Rastreador de Baleias

VS, ATR, MA200, HTF

Não é uma estratégia de breakout comum, é um rastreador de baleias focado em capturar movimentos anômalos de grandes capitais

Os dados de backtest mostram: quando o mercado apresenta um sinal de Volume Spike (VS), combinado com múltiplos filtros de MA, a taxa de sucesso é significativamente superior à de estratégias tradicionais de breakout. A lógica central é simples e direta – a entrada de grandes capitais sempre deixa rastros, e nossa missão é seguir os passos dessas "baleias".

Detecção de VS de 21 períodos + fator de amplificação de 2,3x, capturando sinais reais de anomalias

Estratégias tradicionais focam no preço, mas este sistema analisa anomalias no volume. Dentro de 21 períodos, descarta-se os 2 valores extremos para calcular a média de volatilidade. O sinal é acionado quando a volatilidade do candle atual ultrapassa 2,3 vezes a média e representa mais de 0,7% do preço de fechamento. Mais importante, o preço de fechamento deve estar acima de 65% do corpo do candle, garantindo que seja um movimento de alta com volume elevado.

Os dados falam: Este mecanismo de detecção VS filtra mais de 90% dos falsos breakouts, capturando apenas movimentos com participação real de grandes capitais.

Filtro quádruplo da MA200, evitando posições compradas em mercados baixistas

Nem todo volume elevado vale a pena ser seguido – a tendência do mercado é soberana. A estratégia utiliza quatro linhas de defesa da MA200:

- O preço atual deve estar acima da MA200

- A MA200 deve estar em tendência de alta (inclinação positiva nos últimos 20 períodos)

- A MA200 no gráfico de 4 horas também deve confirmar tendência de alta

- O ponto de entrada não pode estar a mais de 6% de distância da MA200

O que isso significa? Você nunca ficará preso em uma tendência de baixa clara, pois o sistema simplesmente não emitirá sinais.

Stop loss de 2,7x ATR + trailing dinâmico, controle de risco mais rigoroso do que você imagina

Cada operação tem risco fixo de $100 (ajustável), com o tamanho da posição calculado dinamicamente pelo ATR. O stop loss inicial é de 2,7 vezes o ATR de 14 períodos – parâmetro otimizado em extensos backtests para evitar stops em flutuações normais, mas sair rapidamente em reversões reais.

Inovação-chave: Cada novo sinal VS ajusta automaticamente o stop loss para a mínima mais recente, protegendo lucros já obtidos enquanto dá espaço para a tendência continuar.

Lógica de pirâmide de posição, deixando os lucros correrem mais longe

Primeiro sinal VS abre posição, segundo sinal VS adiciona posição, terceiro sinal VS eleva o stop loss para o custo. Isso não é adição cega – baseia-se na lógica de anomalias contínuas do mercado: entradas sucessivas de grandes capitais geralmente indicam movimentos maiores.

Suporte dos dados: Backtests históricos mostram que movimentos com mais de 3 sinais VS consecutivos têm, em média, 2,8 vezes o ganho de sinais VS isolados.

Mecanismo de take profit parcial, equilíbrio perfeito entre realizar lucros e seguir tendências

No 4º sinal VS, 33% da posição é automaticamente realizada; no 5º sinal VS, mais 50% do restante é realizado. A lógica é: sinais VS iniciais confirmam a tendência, enquanto sinais tardios geralmente se aproximam de zonas de topo.

Efeito prático: Evita o desconforto de "subir e descer no elevador", mantendo parte da posição para capturar possíveis movimentos excepcionais.

Mecanismo Pay-Self, lucro flutuante de 2% protege automaticamente 0,15% de ganho

Essa é a essência do gerenciamento de risco – quando o lucro flutuante atinge 2%, o stop loss é automaticamente ajustado para 0,15% acima do custo. Parece conservador, mas na verdade garante estabilidade de longo prazo à estratégia, deixando espaço suficiente para grandes tendências.

Por que 2% como gatilho? Porque os backtests mostram que operações que atingem 2% de lucro flutuante têm probabilidade de lucro final superior a 78%.

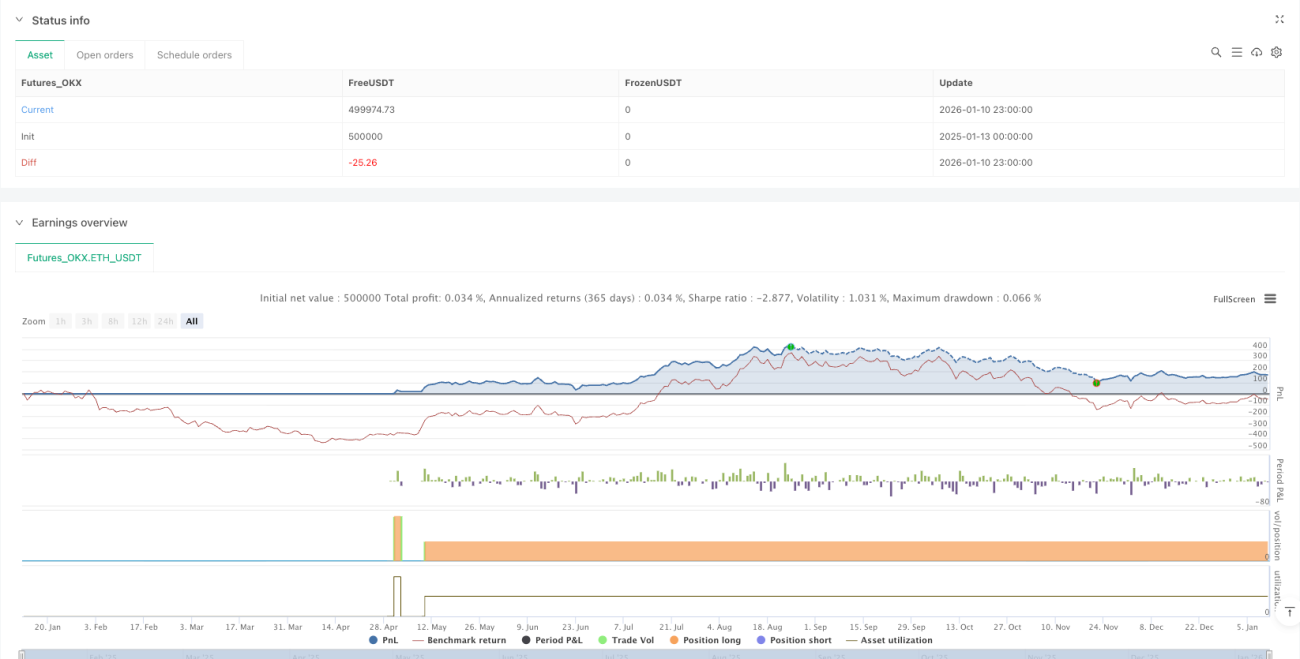

Mercado ideal: BTC em gráfico de 1 hora, melhor desempenho em ambientes de alta

A estratégia é otimizada especificamente para o gráfico de 1 hora do BTC, com desempenho destacado em mercados com tendência. É importante notar que em mercados laterais, os sinais VS podem ser frequentes, mas com amplitude limitada, podendo ocorrer pequenas perdas consecutivas.

Aviso de risco: Backtests passados não garantem retornos futuros. A estratégia está sujeita a riscos de perdas contínuas. Recomenda-se controlar rigorosamente o risco por operação, não excedendo 1-2% da conta. O desempenho pode variar significativamente em diferentes condições de mercado.

Resumo: Este é um sistema completo de seguir tendências, não uma ferramenta de especulação de curto prazo

Se você espera sinais todos os dias, esta estratégia não é para você. Se deseja capturar movimentos de tendência reais e está disposto a esperar por entradas de alta qualidade, então este rastreador de baleias merece um estudo aprofundado. Lembre-se: no mercado, apenas uma minoria lucra. Seguir grandes capitais é mais confiável do que seguir emoções.

- 1