguhan strategi.

Arah Pengoptimuman

Strategi ini boleh dioptimumkan dari beberapa arah berikut:

-

Melaraskan parameter penapis berganda untuk mencari kombinasi parameter terbaik;

-

Menguji dan memilih penapis bantuan yang terbaik;

-

Mengoptimumkan algoritma ambil untung dan henti rugi untuk menjadikannya lebih pintar;

-

Mencuba memperkenalkan kaedah pembelajaran mesin untuk mencapai pelarasan parameter dinamik strategi;

-

Menguji dalam lebih banyak instrumen perdagangan dan jangka masa yang lebih panjang untuk meningkatkan kestabilan strategi.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi perdagangan kuantitatif yang stabil, tepat, dan mudah dioptimumkan. Ia menggunakan penapis arah aliran berganda digabungkan dengan beberapa penapis bantuan untuk menghasilkan isyarat perdagangan, dapat menapis kebanyakan bunyi, menjadikan isyarat lebih tepat dan boleh dipercayai. Pada masa yang sama, strategi ini mempunyai penetapan ambil untung dan henti rugi terbina dalam, dapat mengurangkan risiko perdagangan. Ini adalah strategi yang sangat bernilai praktikal, yang selepas dioptimumkan dan disahkan, boleh digunakan secara langsung dalam perdagangan sebenar. Ia juga mempunyai potensi pengembangan yang besar, merupakan strategi kuantitatif yang layak untuk dikaji secara mendalam.

- 1