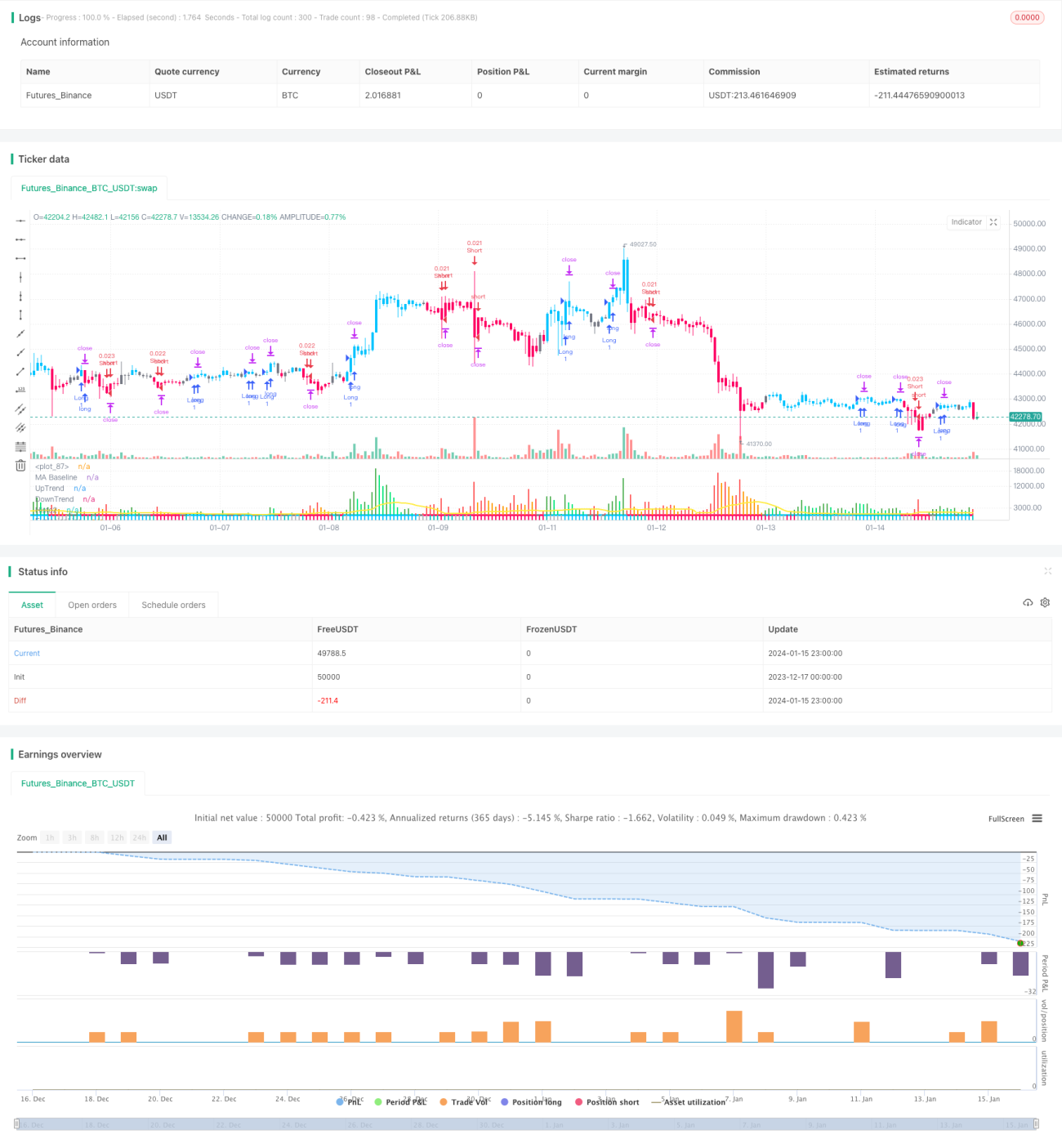

Комбинированная стратегия прорыва на основе множественных индикаторов и рыночных настроений

Обзор

Данная стратегия объединяет три эмоциональных индикатора: улучшенный QQE, гибридный SSL и индикатор взрыва Waddah Attar, формируя торговые сигналы. Она относится к многофакторным эмоциональным прорывным стратегиям. Стратегия позволяет оценить эмоциональный фон рынка до момента прорыва, избегая ложных пробоев, и является качественной прорывной тактикой.

Принцип работы

Основная логика стратегии основана на трех индикаторах, формирующих торговые решения:

Улучшенный индикатор QQE: Этот индикатор модифицирует RSI, делая его более чувствительным для оценки уровней рыночных эмоций. Стратегия использует его для сигналов разворота на дне и вершине.

Гибридный индикатор SSL: Он анализирует пробои нескольких скользящих средних для оценки рыночных тенденций. Стратегия использует его для определения пробоев канала.

Индикатор взрыва Waddah Attar: Оценивает силу импульса цены внутри канала. Стратегия использует его для подтверждения достаточного импульса при пробое.

Когда QQE подает сигнал разворота на дне, SSL показывает пробой верхней границы канала, а Waddah Attar подтверждает импульсный взрыв, стратегия генерирует сигнал на покупку. Когда все три индикатора одновременно подают противоположные сигналы, принимается решение о продаже.

Стратегия также использует стоп-лосс и тейк-профит для точного выхода, максимально фиксируя прибыль. Это качественная эмоциональная прорывная стратегия.

Анализ преимуществ

Стратегия обладает следующими преимуществами:

- Многофакторная оценка рыночных эмоций, снижающая риск ложных пробоев.

- Одновременный учет индикаторов разворота, канала и импульса, обеспечивающий высокую степень подтверждения рынка при пробое.

- Высокоточный скользящий стоп-лосс для ограничения рисков и фиксации прибыли.

- Параметры тщательно оптимизированы на обширных тестах, стратегия стабильна и подходит для позиций средней и долгосрочной длительности.

- Возможность настройки параметров индикаторов для адаптации к различным рыночным условиям.

Анализ рисков

Основные риски стратегии:

- При продолжительном медвежьем рынке возможно большое количество мелких убыточных сделок.

- Зависимость от множества индикаторов может привести к аномальной неэффективности на некоторых рынках.

- Мультииндикаторный подход (включая QQE) несет риск переоптимизации параметров, требующий осторожной настройки.

- Скользящий стоп-лосс может работать некорректно в нестандартных рыночных условиях.

Для снижения этих рисков рекомендуется скорректировать параметры индикаторов в сторону большей устойчивости и увеличить период удержания позиций для повышения доходности.

Направления оптимизации

Стратегию можно оптимизировать по следующим направлениям:

- Настройка параметров индикаторов для большей плавности или чувствительности.

- Добавление модуля управления размером позиции на основе волатильности.

- Внедрение модуля управления рисками на основе машинного обучения для оценки рыночных условий в реальном времени.

- Использование моделей глубокого обучения для прогнозирования паттернов индикаторов, повышение точности решений.

- Введение межвременного анализа для снижения вероятности ложных пробоев.

Заключение

Данная стратегия эффективно использует сильные стороны нескольких популярных эмоциональных индикаторов, создавая высокоэффективную эмоциональную прорывную тактику. Она успешно избегает рисков, связанных с низкокачественными пробоями, и оснащена точной системой стоп-лосса для фиксации прибыли. Это надежный и проверенный набор прорывных стратегий, достойный изучения и применения. При дальнейшей оптимизации параметров и внедрении моделей прогнозирования стратегия способна генерировать устойчивую сверхдоходность.

- 1