تین نمونوں کی دوغلہ تجارتی حکمت عملی

خلاصہ

تین گنا اتار چڑھاؤ کی تجارتی حکمت عملی ایک قلیل مدتی تجارتی حکمت عملی ہے جو متعدد تکنیکی اشاریوں کے امتزاج پر مبنی ہے۔ یہ حکمت عملی سپر ٹرینڈ انڈیکیٹر، SSL مخلوط اوسط اور بہتر QQE انڈیکیٹر کو ملا کر مستحکم تجارتی سگنلز بناتی ہے۔ یہ ڈیجیٹل کرنسیوں اور اسٹاکس جیسے زیادہ اتار چڑھاؤ والے تجارتی آلات کے لیے موزوں ہے، خاص طور پر بریک آؤٹ کے بعد کے ادوار میں اچھی کارکردگی دکھاتی ہے۔

اصول

داخلے کے سگنل

لمبی پوزیشن میں داخلہ:

- سپر ٹرینڈ خالی سے لمبی میں تبدیل ہوتا ہے۔

- بند ہونے والی قیمت SSL مخلوط بنیاد کی اوپری لکیر کو اوپر سے کراس کرتی ہے۔

- QQE کا بہتر ورژن نیلا ہوتا ہے (لمبی)۔

خالی پوزیشن میں داخلہ:

- سپر ٹرینڈ لمبی سے خالی میں تبدیل ہوتا ہے۔

- بند ہونے والی قیمت SSL مخلوط بنیاد کی نچلی لکیر کو نیچے سے کراس کرتی ہے۔

- QQE کا بہتر ورژن سرخ ہوتا ہے (خالی)۔

خارج ہونے کے سگنل

لمبی پوزیشن سے خارج: سپر ٹرینڈ لمبی سے خالی میں تبدیل ہوتا ہے۔

خالی پوزیشن سے خارج: سپر ٹرینڈ خالی سے لمبی میں تبدیل ہوتا ہے۔

نقصان روکنا

فیصدی نقصان روکنا، ATR نقصان روکنا، یا حالیہ بلند ترین اور پست ترین قیمتوں پر مبنی نقصان روکنا منتخب کیا جا سکتا ہے۔

منافع بند کرنا

منافع بند کرنے کا تناسب مقرر کیا جا سکتا ہے، اور منافع بند کرنے کی قیمت خود بخود شمار ہو جاتی ہے۔

سرمایہ کا انتظام

اختیاری طور پر سرمایہ کے انتظام کی منطق استعمال کی جا سکتی ہے تاکہ پوزیشن کے سائز کو کنٹرول کیا جا سکے۔

خاکہ نویسی

- سپر ٹرینڈ لائن اور SSL مخلوط اوسط کا چینل بنایا جاتا ہے۔

- اختیاری طور پر EMA اوسط لائن بنائی جا سکتی ہے۔

- لمبی اور خالی پوزیشنوں کے کھلنے، نقصان روکنے، اور منافع بند کرنے کی لکیریں بنائی جاتی ہیں۔

- لمبی اور خالی پوزیشنوں کے کھلنے کے لیبل بنائے جاتے ہیں۔

فوائد

-

متعدد اشاریوں کا امتزاج، مستحکم تجارتی سگنل تشکیل

سپر ٹرینڈ، SSL مخلوط اوسط، اور QQE کے بہتر ورژن کو ملا کر، مختلف اشاریے ایک دوسرے کی تصدیق کرتے ہیں، جھوٹے بریک آؤٹ کو فلٹر کرتے ہیں، اور اعلیٰ معیار کے تجارتی سگنل بناتے ہیں۔

-

اتار چڑھاؤ والے آلات کے لیے اتار چڑھاؤ کی تجارت کے لیے موزوں

یہ حکمت عملی قلیل مدتی تجارت کا طریقہ استعمال کرتی ہے اور درمیانی سے قلیل مدتی قیمتوں کے اتار چڑھاؤ کو پکڑنے پر توجہ مرکوز کرتی ہے۔ سپر ٹرینڈ قیمت کے رجحان کو مؤثر طریقے سے ٹریک کر سکتا ہے، جبکہ SSL مخلوط اوسط مزاحمت اور سپورٹ کی سطحوں کو واضح طور پر پہچان سکتی ہے، دونوں کا استعمال اتار چڑھاؤ والی مارکیٹ میں منافع حاصل کرنے میں مدد کرتا ہے۔

-

نقصان روکنے اور منافع بند کرنے کے متعدد طریقے منتخب کرنے کے قابل

نقصان روکنے کے لیے فیصد، ATR قدر، یا حالیہ انتہائی اقدار میں سے انتخاب کیا جا سکتا ہے۔ منافع بند کرنے کے لیے منافع کا تناسب مقرر کیا جا سکتا ہے۔ سرمایہ کا انتظام پوزیشن کے سائز کو کنٹرول کر سکتا ہے۔ صارف اپنے آلے کی خصوصیات اور خطرے کی ترجیحات کے مطابق آزادانہ طور پر امتزاج کر سکتا ہے۔

-

واضح خاکہ نویسی

حکمت عملی کی خاکہ نویسی واضح ہے، اور نقصان روکنے اور منافع بند کرنے کی لکیریں بصری طور پر دکھائی دیتی ہیں۔ کھلنے کی لکیروں کے نشانات تجارتی سگنلز کو پہچاننے میں آسانی پیدا کرتے ہیں۔

خطرات اور بہتری

-

چھوٹے نقصانات کا امکان

قلیل مدتی تجارت کی وجہ سے، عام اتار چڑھاؤ والے چھوٹے نقصانات سے مکمل طور پر بچنا ممکن نہیں۔ نقصان روکنے کی حد کو قدرے بڑھایا جا سکتا ہے اور سرمایہ کے انتظام کی منطق کو بہتر بنایا جا سکتا ہے۔

-

جھوٹے بریک آؤٹ کا خطرہ

جب قیمت جھوٹا بریک آؤٹ کرتی ہے، تو غلط سگنل پیدا ہو سکتے ہیں۔ جھوٹے بریک آؤٹ کو فلٹر کرنے کے لیے مختلف ادوار کے EMA کو آزمایا جا سکتا ہے، یا رجحان کی شناخت کرنے والے اشاریوں کے پیرامیٹرز کو بہتر بنایا جا سکتا ہے۔

-

اشاریوں کے ناکام ہونے کا خطرہ

اگر بنیادی اشاریے ناکام ہو جائیں، تو متعدد غلط سگنل پیدا ہوں گے۔ اشاریوں کی تاثیر کو باقاعدگی سے جانچنا ضروری ہے، اور مسائل پائے جانے پر فوری طور پر ایڈجسٹمنٹ کرنی چاہیے۔

-

بیک ٹیسٹنگ کی مدت کو بہتر بنانا

موجودہ بیک ٹیسٹنگ کی مدت ایک مقررہ وقت کی مدت ہے، جو مختلف آلات کی مارکیٹ سائیکل کے مطابق نہیں ہوتی۔ تجویز ہے کہ اسے متعلقہ معاہدے کے اہم تجارتی وقت کی مدت کے مطابق بہتر بنایا جائے۔

-

آلات کے لیے موافقت کو بہتر بنانا

مختلف آلات کے ڈیٹا کی خصوصیات کے مطابق، حکمت عملی کے پیرامیٹرز کو ٹھیک ٹیون کیا جا سکتا ہے تاکہ لمبی اور خالی پوزیشنوں کی جیت کی شرح بہتر ہو سکے۔ تجویز ہے کہ مرحلہ وار آپٹیمائزیشن کا طریقہ استعمال کریں تاکہ مختلف پیرامیٹرز کے حکمت عملی پر اثرات کا موازنہ کیا جا سکے۔

خلاصہ

یہ حکمت عملی متعدد اشاریوں کو ملا کر تجارتی سگنل بناتی ہے، جو جھوٹے بریک آؤٹ کو مؤثر طریقے سے فلٹر کر سکتی ہے، اور زیادہ اتار چڑھاؤ والی ڈیجیٹل کرنسیوں اور انفرادی اسٹاکس کے لیے موزوں ہے۔ اس کے علاوہ، یہ نقصان روکنے اور منافع بند کرنے کے متعدد طریقے فراہم کرتی ہے جو منتخب کیے جا سکتے ہیں، جس سے یہ لچکدار ہے۔ مجموعی طور پر، یہ حکمت عملی مستحکم تجارتی سگنل بناتی ہے اور درمیانی سے قلیل مدتی اتار چڑھاؤ والی مارکیٹ میں اچھے منافع حاصل کر سکتی ہے۔ مزید بہتری کے ذریعے، مختلف تجارتی آلات کے لیے پیرامیٹرز کو بہتر بنایا جا سکتا ہے، جس سے حکمت عملی کا منافع کا تناسب بڑھ سکتا ہے۔ یہ حکمت عملی ایک قابل غور اور مؤثر تجارتی نظام ہے۔

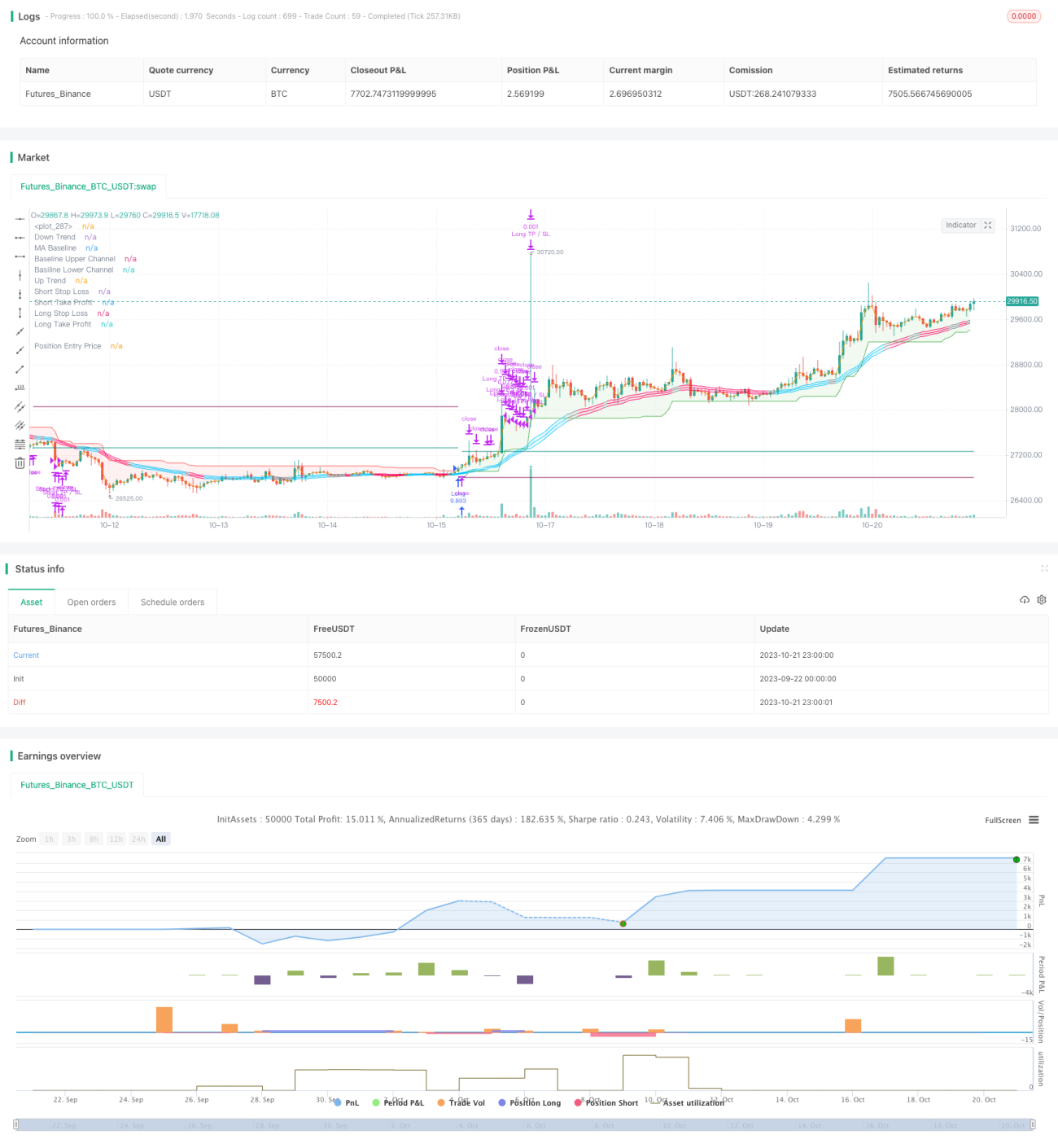

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1