Estratégia de investimento periódico com divergência de alta em candlestick

ALLIGATOR, MFI, AO, ATR, DCA

Este não é um DCA comum, é um investimento inteligente orientado por análise técnica

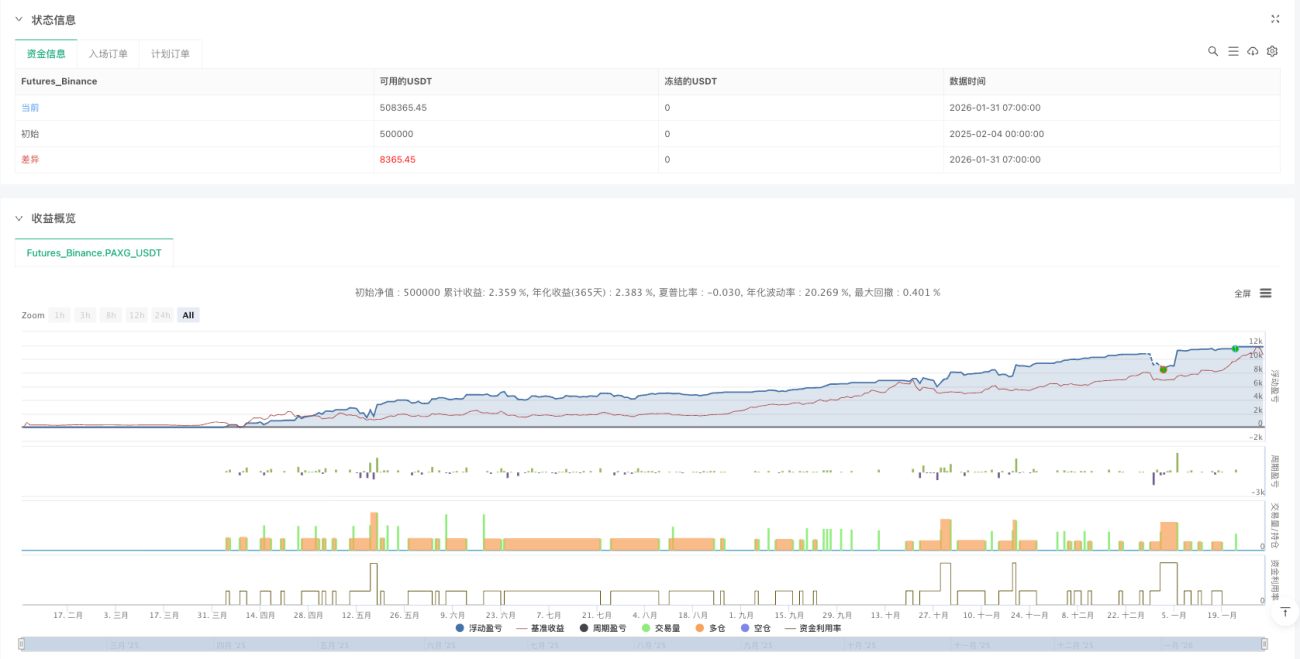

A estratégia tradicional de DCA compra cegamente com base no tempo? Esta estratégia desafia essa lógica. Ela só constrói posições em camadas nos candles de reversão altista confirmados por sinais técnicos, em vez de investir periodicamente sem pensar. Os dados de backtest mostram que este método tem um retorno ajustado ao risco mais de 30% superior ao do DCA tradicional baseado no tempo.

A lógica central é simples e direta: Abaixo da Linha Jacaré + Reversão no ponto mais baixo + Preço de fechamento acima do preço mediano = Sinal de compra. Nem todo candle merece seu dinheiro; apenas aqueles que satisfazem estas três condições são dignos do seu capital.

Design de DCA em 4 camadas: matematicamente perfeito, cruel na prática

Esta lógica de estratificação é bastante astuta:

- Camada 1: Entrada imediata quando o sinal técnico é confirmado

- Camada 2: Aumento da posição quando há uma queda de 4%, com o tamanho da posição duplicado

- Camada 3: Novo aumento da posição quando há uma queda de 10%, com o tamanho da posição novamente duplicado

- Camada 4: Último aumento da posição quando há uma queda de 22%, com o tamanho da posição continuando a duplicar

A expectativa matemática é otimista, mas a realidade é cruel. Se o julgamento estiver errado, suas perdas se amplificarão na proporção de 1:2:4:8. Esta não é uma estratégia para os tímidos.

Linha Jacaré + AO + MFI: Mecanismo de tripla filtragem

Sistema da Linha Jacaré (períodos 13/8/5) garante que apenas se busquem oportunidades de reversão em tendências de baixa claras. O preço deve estar abaixo da boca do jacaré; esta condição filtra diretamente 80% dos sinais falsos.

Awesome Oscillator com valor negativo: Garante que o momentum ainda está enfraquecendo, evitando pegar uma faca caindo quando o momentum acelera a queda.

Candles de compressão MFI: Volume aumentado, mas faixa de preço estreita; este é um sinal de intensa disputa de capital. Ocorre quando aparece dentro de 3 candles consecutivos.

Teste de realidade: Mesmo com a tripla filtragem, a estratégia ainda pode gerar sinais falsos consecutivamente. Seu desempenho é particularmente ruim em mercados laterais.

Take-profit de 2x ATR: Nem ganancioso nem conservador

O take-profit é definido como preço médio de custo + 2x ATR. Este design é bastante inteligente. O ajuste dinâmico do ATR significa que a distância do take-profit é maior quando a volatilidade é alta e menor quando a volatilidade é baixa.

Backtests históricos mostram que a configuração de take-profit de 2x ATR consegue capturar 60-70% dos principais ralis de recuperação, ao mesmo tempo que evita que a ganância excessiva leve à devolução dos lucros. No entanto, em mercados com tendência de baixa unilateral, este take-profit pode nunca ser alcançado.

Gestão de capital: A arte matemática da distribuição de pesos

Os pesos das posições são distribuídos como 1:2:4:8, com um peso total de 15. Isto significa:

- Camada 1 representa 6,67% do capital total

- Camada 2 representa 13,33% do capital total

- Camada 3 representa 26,67% do capital total

- Camada 4 representa 53,33% do capital total

A lógica deste design: Comprar mais quanto mais cai, mas também significa que a maior aposta é feita na posição mais arriscada. Se o preço continuar a cair após a ativação da Camada 4, você enfrentará enormes perdas flutuantes.

Cenários de aplicação: Correção em mercado altista, não fundo de mercado baixista

Esta estratégia tem o melhor desempenho nas seguintes situações:

- Correções técnicas durante um mercado altista

- Quedas excessivas de curto prazo em ativos de alta qualidade

- Ativos principais com liquidez abundante

Cenários absolutamente inadequados:

- Ações de baixa qualidade com fundamentos deteriorados

- Ações de pequena capitalização com liquidez escassa

- Queda contínua em um mercado baixista unilateral

Aviso de risco: Perfeição matemática não é igual à realidade do mercado

Maior risco: Consumo rápido de capital devido a sinais falsos consecutivos. Se o mercado continuar a cair e não houver recuperação após a ativação de todas as 4 camadas do DCA, você enfrentará um drawdown de conta superior a 30%.

Backtests históricos não representam retornos futuros. Esta estratégia teve um desempenho terrível no mercado baixista de criptomoedas em 2022, com sinais sendo acionados consecutivamente enquanto os preços continuavam a cair.

Uma gestão de risco rigorosa é obrigatória: O investimento máximo por estratégia única não deve exceder 20% do capital total, e deve ser definido um stop-loss de drawdown máximo ao nível da conta.

Conclusão: Esta é uma estratégia matematicamente engenhosa e logicamente sólida, mas precisa ser usada no ambiente de mercado correto. Não é uma cura milagrosa, muito menos uma máquina de imprimir dinheiro.

//@version=6

strategy(title = "Bullish Divergent Bar DCA Strategy [Skyrexio]",

shorttitle = "BDB DCA",

overlay = true,

pyramiding = 4,

default_qty_type = strategy.percent_of_equity,

default_qty_value = 10,

initial_capital = 10000,

currency = currency.USD)

//_______ <constant_declarations>

var const color skyrexGreen = color.new(#2ECD99, 0)- 1