Estratégia de negociação quantitativa de reversão multifatorial

Visão Geral

Esta estratégia combina a Estratégia de Reversão 123 com a Estratégia de Linha Psicológica, formando uma estratégia de negociação quantitativa multifatorial. A estratégia considera múltiplas dimensões, como formações técnicas e psicologia de mercado, permitindo tomar decisões mais precisas ao avaliar as tendências do mercado.

Princípio

Estratégia de Reversão 123

A Estratégia de Reversão 123 avalia se o preço de fechamento do dia atual subiu em relação ao dia anterior. Se subiu e a linha lenta K está abaixo de 50, opera-se comprado; se caiu e a linha rápida K está acima de 50, opera-se vendido. Essa estratégia aproveita as características de reversão de curto prazo para obter lucros.

Estratégia de Linha Psicológica

A Estratégia de Linha Psicológica calcula a proporção de altas e baixas em um determinado período. Se a alta for superior a 50%, indica que os compradores dominam o mercado; se for inferior a 50%, indica que os vendedores dominam. Ela avalia o sentimento do mercado com base na proporção de altas/baixas.

Esta estratégia combina os sinais das duas estratégias mencionadas. Quando ambas fornecem sinais na mesma direção, abre-se uma posição; quando os sinais são opostos, fecha-se a posição.

Vantagens

A estratégia combina múltiplos fatores, permitindo avaliar as tendências do mercado com maior precisão e evitando julgamentos equivocados causados por indicadores técnicos únicos. Além disso, ao incorporar fatores de psicologia de mercado, a estratégia se torna mais robusta e capaz de lidar com condições de mercado mais complexas.

Riscos e Soluções

A definição dos parâmetros de cada fator nesta estratégia tem grande impacto em seu desempenho. Combinações inadequadas de parâmetros podem reduzir significativamente a eficácia da estratégia. Além disso, mudanças bruscas nas condições de mercado podem levar à falha da estratégia. Para mitigar riscos, é necessário realizar extensos backtests em diferentes condições de mercado para encontrar os parâmetros ideais, bem como controlar o tamanho das posições para garantir que as perdas individuais não sejam excessivas.

Direções de Otimização

Podemos continuar adicionando outros fatores de julgamento, como indicadores de volatilidade e volume, para criar uma lógica de estratégia mais tridimensional. Ou incorporar algoritmos de aprendizado de máquina para alcançar a otimização adaptativa dos parâmetros da estratégia. Essas são direções promissoras para aprimorar ainda mais esta estratégia.

Resumo

Esta estratégia considera múltiplos fatores, como formações técnicas e psicologia de mercado, validando a eficácia dos sinais por meio da verificação cruzada entre diferentes fatores. Ao mesmo tempo, oferece amplo espaço para otimização, com potencial para obter desempenho superior. Trata-se de uma estratégia quantitativa de qualidade que merece acompanhamento, acumulação e otimização a longo prazo.

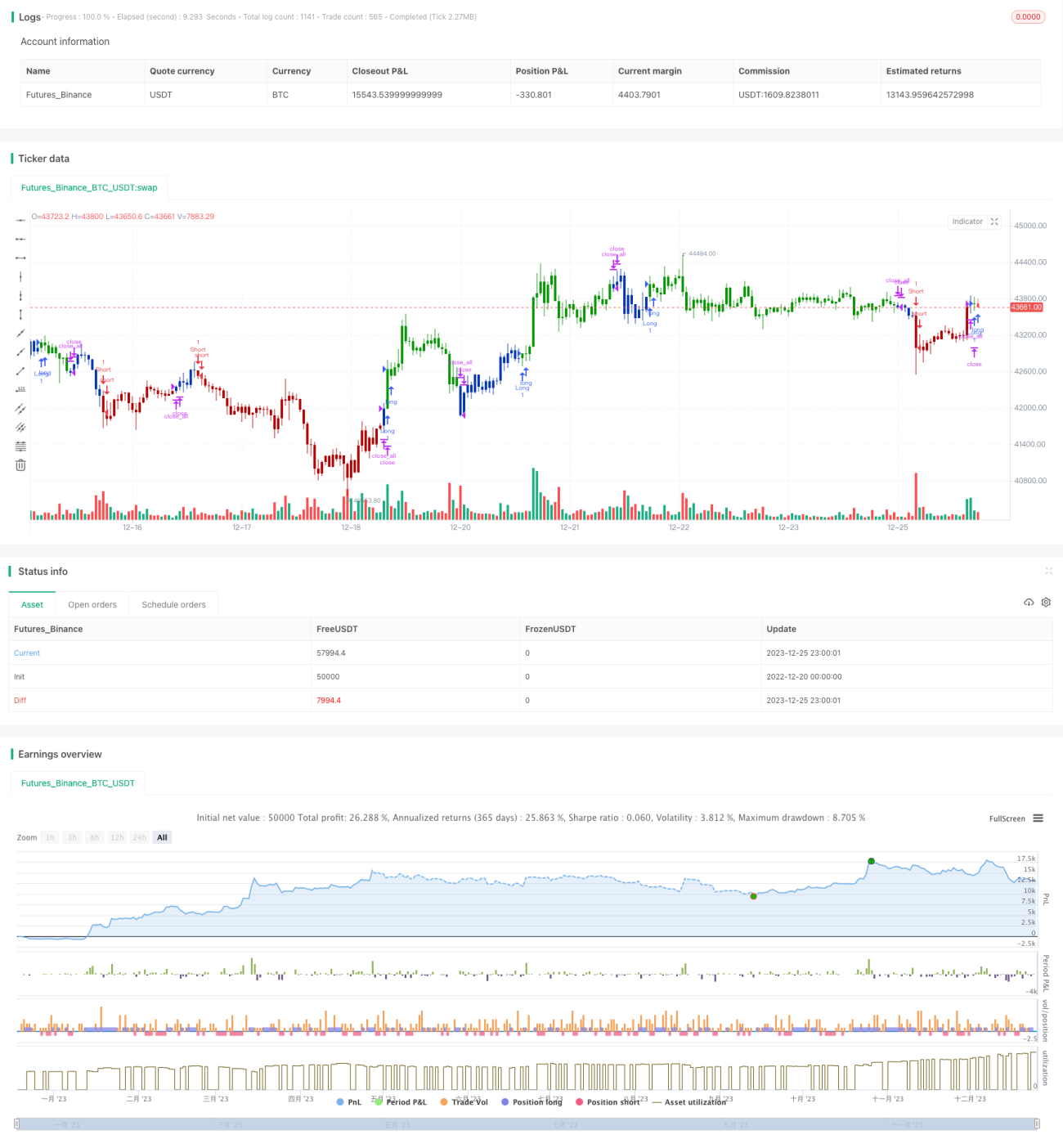

/*backtest

start: 2022-12-20 00:00:00

end: 2023-12-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 30/04/2021

// This is combo strategies for get a cumulative signal. - 1