Стратегия покупки на коррекционном падении

Обзор

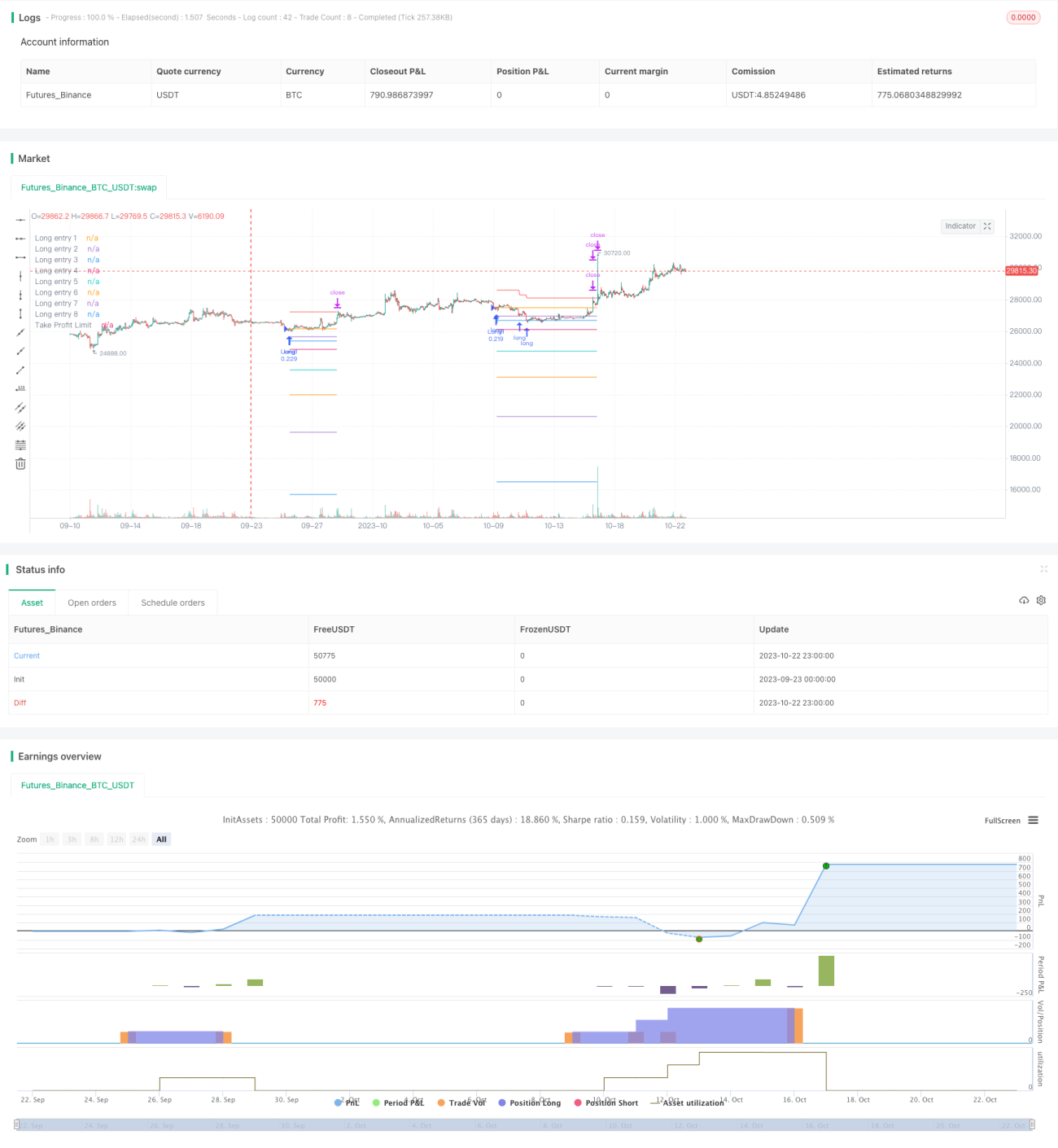

Данная стратегия сочетает индикатор RSI и скользящую среднюю цены, открывая длинную позицию при падении цены ниже скользящей средней в зоне перепроданности. При дальнейшем снижении цены стратегия последовательно добавляет позиции с заданным процентом, чтобы усреднить стоимость входа. Когда прибыль по позиции достигает заданного процента тейк-профита, стратегия закрывает позицию. Кроме того, стратегия внедряет механизм постепенного тейк-профита, динамически корректируя цену тейк-профита всей позиции на основе уже реализованной прибыли по отдельным частям. Это эффективно снижает риск убытков и обеспечивает постепенный выход.

Принцип стратегии

-

Когда RSI ниже уровня перепроданности 29 и цена закрытия ниже скользящей средней, открывается первая длинная позиция.

-

При падении цены на 2% от первой позиции добавляется вторая длинная позиция; при падении на 3% — третья, и так до 8 добавлений. Это реализует поэтапное наращивание позиции.

-

После каждого открытия позиции фиксируется цена открытия. Эти цены служат референтными точками входа и отображаются на графике в виде линий.

-

После открытия позиции рассчитывается средняя цена всех частей. 3% от средней цены используется как тейк-профит для каждой отдельной позиции, 4% — как тейк-профит для всей совокупной позиции.

-

Когда цена поднимается выше тейк-профита отдельной позиции, эта позиция закрывается.

-

Расчет постепенного тейк-профита: при закрытии каждой позиции из общего тейк-профита вычитается прибыль, полученная по этой позиции. Это позволяет линии тейк-профита медленно опускаться, и только когда прибыль по всем позициям достаточна для покрытия максимального убытка, происходит полное закрытие.

-

Когда цена достигает линии постепенного тейк-профита, все позиции закрываются.

Анализ преимуществ

-

Индикатор RSI достаточно точно определяет зону перепроданности, что способствует выявлению разворотов.

-

Многократное добавление позиций позволяет усреднить стоимость входа на низких уровнях.

-

Постепенный тейк-профит снижает риск убытков и обеспечивает постепенный выход. Даже при убытках они контролируются в определенных пределах.

-

Настраиваемые проценты тейк-профита и добавления позволяют адаптировать риск стратегии к рынку.

-

Отображение на графике линий открытия и тейк-профита позволяет интуитивно оценить распределение позиций.

Анализ рисков

-

На волатильном рынке стратегия может часто срабатывать на открытие и закрытие, что приводит к проскальзыванию из-за большого числа сделок. Можно увеличить параметры RSI, чтобы уменьшить количество сделок.

-

Неправильная настройка количества и процента добавлений может привести к чрезмерной торговле; эти параметры следует выбирать с учетом объема капитала.

-

Если рынок продолжает падать после добавлений, стратегия может столкнуться с неограниченным риском. Следует установить максимальное количество добавлений и консервативный процент для последнего добавления.

-

Слишком маленький процент тейк-профита может привести к преждевременному закрытию. Следует подобрать оптимальный процент на основе исторических тестов.

Направления оптимизации

-

Можно добавить фильтрацию сигналов RSI с помощью индикатора MACD, чтобы уменьшить количество неэффективных сделок.

-

Можно установить стоп-лосс на основе ATR, чтобы избежать крупных убытков при экстремальных движениях.

-

Можно оптимизировать параметры количества добавлений, процентов и тейк-профита для разных инструментов.

-

Можно динамически корректировать процент тейк-профита в зависимости от волатильности, увеличивая его при высокой волатильности.

Заключение

Данная стратегия эффективно использует индикатор RSI для определения зоны перепроданности в сочетании со скользящей средней для разворотной торговли. Применяя механизмы интеллектуального добавления и постепенного тейк-профита, она реализует эффективную длинную стратегию с контролем риска. Оптимизация параметров индикаторов и механизма тейк-профита позволяет сделать стратегию более стабильной и эффективной. Стратегия может широко применяться к финансовым инструментам с разворотным характером, таким как фьючерсы на индексы, криптовалюты и т.д., и обладает практической инвестиционной ценностью.

- 1