Strategi Pengikut Trend Purata Bergerak Berasaskan SSL

Gambaran Keseluruhan

Strategi ini menggunakan penunjuk saluran SSL untuk menilai arah pasaran dan mengikuti trend berdasarkan purata bergerak. Ia sesuai untuk carta 4 jam dan harian jangka sederhana hingga panjang.

Prinsip Strategi

-

Saluran SSL terdiri daripada purata bergerak Keltner dan amplitud sebenar. Ia boleh menentukan arah arah aliran pasaran. Apabila harga menembusi jalur atas, ia adalah isyarat kenaikan; apabila menembusi jalur bawah, ia adalah isyarat penurunan.

-

Strategi ini menggunakan penunjuk purata bergerak seperti EMA untuk mengira garis purata asas. Garis ini boleh menapis sebahagian penembusan palsu.

-

Strategi akan membeli apabila harga menembusi garis atas SSL, dan menjual apabila harga menembusi garis bawah SSL. Ia mengejar kenaikan dalam arah aliran menaik dan menangkap penurunan dalam arah aliran menurun.

-

Kaedah henti rugi termasuk peratusan henti rugi, ATR henti rugi, dan henti rugi berdasarkan harga terendah/tertinggi terkini. Ambil untung adalah N kali ganda henti rugi. Parameter khusus ditentukan oleh pengguna.

Analisis Kelebihan

-

Saluran SSL menentukan arah arah aliran dengan tepat, mengurangkan isyarat palsu. Digabungkan dengan purata bergerak sebagai asas kemasukan, mengelakkan pembelian di puncak dan penjualan di dasar.

-

Boleh memilih pelbagai jenis purata bergerak secara fleksibel, sesuai untuk pelbagai keadaan pasaran.

-

Kaedah henti rugi yang fleksibel dan pelbagai, mengawal risiko. Gandaan ambil untung juga boleh ditetapkan secara fleksibel untuk memenuhi keutamaan yang berbeza.

-

Boleh mengambil kedua-dua posisi beli dan jual secara serentak, memanfaatkan sepenuhnya peluang dua hala pasaran.

Analisis Risiko

-

Semua penunjuk purata bergerak mempunyai kelewatan, yang boleh menyebabkan pengumpulan kerugian.

-

Dalam pasaran berayun, penembusan baru jalur atas/bawah boleh diterbalikkan dengan cepat, menyebabkan kerugian.

-

Henti rugi ATR dan berdasarkan harga terkini mungkin terlalu longgar semasa penembusan luar biasa, menyebabkan kerugian yang lebih besar.

Langkah mengatasi risiko:

- Laraskan parameter purata bergerak dengan sesuai, atau pilih jenis purata bergerak lain.

- Besarkan jarak henti rugi, henti rugi tepat pada masanya.

- Tambah faktor gandaan dalam ATR, atau laraskan tempoh semakan semula.

Arah Pengoptimuman

- Uji lebih banyak jenis penunjuk purata bergerak untuk mencari parameter terbaik.

- Optimumkan parameter tempoh ATR untuk henti rugi.

- Uji parameter gandaan henti rugi yang berbeza.

- Uji pekali risiko ambil untung yang berbeza.

Kesimpulan

Strategi ini menggabungkan penggunaan SSL untuk menilai arah aliran dan penunjuk purata bergerak untuk mengesahkan kemasukan, membolehkan pengikut trend yang berkesan. Ia menyediakan kaedah henti rugi dan ambil untung yang fleksibel, mengawal risiko sambil memperoleh pulangan yang lebih tinggi. Melalui ujian dan pengoptimuman parameter yang berterusan, prestasi dagangan yang lebih baik dapat dicapai. Ia adalah strategi yang berkesan yang patut diikuti dan digunakan dalam jangka masa panjang.

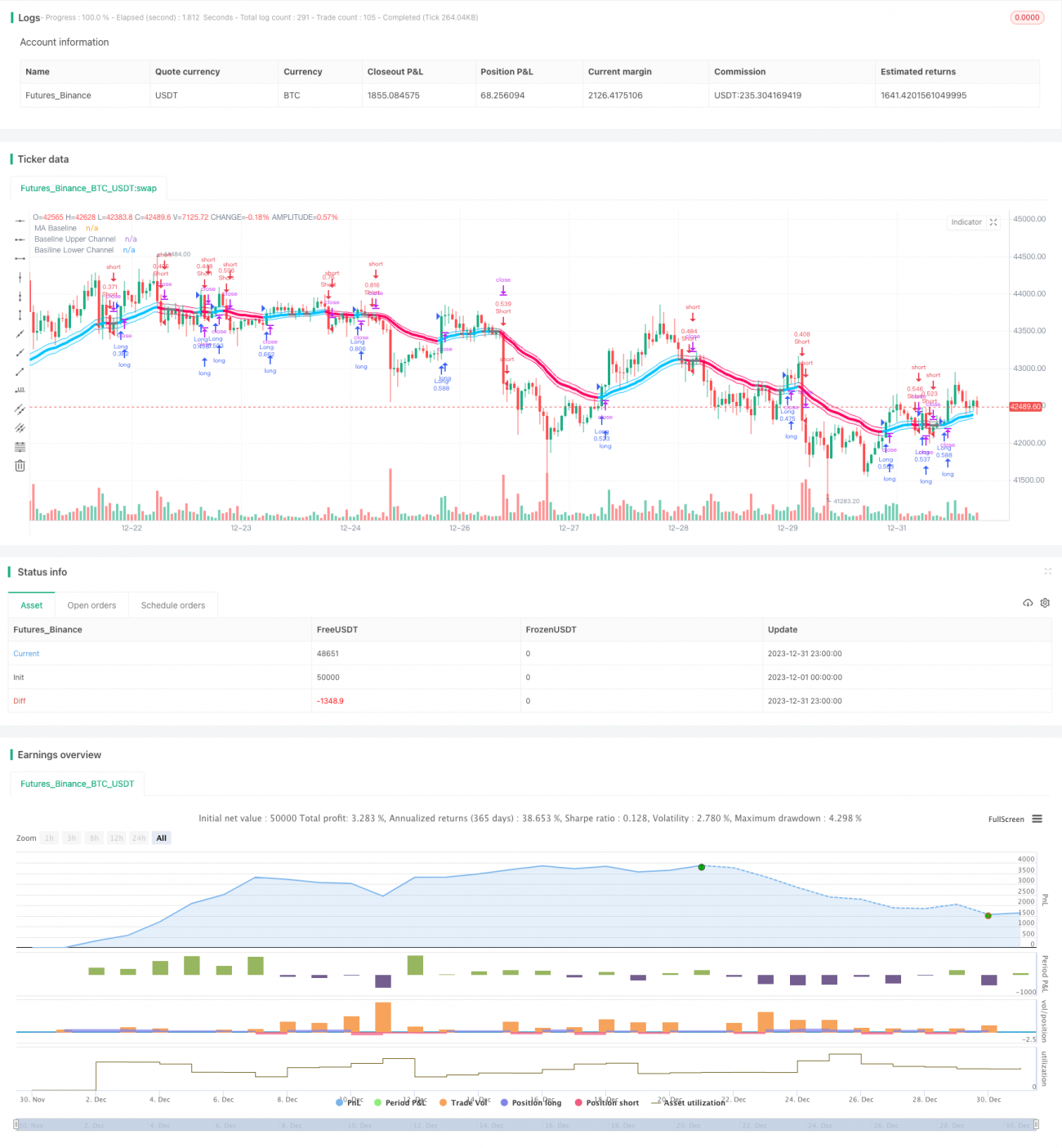

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1