Strategi Perdagangan Kuantitatif Berdasarkan Pelbagai Faktor

Gambaran Keseluruhan

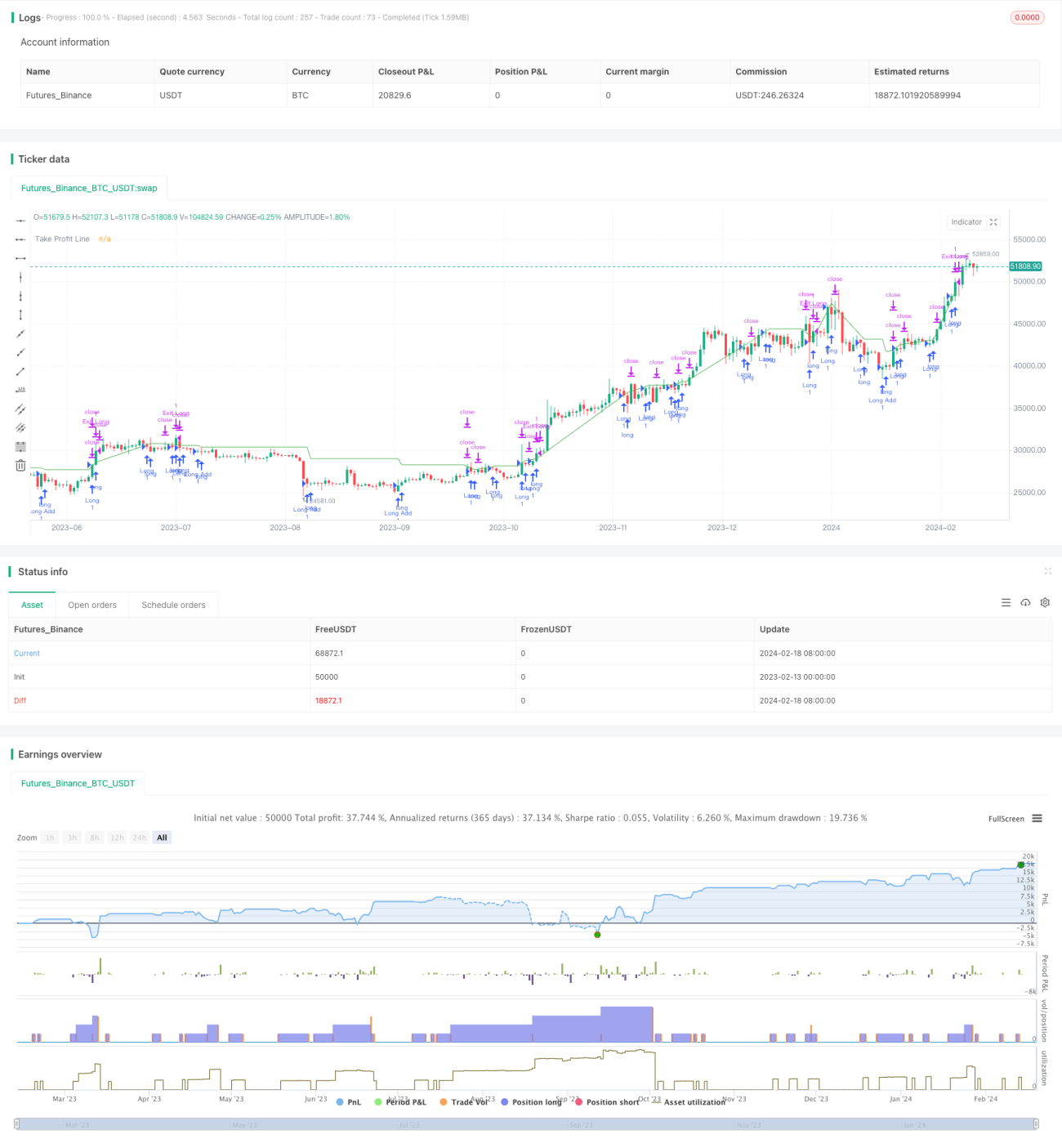

Strategi ini menggunakan gabungan beberapa petunjuk teknikal seperti RSI, MACD, OBV, CCI, CMF, MFI dan VWMACD untuk mengesan divergens antara harga dan volum, bagi mengenal pasti peluang masuk yang berpotensi. Strategi ini turut menggabungkan petunjuk pengesanan dip yang ditentukan pengguna, dan menghasilkan isyarat dagangan apabila keadaan turun naik tinggi dan syarat kedalaman atau VFI dipenuhi. Strategi ini hanya membuat posisi beli (long), dan membina kedudukan secara berperingkat menggunakan trailing stop loss.

Prinsip Strategi

-

Mengira petunjuk RSI, MACD, OBV, CCI, CMF, MFI dan VWMACD, serta menggunakan kaedah regresi linear adaptif untuk mengesan divergens antara setiap petunjuk dengan harga sejarah. Apabila petunjuk mencapai paras rendah baharu tetapi harga tidak mengikutinya, isyarat beli dikeluarkan.

-

Berdasarkan ambang turun naik dan peratusan kedalaman yang dimasukkan oleh pengguna, ditapis dengan petunjuk VFI, isyarat dikeluarkan pada lilin yang memenuhi ujian turun naik tinggi dan kedalaman.

-

Selepas posisi beli awal, jika harga jatuh di bawah peratusan tertentu daripada harga beli terakhir (boleh dikonfigurasikan), maka posisi beli ditambah semula.

-

Menggunakan trailing stop loss; apabila mencapai peratusan ambil untung yang dikonfigurasikan, kedudukan ditutup.

Analisis Kelebihan

-

Gabungan pelbagai faktor menggunakan petunjuk harga dan volum, meningkatkan kebolehpercayaan isyarat.

-

Kaedah regresi linear adaptif mengesan divergens mengelakkan subjektiviti pertimbangan manusia.

-

Menggabungkan petunjuk turun naik dan kedalaman/VFI membantu mengesan peluang pembalikan.

-

Penambahan kedudukan berbilang kali memanfaatkan pembetulan harga, dan trailing take profit membantu mengunci keuntungan.

Analisis Risiko

-

Penentuan gabungan pelbagai faktor agak rumit; kesan pengoptimuman parameter dan pengesanan divergens mungkin mempengaruhi prestasi sebenar.

-

Risiko tinggi bagi kedudukan sehala; jika penilaian salah, kerugian besar mungkin berlaku.

-

Dalam mod penambahan kedudukan berulang, kerugian juga akan dibesarkan; kawalan saiz kedudukan perlu berhati-hati.

-

Perlu mengambil kira kesan yuran transaksi terhadap keuntungan sebenar.

Arah Pengoptimuman

-

Uji kesan kombinasi parameter dan petunjuk yang berbeza, pilih konfigurasi optimum.

-

Tambah strategi stop loss untuk mengawal kerugian tunggal dan maksimum.

-

Pertimbangkan peluang dagangan dua hala untuk menyebarkan risiko.

-

Gunakan kaedah pembelajaran mesin untuk mengoptimumkan parameter secara automatik.

Kesimpulan

Strategi ini menggabungkan pelbagai petunjuk teknikal untuk mengenal pasti titik masuk, sambil menggunakan syarat ditentukan pengguna dan petunjuk VFI untuk menapis isyarat palsu. Strategi ini memanfaatkan pembetulan harga untuk menambah kedudukan secara berterusan, membantu meraih peluang dalam arah aliran. Namun, ia juga menghadapi risiko penilaian salah dan kedudukan sehala; parameter petunjuk dan strategi stop loss perlu dioptimumkan dengan sewajarnya untuk mengurangkan risiko dan meningkatkan ruang keuntungan.

- 1