Aplicando a estratégia de acompanhamento de equilíbrio da Média Móvel de Hull

Visão Geral

A Estratégia de Acompanhamento de Equilíbrio utiliza a Média Móvel de Hull como principal indicador de entrada, determinando a direção da tendência de preços. Ao mesmo tempo, a estratégia combina vários outros indicadores, como a linha de base, indicador de confirmação, etc., para verificar a tendência de preços e filtrar sinais falsos. Após a entrada, a estratégia utiliza o Average True Range (ATR) para calcular um stop loss dinâmico, a fim de acompanhar a tendência e obter lucros.

Princípio da Estratégia

O núcleo da Estratégia de Acompanhamento de Equilíbrio é a Média Móvel de Hull. A Média Móvel de Hull é mais sensível às mudanças de preço, permitindo determinar efetivamente a direção da tendência. Quando o preço rompe para cima a linha Hull, confirma a formação de uma tendência de alta, compre (long). Quando o preço rompe para baixo a linha Hull, confirma a formação de uma tendência de baixa, venda (short).

Além disso, a estratégia também introduz o indicador de linha de base para determinar tendências de longo prazo; e o indicador de confirmação para filtrar falsos rompimentos. Apenas quando tanto a linha de base quanto o indicador de confirmação validam a direção da tendência, o sinal de negociação é acionado.

Após a entrada, a estratégia utiliza o ATR e a Média Móvel Exponencial de Hull (Hull EMA) para calcular o valor do Average True Range e definir o nível de stop loss. À medida que a tendência continua, a linha de stop loss também se desloca para cima/baixo, a fim de travar os lucros da tendência.

Análise de Vantagens

A Estratégia de Acompanhamento de Equilíbrio combina as vantagens da identificação de tendências e do controle de risco, podendo obter bons lucros em mercados com tendência. Em comparação com estratégias de stop loss fixo, ela pode acompanhar a tendência através de um stop loss móvel, evitando ser interrompida por flutuações normais do mercado.

O uso combinado de vários indicadores também torna a estratégia mais sensível às mudanças do mercado, ao mesmo tempo que consegue filtrar efetivamente os sinais falsos. Além disso, a estratégia oferece vários parâmetros ajustáveis, e os usuários podem otimizá-los de acordo com seu próprio julgamento do mercado.

Análise de Riscos

Esta estratégia depende principalmente de indicadores de tendência, sendo propensa a gerar sinais falsos e perdas por stop loss durante períodos de consolidação. Além disso, a combinação de múltiplos indicadores pode levar a conflitos entre eles. A definição inadequada de parâmetros também pode resultar em desempenho insatisfatório da estratégia.

Pode-se considerar a adição de um módulo de julgamento adicional na estratégia, que pausa as negociações quando os indicadores apresentam divergência; ou adotar um mecanismo de votação que combine os resultados de vários indicadores. Em relação à configuração de parâmetros, pode-se encontrar os melhores parâmetros através de métodos de otimização por backtest.

Direções de Otimização

A Estratégia de Acompanhamento de Equilíbrio pode ser otimizada nas seguintes direções:

- Adicionar módulo de julgamento, como um módulo de volatilidade, que faz uma pausa nas negociações durante alta volatilidade;

- Adicionar módulo de aprendizado de máquina, utilizando algoritmos de aprendizado de máquina para determinar os pesos dos indicadores;

- Otimizar os parâmetros dos indicadores para encontrar a melhor combinação de parâmetros;

- Otimizar o algoritmo de stop loss móvel para que o stop loss acompanhe melhor a tendência;

- Adicionar módulo de gerenciamento de risco, como trailing stop, ajuste dinâmico de posição, etc.

Resumo

A Estratégia de Acompanhamento de Equilíbrio é, no geral, uma excelente estratégia de acompanhamento de tendência. Ela combina com sucesso a identificação de tendências com o stop loss dinâmico, podendo acompanhar efetivamente a tendência e obter lucros. Com novas otimizações, espera-se obter um melhor desempenho da estratégia. Esta estratégia oferece uma boa referência para a construção de estratégias de negociação quantitativa.

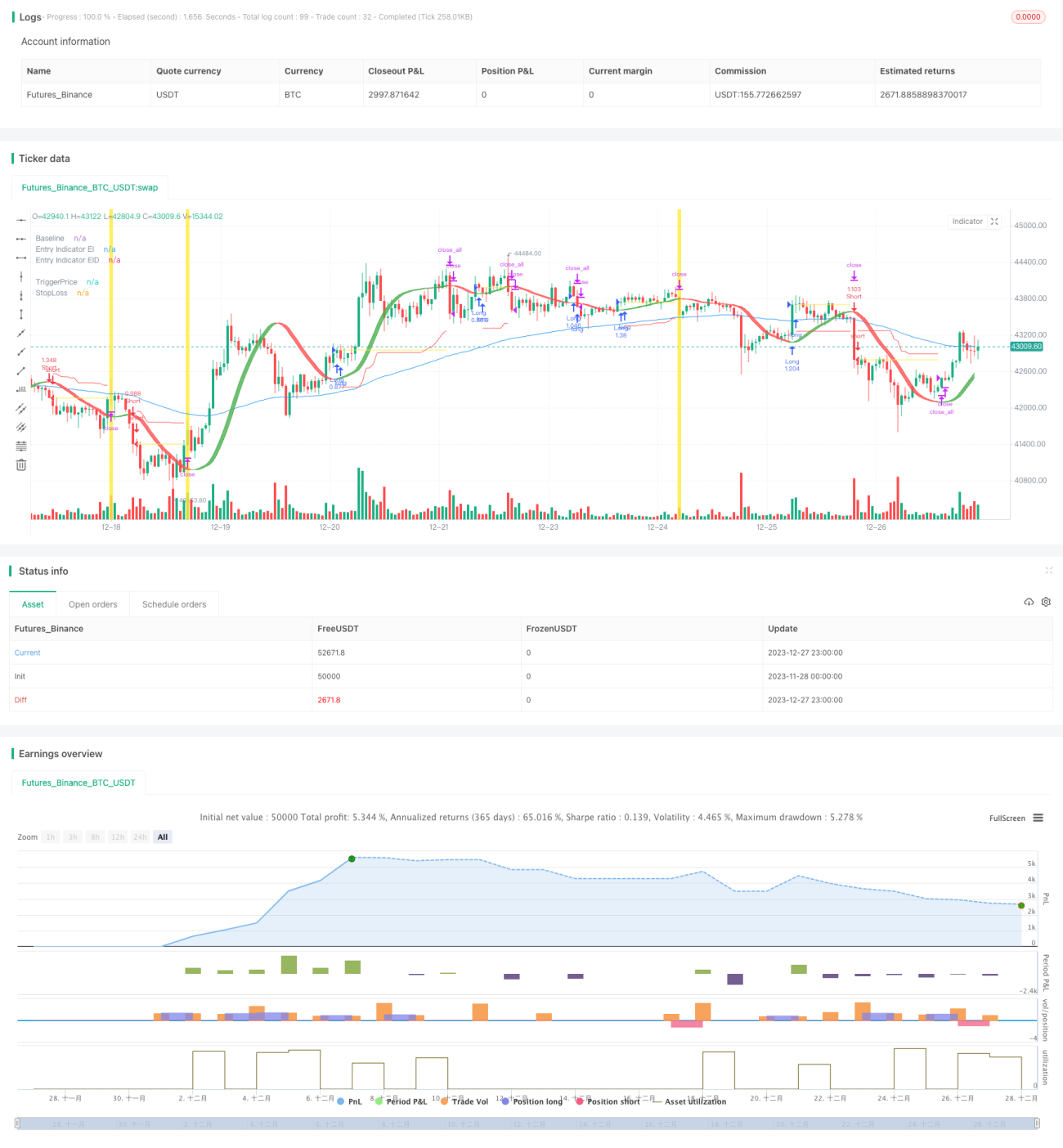

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1