ڈیجیٹل کرنسی اسپاٹ ملٹی ویریٹی ڈبل ای ایم اے حکمت عملی (ٹیوٹوریل)

مصنف:لیدیہ, تخلیق: 2022-11-08 12:50:56, تازہ کاری: 2023-09-15 20:57:25

کمیونٹی کے صارفین کی درخواست پر جو ڈیزائن حوالہ کے لئے کثیر اقسام کی ڈبل ای ایم اے حکمت عملی رکھنا چاہتے ہیں۔ اس مضمون میں ، ہم کثیر اقسام کی ڈبل ای ایم اے حکمت عملی کو نافذ کریں گے۔ حکمت عملی کوڈ پر تبصرے آسان تفہیم اور سیکھنے کے ل written لکھے جائیں گے۔ پروگرامنگ اور مقداری تجارت کے زیادہ نئے آنے والوں کو جلدی سے شروعات کرنے دیں۔

حکمت عملی کے خیالات

ڈبل ای ایم اے حکمت عملی کا منطق بہت آسان ہے ، یعنی دو ای ایم اے۔ ایک ای ایم اے (فاسٹ لائن) جس میں پیرامیٹر کی مدت چھوٹی ہے اور ایک ای ایم اے (سست لائن) جس میں پیرامیٹر کی مدت بڑی ہے۔ اگر دونوں لائنوں میں سنہری کراس ہے (فاسٹ لائن نیچے سے اوپر تک سست لائن سے گزرتی ہے) تو ہم خریدتے ہیں اور طویل ہوجاتے ہیں۔ اور اگر دونوں لائنوں میں مردہ کراس ہے (فاسٹ لائن اوپر سے نیچے تک سست لائن سے گزرتی ہے) تو ہم فروخت کرتے ہیں اور مختصر ہوجاتے ہیں۔ ہم یہاں ای ایم اے کا استعمال کرتے ہیں۔

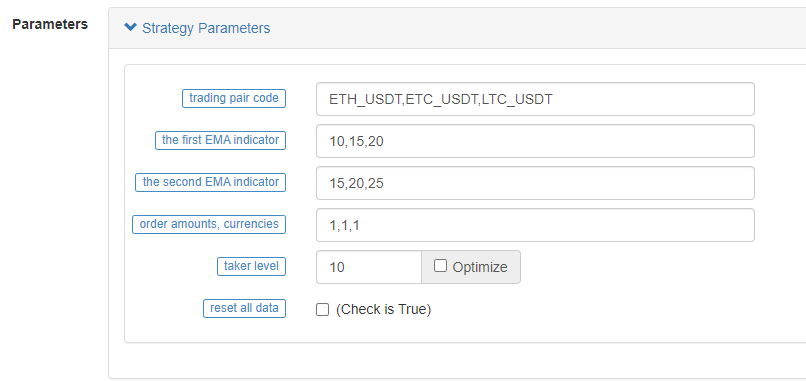

تاہم ، حکمت عملی کو کثیر قسم کے طور پر ڈیزائن کیا جانا چاہئے ، لہذا ہر قسم کے پیرامیٹرز مختلف ہوسکتے ہیں (مختلف قسمیں مختلف EMA پیرامیٹرز استعمال کرتی ہیں) ، لہذا پیرامیٹرز کو ڈیزائن کرنے کے لئے

پیرامیٹرز کو اسٹرنگ کی شکل میں ڈیزائن کیا گیا ہے ، ہر پیرامیٹر کو کوما سے الگ کیا گیا ہے۔ جب حکمت عملی چلنا شروع ہوتی ہے تو ان تاروں کو تجزیہ کریں۔ عملدرآمد کا منطق ہر قسم (ٹریڈنگ جوڑی) سے ملتا ہے۔ گھومنے والی حکمت عملی ہر قسم کی مارکیٹ کا پتہ لگاتی ہے ، تجارتی حالات کو متحرک کرتی ہے ، چارٹ پرنٹنگ وغیرہ۔ تمام اقسام کو ایک بار گھومنے کے بعد ، اعداد و شمار کا خلاصہ کریں اور اسٹیٹس بار پر ٹیبل کی معلومات دکھائیں۔

یہ حکمت عملی بہت سادہ اور نئے آنے والوں کے لئے موزوں ہونے کے لئے ڈیزائن کی گئی ہے، مجموعی طور پر صرف 200+ کوڈ لائنوں کے ساتھ.

حکمت عملی کا کوڈ

// Function: cancel all takers of the current trading pair

function cancelAll(e) {

while (true) {

var orders = _C(e.GetOrders)

if (orders.length == 0) {

break

} else {

for (var i = 0 ; i < orders.length ; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

Sleep(500)

}

}

// Functionn: calculate the profit/loss in real-time

function getProfit(account, initAccount, lastPrices) {

// account is the current account information, initAccount is the initial account information, lastPrices is the latest price of all varieties

var sum = 0

_.each(account, function(val, key) {

// Iterate through all current assets, calculate the currency difference of assets other than USDT, and the amount difference

if (key != "USDT" && typeof(initAccount[key]) == "number" && lastPrices[key + "_USDT"]) {

sum += (account[key] - initAccount[key]) * lastPrices[key + "_USDT"]

}

})

// Return to the profit and loss of the asset based on the current prices

return account["USDT"] - initAccount["USDT"] + sum

}

// Function: generate chart configuration

function createChartConfig(symbol, ema1Period, ema2Period) {

// symbol is the trading pair, ema1Period is the first EMA period, ema2Period is the second EMA period

var chart = {

__isStock: true,

extension: {

layout: 'single',

height: 600,

},

title : { text : symbol},

xAxis: { type: 'datetime'},

series : [

{

type: 'candlestick', // K-line data series

name: symbol,

id: symbol,

data: []

}, {

type: 'line', // EMA data series

name: symbol + ',EMA1:' + ema1Period,

data: [],

}, {

type: 'line', // EMA data series

name: symbol + ',EMA2:' + ema2Period,

data: []

}

]

}

return chart

}

function main() {

// Reset all data

if (isReset) {

_G(null) // Clear data of all persistent records

LogReset(1) // Clear all logs

LogProfitReset() // Clear all return logs

LogVacuum() //Release the resources occupied by the real bot database

Log("Reset all data", "#FF0000") // Print messages

}

// Parameter analysis

var arrSymbols = symbols.split(",") // Comma-separated string of trading varieties

var arrEma1Periods = ema1Periods.split(",") // Parameter string for splitting the first EMA

var arrEma2Periods = ema2Periods.split(",") // Parameter string for splitting the second EMA

var arrAmounts = orderAmounts.split(",") // Splitting the amount of orders placed for each variety

var account = {} // Variables used for recording current asset messages

var initAccount = {} // Variables used for recording initial asset messages

var currTradeMsg = {} // Variables used for recording whether current BAR trades

var lastPrices = {} // Variables used for recording the latest price of monitored varieties

var lastBarTime = {} // Variable used for recording the time of the last BAR, used to judge the update of BAR when drawing

var arrChartConfig = [] // Used for recording chart configuration message and draw

if (_G("currTradeMsg")) { // For example, restore currTradeMsg data when restarting

currTradeMsg = _G("currTradeMsg")

Log("Restore records", currTradeMsg)

}

// Initialize account

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol)

var arrCurrencyName = symbol.split("_")

var baseCurrency = arrCurrencyName[0]

var quoteCurrency = arrCurrencyName[1]

if (quoteCurrency != "USDT") {

throw "only support quoteCurrency: USDT"

}

if (!account[baseCurrency] || !account[quoteCurrency]) {

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

}

// Initialize chart-related data

lastBarTime[symbol] = 0

arrChartConfig.push(createChartConfig(symbol, arrEma1Periods[index], arrEma2Periods[index]))

})

if (_G("initAccount")) {

initAccount = _G("initAccount")

Log("Restore initial account records", initAccount)

} else {

// Initialize the initAccount variable with the current asset information

_.each(account, function(val, key) {

initAccount[key] = val

})

}

Log("account:", account, "initAccount:", initAccount) // Print asset information

// Initialize the chart object

var chart = Chart(arrChartConfig)

// Chart reset

chart.reset()

// Strategy main loop logic

while (true) {

// Iterate through all varieties and execute the double-EMA logic one by one

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol) // Switch the trading pair to the trading pair of symbol string record

var arrCurrencyName = symbol.split("_") // Split the trading pairs with the "_" symbol

var baseCurrency = arrCurrencyName[0] // String for trading currencies

var quoteCurrency = arrCurrencyName[1] // String for denominated currency

// Obtain the EMA parameters of the current trading pair according to the index

var ema1Period = parseFloat(arrEma1Periods[index])

var ema2Period = parseFloat(arrEma2Periods[index])

var amount = parseFloat(arrAmounts[index])

// Obtain the K-line data of the current trading pair

var r = exchange.GetRecords()

if (!r || r.length < Math.max(ema1Period, ema2Period)) { // Return directly if K-line length is insufficient

Sleep(1000)

return

}

var currBarTime = r[r.length - 1].Time // Record the current BAR timestamp

lastPrices[symbol] = r[r.length - 1].Close // Record the latest current price

var ema1 = TA.EMA(r, ema1Period) // Calculate EMA indicators

var ema2 = TA.EMA(r, ema2Period) // Calculate EMA indicators

if (ema1.length < 3 || ema2.length < 3) { // The length of EMA indicator array is too short, return directly

Sleep(1000)

return

}

var ema1Last2 = ema1[ema1.length - 2] // EMA on the penultimate BAR

var ema1Last3 = ema1[ema1.length - 3] // EMA on the third from the last BAR

var ema2Last2 = ema2[ema2.length - 2]

var ema2Last3 = ema2[ema2.length - 3]

// Write data to the chart

var klineIndex = index + 2 * index

// Iterate through the K-line data

for (var i = 0 ; i < r.length ; i++) {

if (r[i].Time == lastBarTime[symbol]) { // Draw the chart, update the current BAR and indicators

// update

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close], -1)

chart.add(klineIndex + 1, [r[i].Time, ema1[i]], -1)

chart.add(klineIndex + 2, [r[i].Time, ema2[i]], -1)

} else if (r[i].Time > lastBarTime[symbol]) { // Draw the charts, add BARs and indicators

// add

lastBarTime[symbol] = r[i].Time // Update timestamp

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close])

chart.add(klineIndex + 1, [r[i].Time, ema1[i]])

chart.add(klineIndex + 2, [r[i].Time, ema2[i]])

}

}

if (ema1Last3 < ema2Last3 && ema1Last2 > ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// Golden cross

var depth = exchange.GetDepth() // Obtain the depth data of current order book

var price = depth.Asks[Math.min(takeLevel, depth.Asks.length)].Price // Take the 10th grade price, taker

if (depth && price * amount <= account[quoteCurrency]) { // Obtain deep data normally with enough assets to place an order

exchange.Buy(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2) // Place a buy order

cancelAll(exchange) // Cancel all makers

var acc = _C(exchange.GetAccount) // Obtain account asset information

if (acc.Stocks != account[baseCurrency]) { // Detect changes in account assets

account[baseCurrency] = acc.Stocks // Update assets

account[quoteCurrency] = acc.Balance // Update assets

currTradeMsg[symbol] = currBarTime // Record that the current BAR has been traded

_G("currTradeMsg", currTradeMsg) // Persistent records

var profit = getProfit(account, initAccount, lastPrices) // Calculate profits

if (profit) {

LogProfit(profit, account, initAccount) // Print profits

}

}

}

} else if (ema1Last3 > ema2Last3 && ema1Last2 < ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// dead cross

var depth = exchange.GetDepth()

var price = depth.Bids[Math.min(takeLevel, depth.Bids.length)].Price

if (depth && amount <= account[baseCurrency]) {

exchange.Sell(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2)

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

if (acc.Stocks != account[baseCurrency]) {

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

currTradeMsg[symbol] = currBarTime

_G("currTradeMsg", currTradeMsg)

var profit = getProfit(account, initAccount, lastPrices)

if (profit) {

LogProfit(profit, account, initAccount)

}

}

}

}

Sleep(1000)

})

// Table variables in the status bar

var tbl = {

type : "table",

title : "Account Information",

cols : [],

rows : []

}

// Write data into the status bar table structure

tbl.cols.push("--")

tbl.rows.push(["initial"])

tbl.rows.push(["current"])

_.each(account, function(val, key) {

if (typeof(initAccount[key]) == "number") {

tbl.cols.push(key)

tbl.rows[0].push(initAccount[key]) // initial

tbl.rows[1].push(val) // current

}

})

// Show status bar table

LogStatus(_D(), "\n", "profit:", getProfit(account, initAccount, lastPrices), "\n", "`" + JSON.stringify(tbl) + "`")

}

}

حکمت عملی کا بیک ٹسٹ

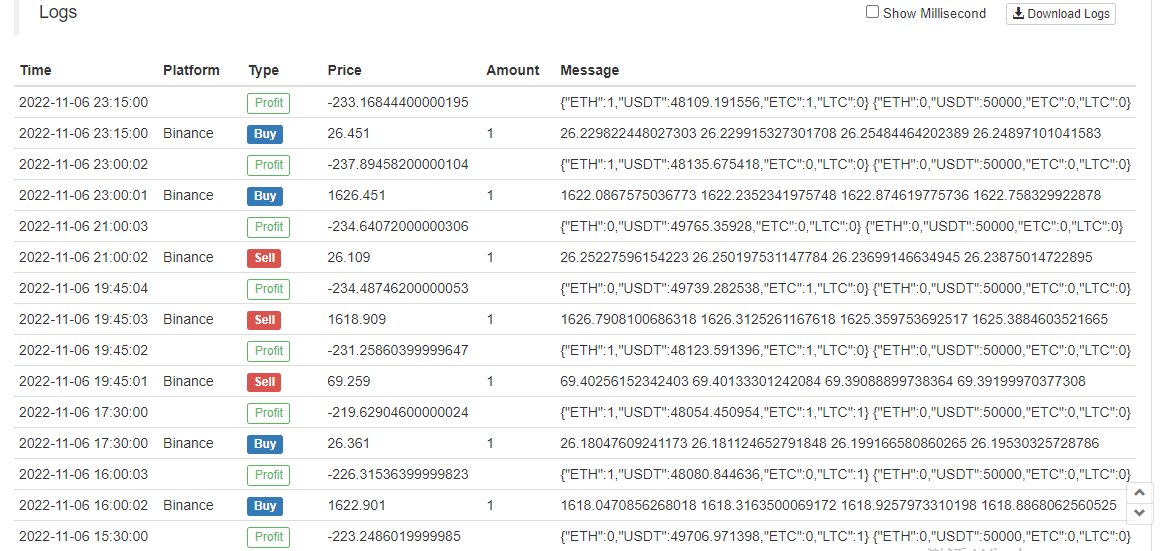

یہ دیکھا جا سکتا ہے کہ ETH، LTC اور ETC کو ای ایم اے کے گولڈن کراس اور ڈیڈ کراس کے مطابق ٹرگر کیا جاتا ہے، اور ٹریڈنگ ہوئی ہے۔

ہم ٹیسٹنگ کے لیے ایک سمیلیٹر روبوٹ بھی لے سکتے ہیں۔

حکمت عملی کا ماخذ کوڈ:https://www.fmz.com/strategy/333783

حکمت عملی backtesting کے لئے استعمال کیا جاتا ہے، سیکھنے کی حکمت عملی ڈیزائن صرف، اور یہ حقیقی بوٹ میں احتیاط کے ساتھ استعمال کیا جانا چاہئے.