A rede de contratos difíceis e fáceis

Autora:O Nobel, Data: 2021-11-18 17:28:35Tags:

Os parâmetros são muito simples, como o exemplo do BTC, para uma área com muito espaço, para uma área aberta, para uma área aberta, para uma região aberta, para uma região aberta, para uma região aberta, para uma região aberta.

Obviamente, no círculo monetário, a longo prazo, nenhum modelo complexo pode funcionar sem uma rede de cérebros.

O código da riqueza é uma rede sem cérebro + um cão sem cérebro.

A esperança, como o primeiro Martin, é a estratégia mais simples, mais rude, mas mais lucrativa.

'''backtest

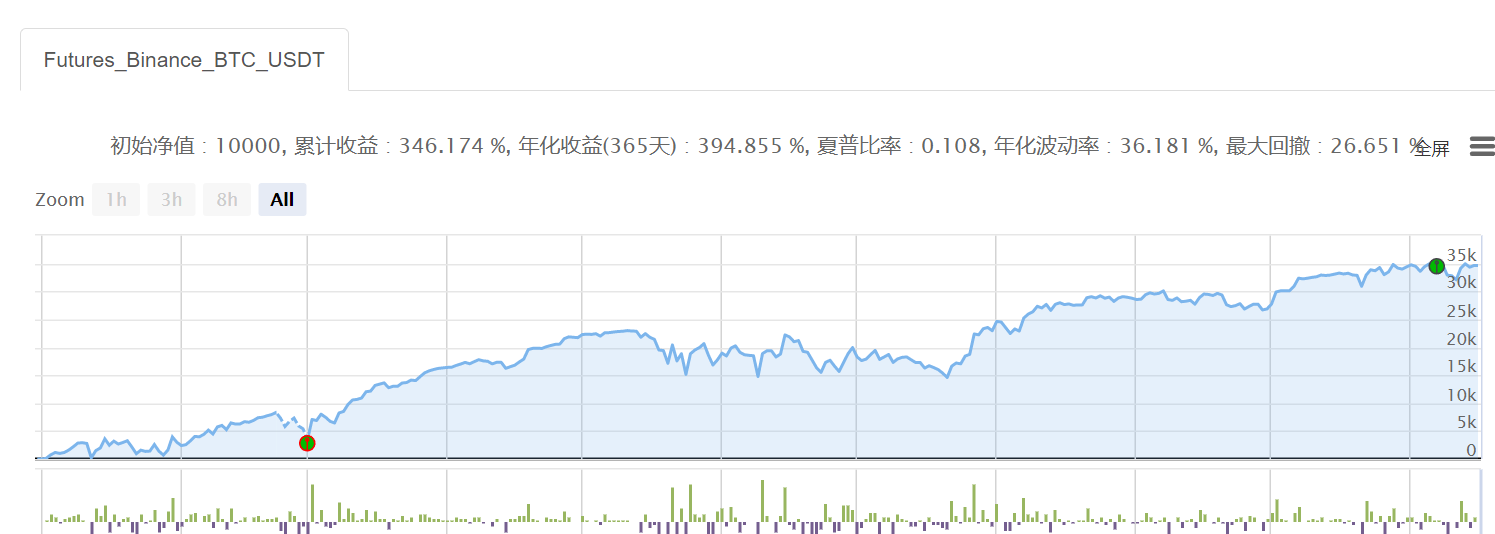

start: 2021-01-01 00:00:00

end: 2021-11-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":2500}]

args: [["H",30],["n1",0.001],["grid",300],["xia",50000]]

'''

def CancelPendingOrders():

orders = _C(exchanges[0].GetOrders)

if len(orders)>0:

for j in range(len(orders)):

exchanges[0].CancelOrder(orders[j].Id, orders[j])

j=j+1

def main():

exchange.SetContractType('swap')

exchange.SetMarginLevel(M)

currency=exchange.GetCurrency()

if _G('buyp') and _G('sellp'):

buyp=_G('buyp')

sellp=_G('sellp')

Log('读取网格价格')

else:

ticker=exchange.GetTicker()

buyp=ticker["Last"]-grid

sellp=ticker["Last"]+grid

_G('buyp',buyp)

_G('sellp',sellp)

Log('网格数据初始化')

while True:

account=exchange.GetAccount()

ticker=exchange.GetTicker()

position=exchange.GetPosition()

orders=exchange.GetOrders()

if len(position)==0:

if ticker["Last"]>shang:

exchange.SetDirection('sell')

exchange.Sell(-1,n1*H)

Log(currency,'到达开空区域,买入空头底仓')

else:

exchange.SetDirection('buy')

exchange.Buy(-1,n1*H)

Log(currency,'到达开多区域,买入多头底仓')

if len(position)==1:

if position[0]["Type"]==1:

if ticker["Last"]<xia:

Log(currency,'空单全部止盈反手')

exchange.SetDirection('closesell')

exchange.Buy(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('sell')

exchange.Sell(sellp,n1)

exchange.SetDirection('closesell')

exchange.Buy(buyp,n1)

if len(orders)==1:

if orders[0]["Type"]==1: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

if orders[0]["Type"]==0:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if position[0]["Type"]==0:

if ticker["Last"]>float(shang):

Log(currency,'多单全部止盈反手')

exchange.SetDirection('closebuy')

exchange.Sell(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('buy')

exchange.Buy(buyp,n1)

exchange.SetDirection('closebuy')

exchange.Sell(sellp,n1)

if len(orders)==1:

if orders[0]["Type"]==0: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if orders[0]["Type"]==1:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

- A estratégia de equilíbrio da Oxfam U

- Estratégias ATR para futuros de moeda digital de várias variedades (instruções)

- Transferir USDT de uma conta contratual para uma conta de dinheiro (OKEX, Binance simultaneamente)

- A ferramenta de transferência de fundos do terminal de negociação de Bitcoin

- Todas as encomendas na conta mostram ((U-bit)

- Binance abre manualmente o instrumento de liquidação

- Obtenha dados de linhas Binance K diretamente através do HttpQuery

- Estratégias binárias para a liquidez de moeda digital com várias variedades (instruções)

- Taxas de capital agregadas de todas as principais bolsas

- Estratégias de pontos de viragem binários em futuros de moedas digitais.

- A estratégia de equilíbrio do índice de preços v1.1 (que foi executada há algum tempo e agora é suspeita de que há um bug, porque não é útil, precisa ser alterada)

- Obtenha o nome da moeda do contrato USDT

- Informações sobre o mercado de assinaturas de contratos permanentes do Binance websocket

- A moeda do Japão está em alta.

- O que é que eles estão a fazer?

- Obtenção automática da precisão de negociação de contratos permanentes de Bitcoin e da posição mínima aberta (abandono)

- A negociação de contratos permanentes é um equilíbrio

- Estratégia de equilíbrio de caixa - 0.0.1v

- Grelha de contratos Binance - 0.0.2v

- Indicador de hedge (campo de zero) 0.0.1

mexminHá um problema com a gramática circular do for.

Nuvens levesTraceback (most recent call last): File "

Nuvens levesEu sou um grande fã do JS, e se eu pudesse escrever um livro com JS, seria muito melhor.

Nuvens levesMuito bem, obrigado.

O NobelEntão, se você olhar para a matriz estrutural da posição, isso deve ser um problema aqui.