Strategi Kuantitatif Pengesanan Trend Berasaskan Indikator Hull dan Indikator LSMA

Gambaran Keseluruhan

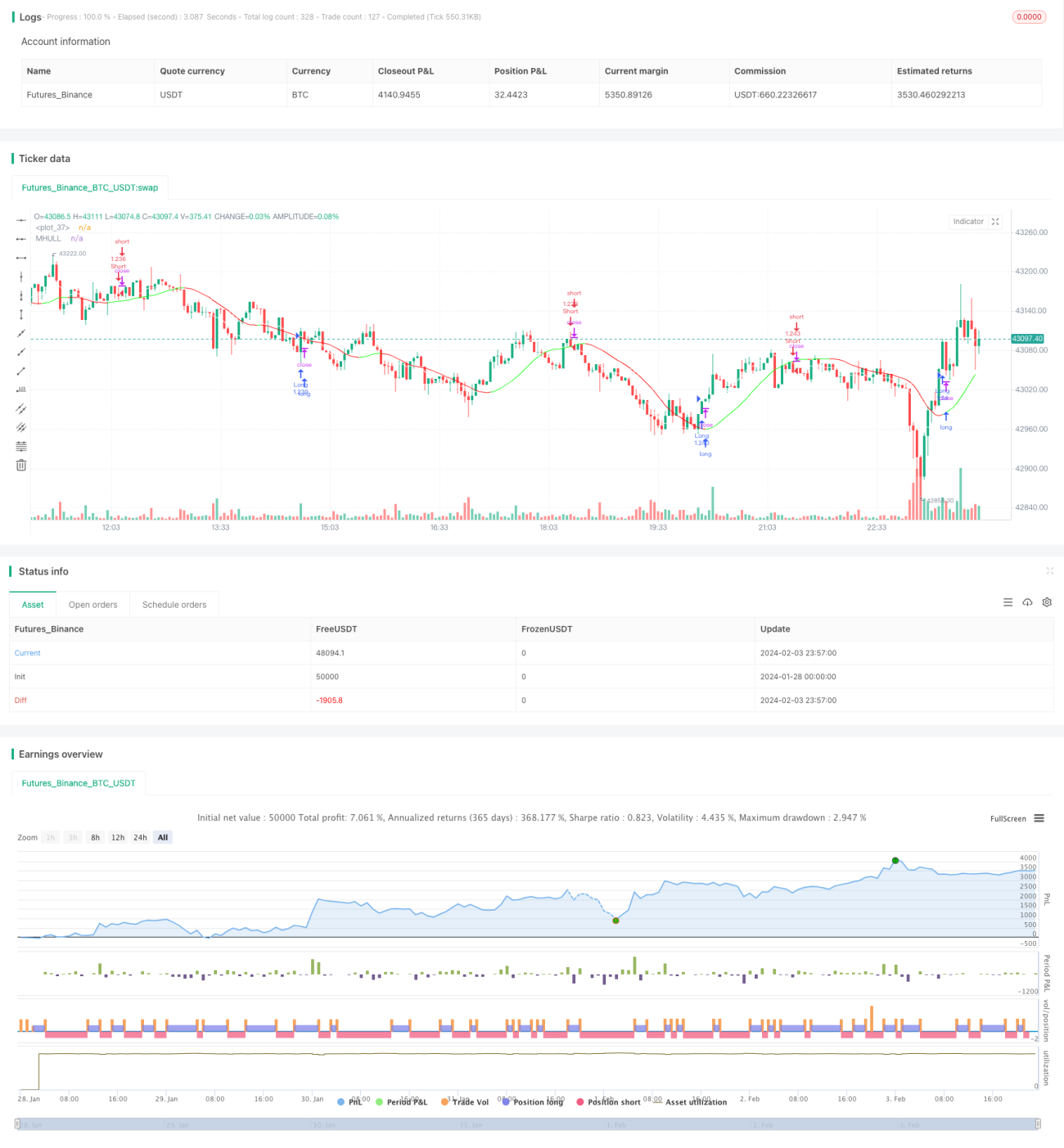

Strategi ini mengesan arah aliran dan titik pembalikan arah aliran dengan menggabungkan indikator Hull dan LSMA (Purata Pergerakan Kuasa Dua Terkecil) untuk melaksanakan penjejakan arah aliran. Apabila indikator Hull menunjukkan arah aliran menaik dan LSMA menembusi ke atas indikator Hull, posisi beli (long) diambil; apabila indikator Hull menunjukkan arah aliran menurun dan LSMA menembusi ke bawah indikator Hull, posisi jual (short) diambil. Strategi ini sesuai untuk dagangan frekuensi sederhana rendah dan boleh digunakan dalam jangka masa 1 minit.

Prinsip Strategi

- Indikator Hull digunakan untuk menentukan arah aliran nilai. Apabila garis tengah (MHULL) berada di atas garis bawah (LHULL), ia menunjukkan arah aliran menaik; sebaliknya, ia menunjukkan arah aliran menurun.

- Indikator LSMA digunakan untuk mengenal pasti titik pembalikan arah aliran. Apabila LSMA menembusi ke atas MHULL, ia menunjukkan arah aliran menaik terbentuk atau dipercepatkan; apabila LSMA menembusi ke bawah MHULL, ia menunjukkan arah aliran menurun terbentuk atau dipercepatkan.

- Menggabungkan kedua-duanya: apabila indikator Hull menunjukkan arah aliran menaik (MHULL > LHULL) dan LSMA menembusi ke atas MHULL, ambil posisi beli; apabila indikator Hull menunjukkan arah aliran menurun (MHULL < LHULL) dan LSMA menembusi ke bawah MHULL, ambil posisi jual.

- Henti rugi (stop loss) ditetapkan pada titik ayunan (swing point) terdekat. Henti rugi untuk posisi beli ialah titik terendah terkini, manakala henti rugi untuk posisi jual ialah titik tertinggi terkini.

Analisis Kelebihan

Strategi ini mempunyai kelebihan berikut:

- Indikator Hull bertindak balas dengan cepat, mampu menangkap perubahan arah aliran dengan segera; LSMA licin dan kuat, memberikan isyarat pembalikan yang tepat dan boleh dipercayai. Gabungan kedua-duanya berkesan.

- Penembusan LSMA digunakan untuk menapis isyarat palsu yang dinilai oleh indikator Hull, mengurangkan kebarangkalian perdagangan yang salah.

- Penggunaan titik ayunan sebagai tahap henti rugi melindungi modal dengan maksimum.

- Sesuai untuk dagangan frekuensi sederhana rendah, boleh digunakan dalam jangka masa 1 minit atau lebih rendah, mempunyai kebolehgunaan yang luas.

Analisis Risiko

Strategi ini juga mempunyai beberapa risiko:

- Dalam pasaran yang berayun (sideways), indikator Hull dan LSMA mungkin menghasilkan banyak persilangan yang menyebabkan perdagangan terlalu kerap. Parameter perlu disesuaikan untuk mengurangkan kekerapan perdagangan.

- Henti rugi yang ditetapkan pada titik ayunan mungkin dicetuskan oleh pelarasan harga jangka pendek. Jarak henti rugi perlu dilebarkan dengan sesuai.

- Oleh kerana sifat ketinggalan (lag) indikator LSMA, mungkin terdapat risiko salah penilaian yang sedikit. Indikator lain seperti corak lilin (candlestick) harus digunakan untuk pengesahan.

Hala Tuju Pengoptimuman

Strategi ini boleh dioptimumkan dari aspek berikut:

- Mengoptimumkan parameter indikator Hull dan LSMA agar gabungannya lebih sesuai dengan instrumen dan jangka masa yang berbeza.

- Menambah penapis berdasarkan turun naik (volatility), volum dagangan, dan lain-lain untuk mengelakkan perdagangan salah semasa pasaran berayun.

- Menambah algoritma pembelajaran mesin sebagai bantuan untuk menentukan kecenderungan arah aliran.

- Menggabungkan teknologi seperti pembelajaran mendalam untuk mengenal pasti kawasan sokongan dan rintangan utama, menjadikan henti rugi lebih munasabah.

Kesimpulan

Strategi ini menggunakan gabungan indikator Hull dan LSMA untuk menilai perubahan arah aliran dan melaksanakan dagangan penjejakan arah aliran. Kelebihannya adalah operasi yang mudah, respons yang pantas, dan boleh digunakan secara meluas dalam dagangan kuantitatif frekuensi sederhana rendah. Dengan pengoptimuman lanjut pada penapis, bantuan penilaian, dan algoritma henti rugi, strategi ini dijangka mencapai prestasi yang lebih baik.

- 1