Estratégia quantitativa de seguimento de tendência baseada nos indicadores Hull e LSMA

Visão Geral

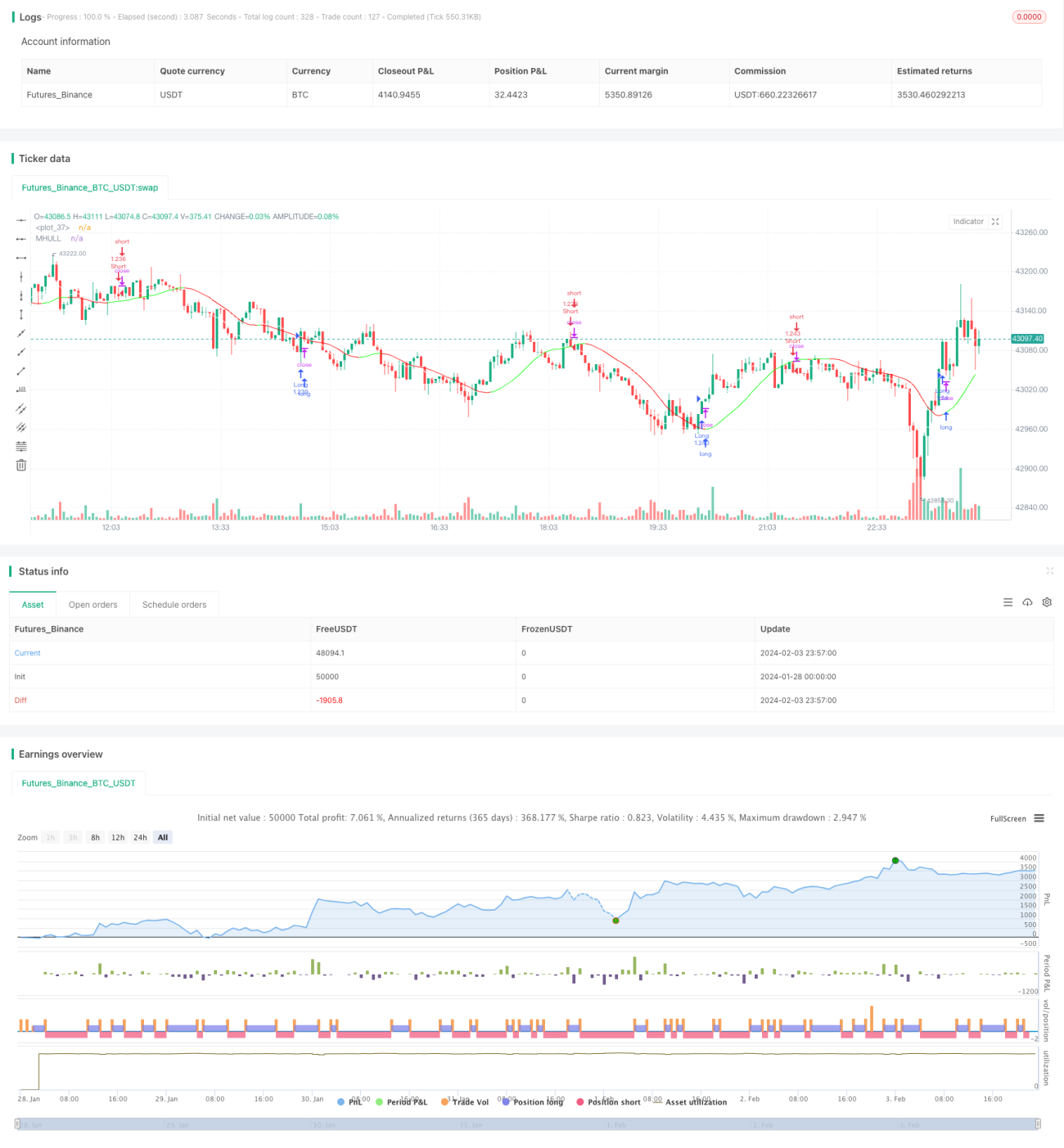

Esta estratégia combina o indicador Hull (HMA) e o indicador LSMA (Média Móvel dos Mínimos Quadrados) para identificar a direção da tendência e pontos de reversão, realizando o acompanhamento da tendência. Quando o indicador Hull mostra uma tendência de alta e o LSMA cruza acima do Hull, opera-se comprado; quando o Hull mostra tendência de baixa e o LSMA cruza abaixo do Hull, opera-se vendido. A estratégia é adequada para negociações de média/baixa frequência, podendo ser utilizada no timeframe de 1 minuto.

Princípio da Estratégia

-

O indicador Hull é usado para determinar a direção da tendência de valor. Quando a linha média (MHULL) está acima da linha inferior (LHULL), indica tendência de alta; caso contrário, indica tendência de baixa.

-

O indicador LSMA é usado para identificar pontos de reversão da tendência. Quando o LSMA cruza acima do MHULL, indica que a tendência de alta se formou ou acelerou; quando o LSMA cruza abaixo do MHULL, indica que a tendência de baixa se formou ou acelerou.

-

Combinando ambos: quando o Hull mostra tendência de alta (MHULL > LHULL) e o LSMA cruza acima do MHULL, opera-se comprado; quando o Hull mostra tendência de baixa (MHULL < LHULL) e o LSMA cruza abaixo do MHULL, opera-se vendido.

-

O stop loss é definido no ponto de volatilidade mais recente. Para posições compradas, o stop é o ponto mais baixo recente; para posições vendidas, o stop é o ponto mais alto recente.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

-

O indicador Hull responde rapidamente, capturando mudanças de tendência em tempo hábil; o LSMA possui alta suavidade, identificando sinais de reversão com precisão e confiabilidade. A combinação de ambos apresenta bons resultados.

-

O cruzamento do LSMA filtra sinais falsos gerados pelo indicador Hull, reduzindo a probabilidade de negociações errôneas.

-

O uso de pontos de volatilidade como stop loss protege ao máximo o capital.

-

Adequada para negociações de média/baixa frequência, podendo ser utilizada em timeframes de 1 minuto ou até menores, com ampla aplicabilidade.

Análise de Riscos

A estratégia também apresenta alguns riscos:

-

Em mercados laterais (sem tendência), o Hull e o LSMA podem gerar múltiplos cruzamentos, resultando em negociações excessivas. Recomenda-se ajustar adequadamente os parâmetros para reduzir a frequência de negócios.

-

O stop loss baseado em pontos de volatilidade pode ser acionado por ajustes de preço de curto prazo; é recomendável aumentar a distância entre os stops.

-

Devido à natureza defasada do LSMA, há um leve risco de erro na identificação. É aconselhável confirmar com outros indicadores, como formações de candles.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

-

Otimizar os parâmetros do indicador Hull e do LSMA para melhor combinação com diferentes ativos e períodos.

-

Adicionar filtros baseados em volatilidade, volume de negociação, etc., para evitar negociações errôneas em mercados laterais.

-

Incorporar algoritmos de aprendizado de máquina para auxiliar na determinação da direção da tendência.

-

Utilizar técnicas como aprendizado profundo para identificar níveis críticos de suporte e resistência, tornando o stop loss mais adequado.

Resumo

Esta estratégia, por meio da aplicação combinada dos indicadores Hull e LSMA, avalia as mudanças de direção da tendência e realiza negociações de acompanhamento de tendência. Suas vantagens são a simplicidade operacional e a rápida resposta, sendo amplamente aplicável a negociações quantitativas de média/baixa frequência. Com otimizações adicionais nos filtros, na confirmação auxiliar e no algoritmo de stop loss, é possível obter melhores resultados.

- 1