Nova estratégia de trading quantitativo baseada no padrão ABCD com trailing stop e trailing take profit.

I. Visão Geral da Estratégia

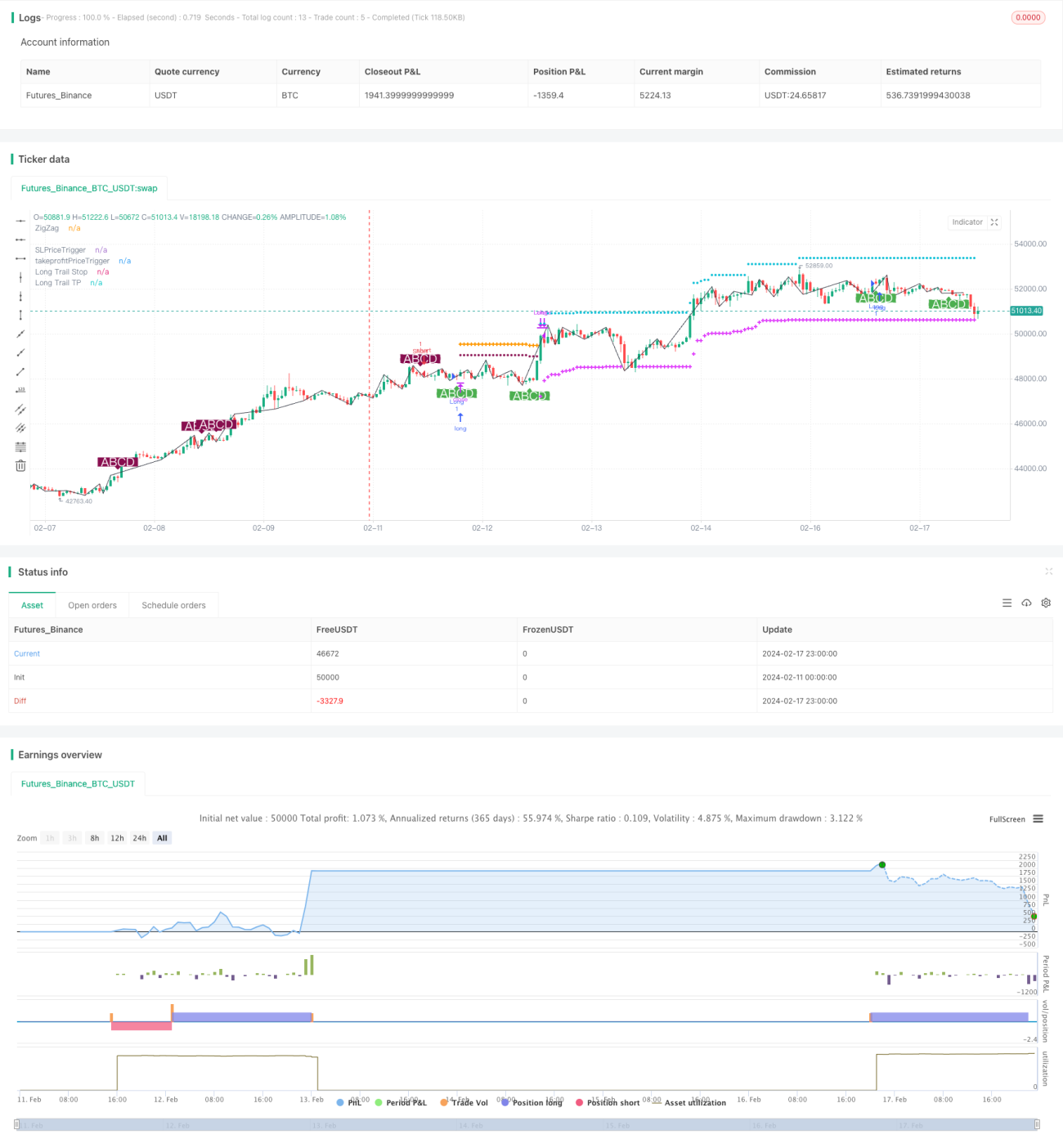

Esta estratégia é denominada "Estratégia de Negociação de Padrão ABCD Ideal (com Stop Loss Trailing e Take Profit Trailing)". Trata-se de uma estratégia quantitativa que opera com base no modelo claro de padrão de preços ABCD. A ideia principal é identificar o padrão ABCD completo e, em seguida, comprar ou vender de acordo com a direção do padrão, configurando stops e takes móveis para gerenciar as posições.

II. Princípio da Estratégia

-

Utiliza o método de julgamento auxiliar das Bandas de Bollinger para identificar os pontos de topo e fundo de preços, obtendo a curva ZigZag dos preços.

-

Na curva ZigZag, identifica o padrão ABCD completo. Os quatro pontos A, B, C e D devem satisfazer uma relação de proporção específica. Após identificar um padrão ABCD válido, executa-se uma operação de compra ou venda.

-

Após abrir a posição, é configurado um stop loss trailing para controlar o risco. Inicialmente, usa-se um stop loss fixo; quando o lucro atinge uma certa porcentagem, ele é convertido em um stop loss móvel para travar parte do lucro.

-

Da mesma forma, é configurado um take profit trailing para garantir que, após obter lucro suficiente, a posição seja fechada a tempo, evitando a devolução dos ganhos. O take profit trailing também é dividido em duas fases: primeiro um take profit fixo para capturar parte do lucro e, depois, um take profit móvel que continua acompanhando o preço.

-

Quando o preço atinge o stop loss móvel ou o take profit, a posição é encerrada, completando um ciclo de negociação.

III. Análise das Vantagens da Estratégia

-

O uso do método de julgamento auxiliar das Bandas de Bollinger para identificar a curva ZigZag evita o problema de lookahead da curva ZigZag tradicional, tornando os sinais de negociação mais confiáveis.

-

O modelo de negociação com padrão ABCD é maduro e estável, oferecendo oportunidades de negociação razoavelmente abundantes. Além disso, a direção do padrão ABCD é clara, facilitando a decisão de entrada.

-

A configuração do stop e take em duas fases permite melhor controle de risco e obtenção de lucros. O stop e take móveis tornam a estratégia mais flexível.

-

Os parâmetros da estratégia são razoavelmente projetados; as porcentagens de stop/take fixos e o percentual para ativar o modo móvel podem ser personalizados, oferecendo flexibilidade de uso.

-

Esta estratégia pode ser aplicada a qualquer ativo, incluindo forex, criptomoedas e índices de ações.

IV. Análise de Risco da Estratégia

-

Embora o padrão ABCD seja relativamente claro, as oportunidades de negociação são limitadas, não garantindo uma frequência suficiente de operações.

-

Em mercados laterais, o stop loss e take profit podem ser acionados com frequência. Nesse caso, é necessário ajustar adequadamente os parâmetros, ampliando a faixa de stop/take.

-

É preciso prestar atenção à liquidez do ativo negociado. Ativos com baixa liquidez podem impedir a execução precisa do stop e take.

-

A estratégia é sensível aos custos de negociação; é necessário escolher corretoras e contas com taxas baixas.

-

Alguns parâmetros podem ser otimizados, por exemplo, as condições para ativar o stop/take móvel podem ser testadas com mais valores para encontrar o ponto ideal.

V. Direções para Otimização da Estratégia

-

Pode-se combinar outros indicadores para adicionar mais filtros, evitando certos padrões ruins (como falsos H&W). Isso reduz operações ineficazes.

-

Adicionar julgamento da estrutura de três ondas do mercado, buscando oportunidades apenas na terceira onda. Isso pode aumentar a taxa de acerto da estratégia.

-

Testar e otimizar o tamanho do capital inicial para encontrar o nível ideal. Tanto capital muito grande quanto muito pequeno são desfavoráveis para obter a melhor taxa de retorno.

-

Pode-se testar dados fora da amostra para verificar a robustez dos parâmetros. Isso é essencial para compreender a estabilidade de médio e longo prazo da estratégia.

-

Continuar otimizando as condições de ativação do stop/take móvel e o tamanho do slippage, melhorando a eficiência da execução. A otimização de parâmetros é interminável.

VI. Resumo da Estratégia

Esta estratégia depende principalmente do padrão de preços ABCD para julgar o mercado e entrar em posições. Utiliza stops e takes móveis em duas fases para gerenciar riscos e lucros. A estratégia é relativamente madura e estável, mas a frequência de negociação pode ser baixa. Podemos obter oportunidades de negociação mais eficientes adicionando filtros. Além disso, continuar otimizando os parâmetros e o tamanho do capital pode melhorar ainda mais a capacidade de lucro estável da estratégia. No geral, a estratégia tem uma lógica clara, é fácil de entender e implementar, sendo uma estratégia de negociação quantitativa digna de estudo e aplicação aprofundados.

- 1