Estratégia de negociação quantitativa multifatorial de momentum combinado com julgamento de tendência

Visão Geral

Esta estratégia é uma estratégia de negociação quantitativa de múltiplos fatores que combina indicadores de momentum e indicadores de tendência. A estratégia calcula combinações matemáticas de várias médias para determinar a tendência geral do mercado e a direção do momentum, emitindo sinais de negociação com base em condições de limiar.

Princípio da Estratégia

- Calcular múltiplos conjuntos de médias e indicadores de momentum

- Calcular várias médias, como a média Harmônica, a média de curto prazo, a média de médio prazo e a média de longo prazo

- Calcular as diferenças entre essas médias, refletindo a tendência de variação de preços

- Calcular a primeira derivada de cada média, refletindo o momentum de variação de preços

- Calcular indicadores de seno e cosseno para determinar a direção da tendência

- Avaliar de forma integrada os sinais de negociação

- Realizar uma operação ponderada de múltiplos fatores, como indicadores de momentum e de tendência

- Determinar o estado atual do mercado com base na distância do valor resultante em relação ao limiar

- Emitir sinais de compra e venda

Análise de Vantagens

- Julgamento de múltiplos fatores, aumentando a precisão dos sinais

- Considera múltiplos fatores: preço, tendência e momentum

- Diferentes fatores podem ser configurados com pesos distintos

- Parâmetros ajustáveis, adaptando-se a diferentes mercados

- Parâmetros das médias e limites da faixa de negociação podem ser personalizados

- Adaptável a diferentes períodos e condições de mercado

- Estrutura de código clara, fácil de entender

- Nomenclatura padronizada, comentários completos

- Fácil para desenvolvimento secundário e otimização

Análise de Riscos

- Dificuldade na otimização de parâmetros

- Necessidade de grande volume de dados históricos backtestados para encontrar os parâmetros ideais

- Frequência de negociação pode ser excessiva

- A combinação de múltiplos fatores pode gerar muitas transações

- Eficácia altamente correlacionada com o mercado

- Estratégia de julgamento de tendência, suscetível a comportamentos irracionais

Direções de Otimização

- Adicionar lógica de stop loss

- Pode evitar grandes perdas causadas por comportamentos irracionais

- Otimizar a configuração de parâmetros

- Encontrar a combinação ideal de parâmetros para aumentar a estabilidade da estratégia

- Incorporar elementos de aprendizado de máquina

- Usar aprendizado profundo para determinar o estado atual do mercado, auxiliando na tomada de decisão da estratégia

Resumo

Esta estratégia avalia o estado do mercado por meio de uma combinação de múltiplos fatores de indicadores de momentum e de tendência, emitindo sinais de negociação com base nos limiares definidos. Suas vantagens incluem alta configurabilidade, adaptabilidade a diferentes ambientes de mercado e fácil compreensão; suas desvantagens incluem a dificuldade de otimização de parâmetros, a possibilidade de alta frequência de negociação e a forte correlação com o mercado. No futuro, pode ser otimizada por meio da adição de stop loss, otimização de parâmetros e uso de aprendizado de máquina.

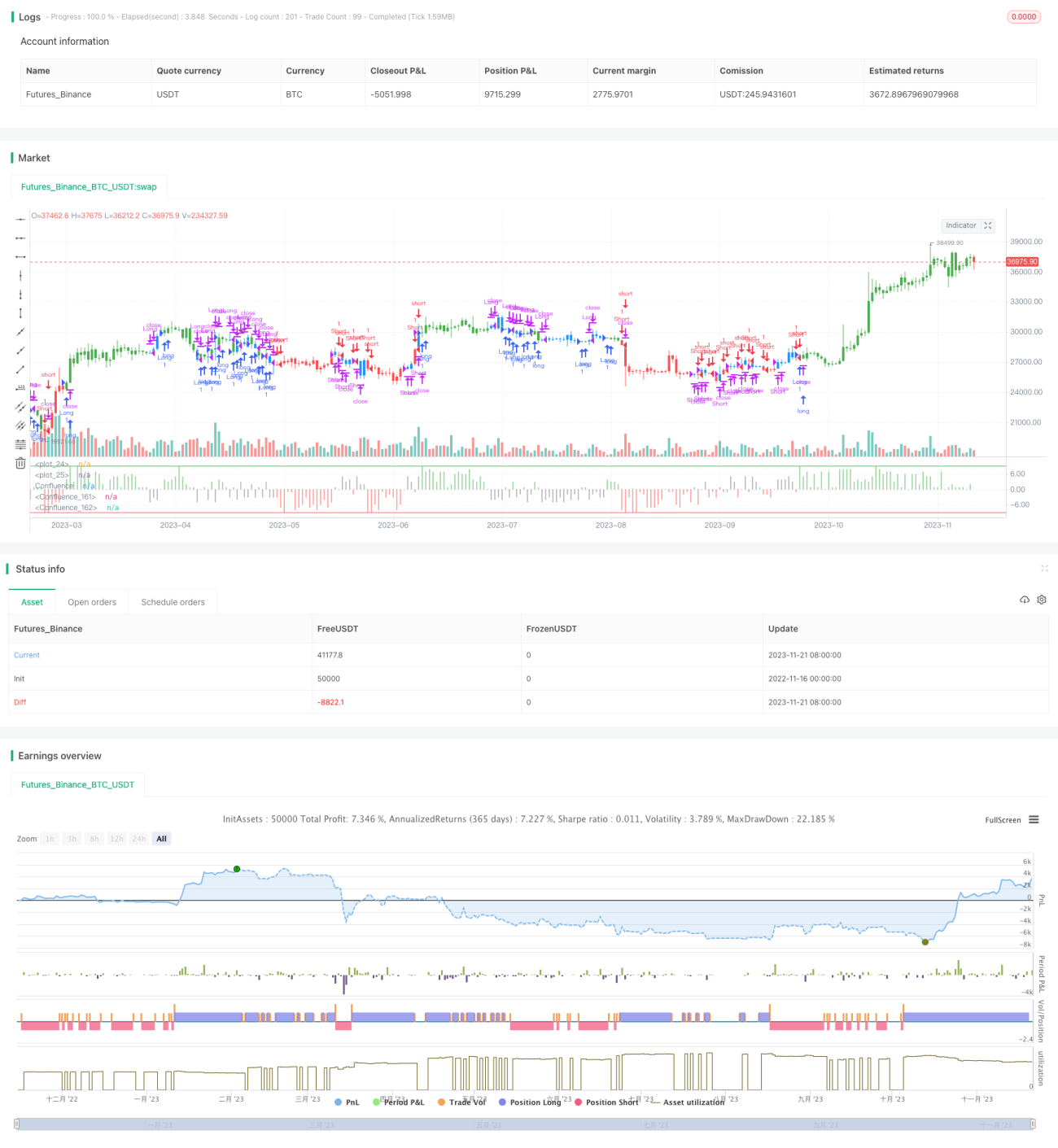

/*backtest

start: 2022-11-16 00:00:00

end: 2023-11-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 14/03/2017

// This is modified version of Dale Legan's "Confluence" indicator written by Gary Fritz.- 1