Стратегия следования за трендом на основе множества индикаторов

Обзор

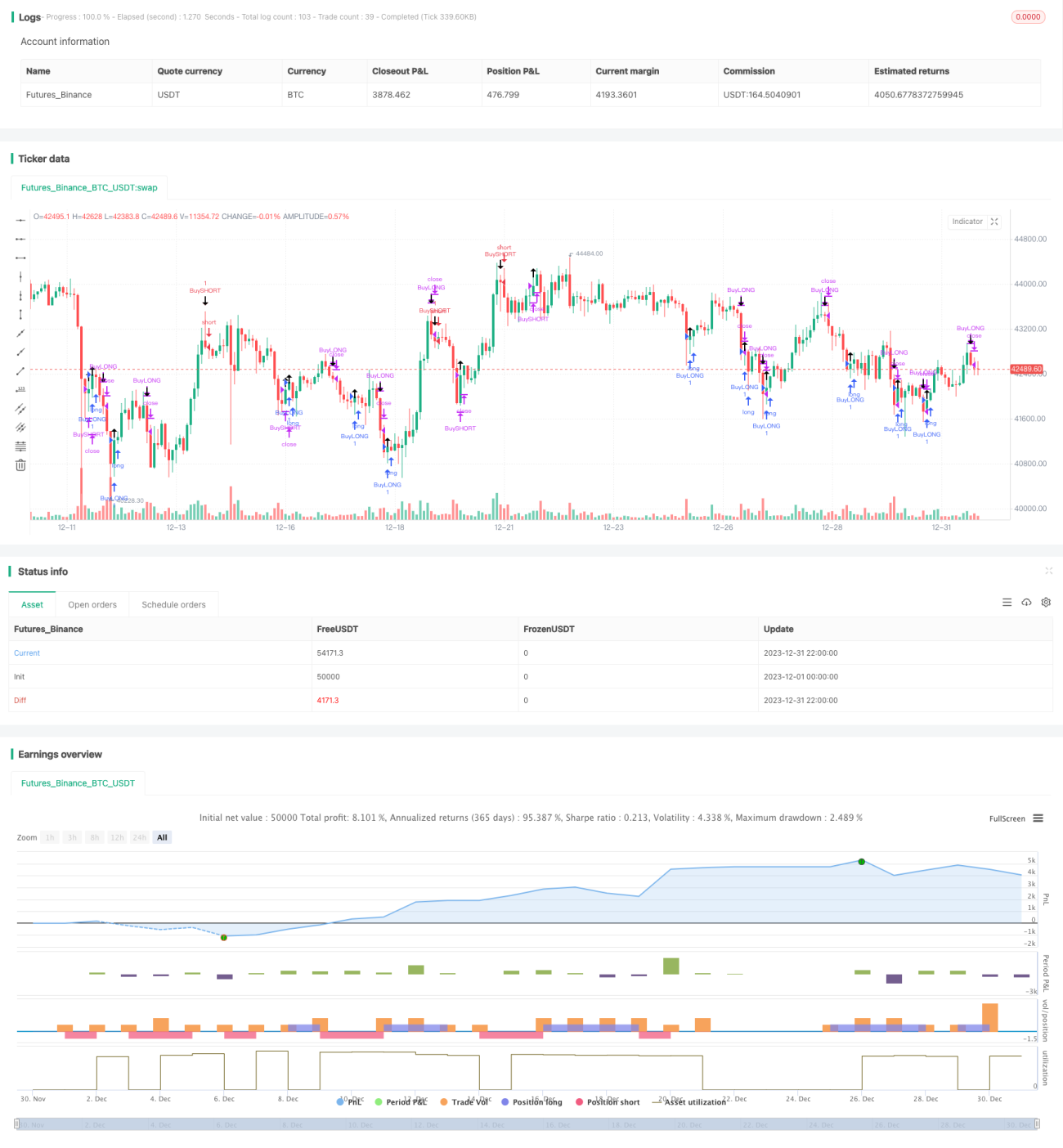

Данная стратегия определяет тренд путем комбинирования нескольких индикаторов и устанавливает трейлинг-стоп для фиксации прибыли. В основном используются полосы Боллинджера, RSI, ADX для определения момента входа, а также ATR и полосы Боллинджера для стоп-лосса.

Принцип стратегии

Основными индикаторами стратегии являются полосы Боллинджера, RSI и ADX. Когда цена приближается к нижней полосе Боллинджера и RSI ниже 30, это считается перепроданностью – открывается длинная позиция. Когда цена приближается к верхней полосе Боллинджера и RSI выше 70, это считается перекупленностью – открывается короткая позиция. Кроме того, если ADX превышает 25, считается, что тренд сформирован, и сигналы на покупку/продажу становятся более эффективными.

После открытия позиции стратегия использует индикатор ATR и верхнюю/нижнюю полосы Боллинджера для установки стоп-лосса. В частности, ATR используется для максимального уровня стоп-лосса: если цена достигает максимальной точки стоп-лосса, позиция закрывается. Верхняя и нижняя полосы Боллинджера используются для установки трейлинг-стопа, который обновляется в реальном времени в зависимости от движения цены.

Анализ преимуществ

Данная стратегия сочетает в себе несколько индикаторов для эффективного определения тренда и использует механизм стоп-лосса для фиксации прибыли и снижения риска убытков. Это довольно консервативная стратегия. Конкретные преимущества:

- Использование полос Боллинджера для определения перекупленности/перепроданности позволяет выявлять моменты разворота.

- Комбинирование с индикатором RSI повышает точность.

- Индикатор ADX определяет формирование тренда, обеспечивая правильное направление торговли.

- Трейлинг-стоп на основе ATR и полос Боллинджера позволяет максимально зафиксировать прибыль.

Анализ рисков

Эта стратегия также имеет некоторые риски:

- Использование нескольких индикаторов делает параметры подверженными переоптимизации.

- При широком диапазоне полос Боллинджера сигналы перекупленности/перепроданности становятся менее эффективными.

- Неправильное отслеживание стоп-лосса может привести к увеличению убытков.

Для снижения этих рисков можно предпринять следующие меры:

- Оптимизация комбинаций параметров для предотвращения переоптимизации.

- Настройка параметров полос Боллинджера в зависимости от волатильности рынка.

- Тестирование параметров расстояния стоп-лосса, чтобы убедиться, что они выдерживают нормальные колебания.

Направления оптимизации

Данную стратегию можно оптимизировать в следующих направлениях:

- Добавить контроль размера позиции, корректируя его в зависимости от множителя стоп-лосса.

- Добавить модуль управления капиталом для строгого контроля убытка по одной сделке.

- Протестировать другие индикаторы стоп-лосса, такие как DMI, Envelopes и т.д.

- Добавить модель машинного обучения для оценки вероятности тренда, чтобы повысить эффективность.

Заключение

В целом, эта стратегия представляет собой относительно консервативную трендовую стратегию. Определяя направление тренда с помощью множества индикаторов и используя меры по контролю рисков (стоп-лосс), можно получить хорошую доходность. Мы также предложили несколько направлений для оптимизации, которые при дальнейшей доработке могут привести к еще лучшим результатам.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1