Estratégia de seguir tendência sólida como uma rocha

Visão Geral

Esta estratégia é baseada na combinação do Canal Misto SSL, QQE Melhorado e Indicador de Explosão Vada Ata, criando uma estratégia robusta de acompanhamento de tendência. Ela pode gerar retornos estáveis em criptomoedas de grande porte como BTC e ETH, sendo adequada para operações de médio e longo prazo.

Princípio da Estratégia

Lógica de Entrada

Condições para entrada em posição comprada:

- Preço de fechamento acima da linha base do Canal Misto SSL

- Indicador QQE Melhorado muda de cor para azul

- Indicador de Explosão Vada Ata está verde

Condições para entrada em posição vendida:

- Preço de fechamento abaixo da linha base do Canal Misto SSL

- Indicador QQE Melhorado muda de cor para vermelho

- Indicador de Explosão Vada Ata está vermelho

Lógica de Saída

Condições para saída de posição comprada:

- Indicador QQE Melhorado muda de cor para vermelho

Condições para saída de posição vendida:

- Indicador QQE Melhorado muda de cor para azul

Análise de Vantagens

Esta estratégia apresenta as seguintes vantagens:

-

A combinação de três indicadores garante a precisão e estabilidade dos sinais de negociação.

-

A linha base do Canal SSL e o indicador QQE Melhorado capturam efetivamente a direção da tendência.

-

O Indicador de Explosão Vada Ata valida ainda mais os sinais de negociação, evitando falsos rompimentos.

-

A estrutura do código é clara, fácil de entender e modificar.

-

Possui mecanismos completos de stop loss, take profit e gerenciamento de risco, controlando os riscos de forma eficaz.

-

Apresenta excelente desempenho em backtests em períodos de tempo maiores (como 1 hora, 4 horas).

Análise de Riscos

Esta estratégia também apresenta os seguintes riscos:

-

Em períodos de tempo curtos (como 5 minutos), os resultados do backtest são ruins.

-

Em mercados com grande volatilidade, os stops podem ser acionados com frequência.

-

Em algumas criptomoedas específicas, os resultados do backtest podem ser insatisfatórios.

Para esses riscos, podem ser tomadas as seguintes medidas:

-

Utilizar apenas para operações de médio e longo prazo, não adequado para curto prazo.

-

Aumentar adequadamente a amplitude do stop loss para evitar acionamentos excessivos.

-

Testar mais ativos para encontrar criptomoedas que se adequem às características da estratégia.

Direções de Otimização

Esta estratégia pode ser otimizada nos seguintes aspectos:

-

Testar diferentes configurações de parâmetros para encontrar a combinação ideal.

-

Incorporar elementos de aprendizado de máquina para tornar a estratégia mais adaptável.

-

Combinar múltiplos fatores, como indicadores de sentimento, para melhorar a estabilidade geral do sistema.

-

Estudar as características do setor e ajustar os parâmetros para tornar a estratégia aplicável a setores específicos.

-

Adicionar módulos de negociação algorítmica, utilizando ordens programáticas para aumentar o retorno.

Resumo

No geral, esta estratégia é recomendável. Ela é estável, fácil de entender e possui um sistema completo de gerenciamento de risco. Nos ativos e períodos de tempo adequados, pode gerar bons retornos. Com otimização e ajustes contínuos, esta estratégia pode se tornar uma ferramenta eficiente de investimento quantitativo.

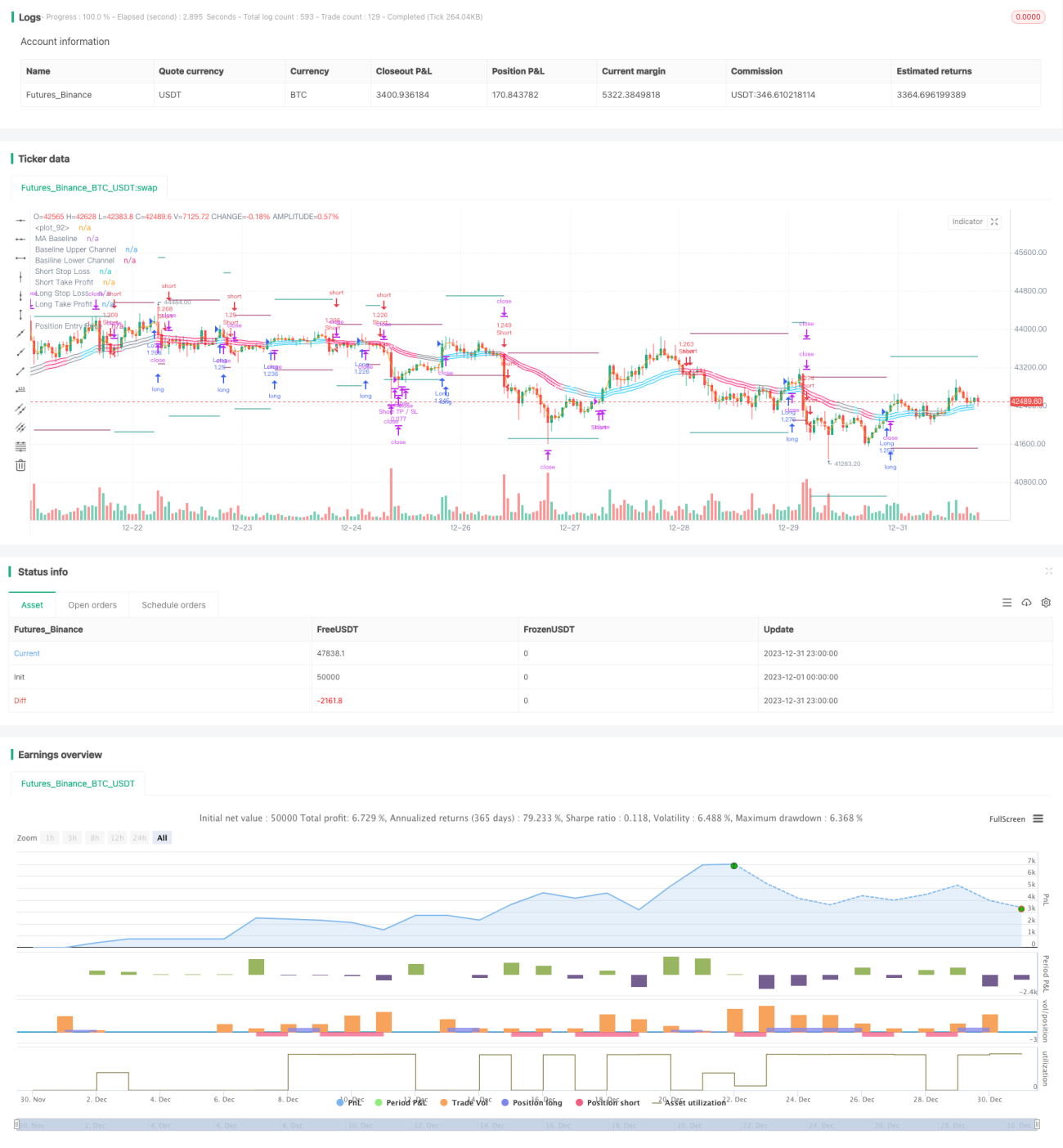

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1