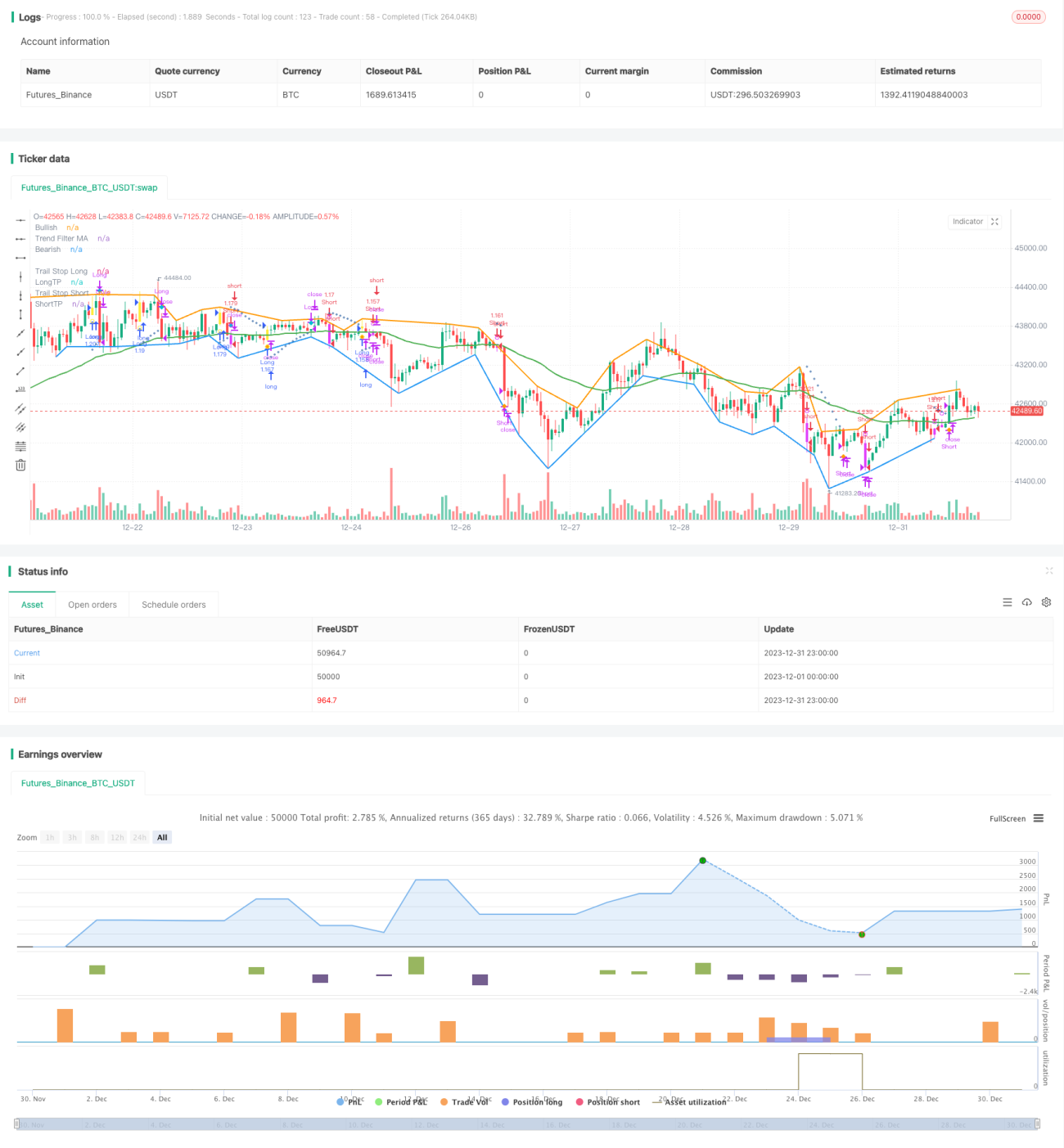

Strategi Perdagangan Indeks MACD Pelbagai Kitaran

Gambaran Keseluruhan

Strategi ini berdasarkan indikator MACD klasik, sambil menggabungkan pelbagai bantuan seperti indikator penentuan arah aliran, kaedah henti rugi dan kaedah ambil untung, membentuk strategi dagangan pengikut arah aliran yang agak lengkap. Ia boleh digunakan untuk mata wang kripto, serta dagangan forex dan saham.

Prinsip Strategi

-

Penentuan Indikator MACD

- Perbezaan antara EMA tempoh FASTLENGTH dan EMA tempoh SLOWLENGTH membentuk bar MACD

- EMA tempoh MACDLENGTH melicinkan bar MACD untuk membentuk garis MACD

- Bar MACD menembusi paksi 0 membentuk isyarat beli/jual

-

Penentuan Arah Aliran

- ADX: Indikator Purata Arah, menentukan sama ada terdapat arah aliran

- MA: Purata Bergerak, harga di atas/bawah MA membentuk arah aliran

- SAR: Parabolik SAR, SAR bergerak di atas/bawah harga untuk menentukan arah aliran

-

Kaedah Henti Rugi

- Henti rugi peratusan ATR: Menetapkan peratusan henti rugi berdasarkan faktor ATR

- Henti rugi SAR: Parabolik bertindak sebagai henti rugi selepas masuk

-

Kaedah Ambil Untung

- Jarak ambil untung tetap ATR: Menetapkan jarak ambil untung tetap berdasarkan faktor ATR

- Ambil untung peratusan: Menetapkan jarak ambil untung peratusan

-

Henti Rugi Masa

- Boleh ditetapkan untuk henti rugi selepas bilangan bar yang ditentukan

Analisis Kelebihan

-

Pelbagai Bantuan Penentuan

- Menggabungkan penentuan arah aliran dan sokongan/rintangan, dapat mengurangkan isyarat palsu

- Henti rugi ATR/SAR, mengawal risiko dengan lebih menyeluruh

-

Boleh Dikonfigurasi Secara Fleksibel

- Boleh memilih sama ada menggunakan penapisan arah aliran

- Boleh memilih henti rugi ATR atau SAR

- Boleh memilih ambil untung ATR atau standard

- Parameter boleh dikonfigurasi secara fleksibel

-

Menyediakan Analisis Perbezaan

- Menunjukkan perbezaan positif/negatif sejarah

- Menyediakan petunjuk teks

-

Memudahkan Pengoptimuman dan Pelarasan

- Strategi dilengkapi dengan banyak parameter yang boleh dikonfigurasi

- Boleh menguji kombinasi pembolehubah yang berbeza dengan mudah

Analisis Risiko

-

Parameter yang Tidak Sesuai Boleh Meningkatkan Kerugian

- Parameter ATR, SAR yang tidak sesuai boleh menyebabkan henti rugi terlalu awal

- Nisbah ambil untung yang terlalu besar boleh menyebabkan ambil untung terlalu awal

-

Risiko Kegagalan Penentuan Arah Aliran

- Parameter indikator arah aliran yang tidak sesuai boleh menyebabkan penentuan yang salah

- Kejadian luar jangka boleh menjejaskan keberkesanan penentuan arah aliran

-

Risiko Henti Rugi Masa

- Menetapkan henti rugi masa tetap mempunyai risiko kerugian

Arah Pengoptimuman

- Laraskan parameter ATR, SAR untuk menjadikan henti rugi lebih lancar

- Uji kitaran MA yang berbeza untuk mengoptimumkan penentuan arah aliran

- Uji dan laraskan nisbah ambil untung untuk mengoptimumkan kadar pulangan

- Gabungkan indikator turun naik untuk mengoptimumkan parameter

Kesimpulan

Strategi ini mempertimbangkan pelbagai sudut seperti penentuan arah aliran, henti rugi dan ambil untung, pengenalan perbezaan, membentuk strategi dagangan mata wang kripto yang agak menyeluruh. Ia menggabungkan kelebihan indikator MACD, menambah penapisan arah aliran untuk mengelakkan transaksi yang salah; menambah henti rugi ATR/SAR untuk mengawal risiko dengan lebih baik; pengenalan perbezaan menyediakan rujukan tambahan. Pelbagai parameter yang boleh dikonfigurasi membolehkan ujian dan pengoptimuman dengan mudah. Secara keseluruhan, strategi ini boleh menjadi contoh yang baik untuk penyelidikan strategi mata wang kripto.

- 1