متعدد اشاروں پر مبنی رجحان کی پیروی کی حکمت عملی

خلاصہ

یہ حکمت عملی 3 اوپن سورس انڈیکیٹرز کو ملا کر کثیر وقتی رجحان کا تعین کرتی ہے، اور منافع کو محفوظ کرنے کے لیے اسٹاپ لاس اور ٹیک پرافٹ مقرر کرتی ہے۔ خاص طور پر، حکمت عملی مختصر مدت کے رجحان کی سمت کا تعین کرنے کے لیے AK MACD BB انڈیکیٹر کا استعمال کرتی ہے، SSL انڈیکیٹر کچھ جھوٹے سگنلز کو فلٹر کرتا ہے، اور آخر میں VSF انڈیکیٹر کے ساتھ مل کر حقیقی خرید و فروخت کی قوت کا فیصلہ کرتی ہے تاکہ داخلے کا مناسب وقت معلوم کیا جا سکے۔ اس کے ساتھ ساتھ، حکمت عملی میں پہلے سے طے شدہ اسٹاپ لاس اور ٹیک پرافٹ پوائنٹس ہیں جو منافع کو محفوظ رکھتے ہیں اور ایک ہی ٹریڈ کے نقصان کے خطرے کو کافی حد تک کم کر سکتے ہیں۔

حکمت عملی کا اصول

-

AK MACD BB انڈیکیٹر

یہ انڈیکیٹر MACD پر بولنگر بینڈ اپلائی کرتا ہے، جب MACD لائن بولنگر بینڈ کے اوپری بینڈ کو توڑتی ہے تو خرید کا سگنل پیدا ہوتا ہے، اور نیچے والے بینڈ کو توڑنے پر فروخت کا سگنل پیدا ہوتا ہے۔

-

SSL انڈیکیٹر

SSL انڈیکیٹر اس بات کا فیصلہ کرتا ہے کہ قیمت متحرک اوسط کو توڑ رہی ہے یا نہیں، اور واپسی کے سگنل کا پتہ لگاتا ہے۔ جب قیمت متحرک اوسط سے اوپر جاتی ہے اور SSL انڈیکیٹر نیلا ہوتا ہے تو یہ اوپر کی طرف رجحان ہے، اور جب قیمت اوسط سے نیچے آتی ہے اور SSL انڈیکیٹر سرخ ہوتا ہے تو یہ نیچے کی طرف رجحان ہے، اس طرح ٹریڈ کا سگنل جاری ہوتا ہے۔

-

VSF انڈیکیٹر

VSF انڈیکیٹر خریداروں اور فروخت کنندگان کی قوت کا فیصلہ کرتا ہے۔ حکمت عملی صرف اس وقت سگنل دیتی ہے جب خریداروں یا فروخت کنندگان کی قوت 50% سے زیادہ ہو، تاکہ بے معنی بریک آؤٹ سے بچا جا سکے۔

-

اسٹاپ لاس اور ٹیک پرافٹ

حکمت عملی میں 4 درجے کی ترقی پسند ٹیک پرافٹ (progressive take profit) شامل ہے، جو 1.5 گنا سے 3 گنا منافع کے وقفے پر سیٹ کی گئی ہے۔ اس کے ساتھ ساتھ 2% کا فکسڈ اسٹاپ لاس مقرر ہے، جو ایک ٹریڈ میں زیادہ سے زیادہ نقصان کو مؤثر طریقے سے کنٹرول کرتا ہے۔

فوائد کا تجزیہ

-

ایک سے زیادہ انڈیکیٹرز کا مجموعہ، درست فیصلہ

مختلف انڈیکیٹرز کے ذریعے کثیر وقتی رجحان کا تعین کرنے سے جھوٹے سگنلز کو فلٹر کیا جا سکتا ہے اور فیصلہ درست ہو جاتا ہے۔

-

خودکار ٹیک پرافٹ اور اسٹاپ لاس، خطرہ کنٹرول میں

حکمت عملی میں بلٹ ان ٹیک پرافٹ اور اسٹاپ لاس سیٹنگز ہیں، جو ایک ٹریڈ کے نقصان کو تقریباً 2% تک محدود رکھ سکتی ہیں اور بڑے نقصان سے بچ سکتی ہیں۔

-

بیک ٹیسٹ کے اعداد و شمار بہترین

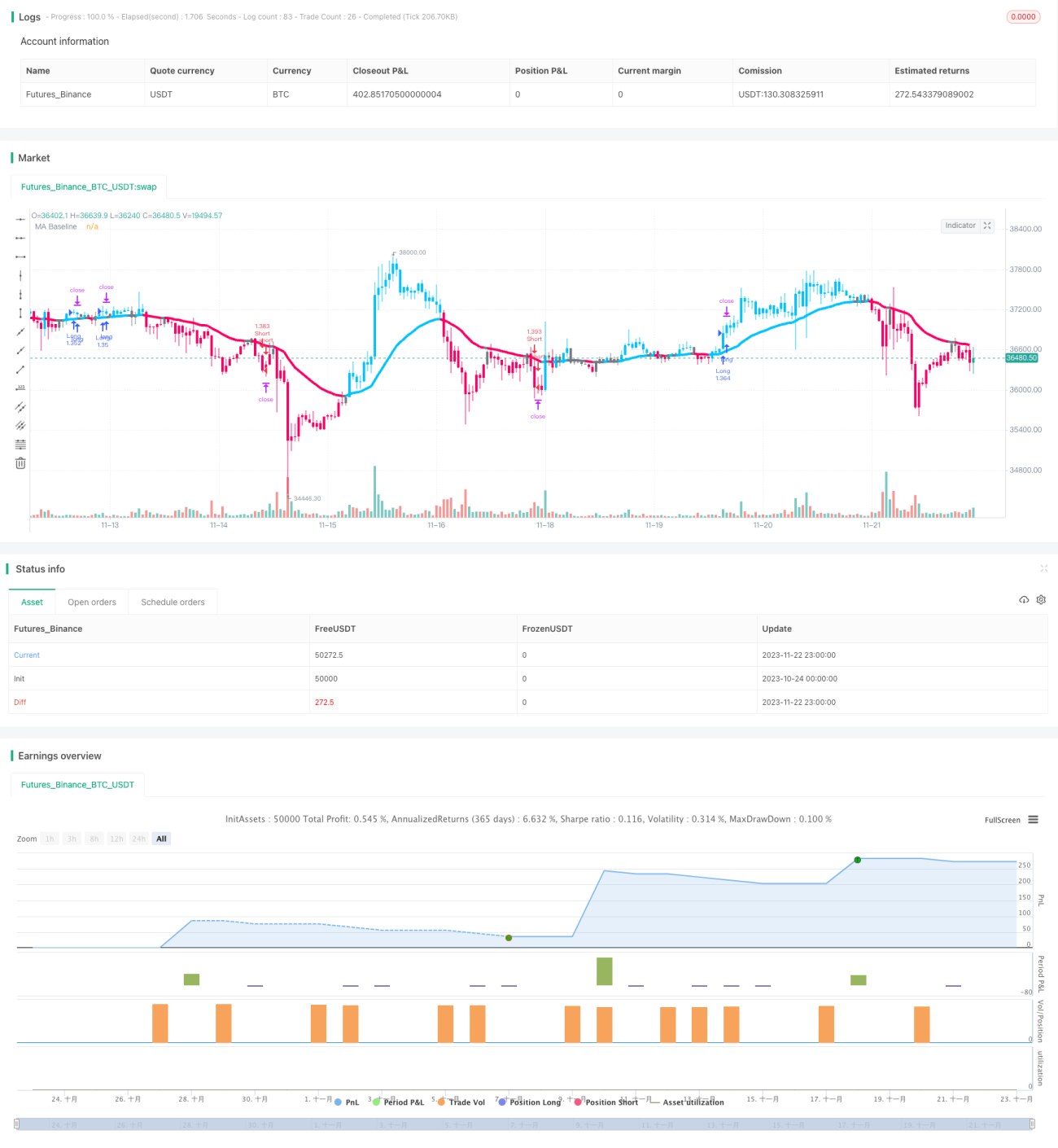

جاری کنندہ کے بیک ٹیسٹ کے مطابق، 100 ٹریڈز میں منافع بخش ٹریڈز 74% تھیں، اور کل منافع 427% تھا۔

خطرات اور ان کا مقابلہ کرنے کا تجزیہ

-

مارکیٹ میں شدید اتار چڑھاؤ کا خطرہ

بڑے پیمانے پر رینج میں اتار چڑھاؤ کے دوران، متعدد بار چھوٹے نقصان ہو سکتے ہیں۔ اس صورت میں، فکسڈ اسٹاپ لاس کی مقدار کو ایڈجسٹ کیا جا سکتا ہے یا ٹریڈنگ روک دی جا سکتی ہے۔

-

لمبی اور چھوٹی پوزیشنوں پر پابندی کا خطرہ

فی الحال حکمت عملی لمبی اور چھوٹی دونوں پوزیشنیں لے سکتی ہے۔ اگر صرف لمبی یا صرف چھوٹی پوزیشنوں تک محدود کر دیا جائے تو منافع کے مواقع آدھے رہ جائیں گے۔

-

ٹریڈنگ کے وقت کا خطرہ

حکمت عملی 5 منٹ کے ڈیٹا پر فیصلہ کرتی ہے۔ اگر ایک ٹریڈنگ دن میں صرف چند گھنٹوں کا ڈیٹا موجود ہو تو نمونے کی مقدار ناکافی ہوگی اور سگنلز قابل اعتماد نہیں ہوں گے۔

حکمت عملی کو بہتر بنانے کی سمت

-

اسٹاپ لاس اور ٹیک پرافٹ پیرامیٹرز کو بہتر بنانا

مختلف اسٹاپ لاس اور ٹیک پرافٹ کی سطحوں کی جانچ کی جا سکتی ہے تاکہ بہترین پیرامیٹرز مل سکیں۔ بہت چھوٹا اسٹاپ لاس خطرے کو مؤثر طریقے سے کنٹرول نہیں کر سکے گا، اور بہت بڑا اسٹاپ لاس زیادہ منافع سے محروم کر سکتا ہے۔

-

خودکار پوزیشن ایڈجسٹمنٹ شامل کرنا

منافع کو محفوظ کرنے کے لیے ٹریلنگ اسٹاپ لاس یا موونگ اسٹاپ لاس سیٹ کیا جا سکتا ہے۔ یا مخصوص حالات میں پوزیشن میں اضافہ کر کے زیادہ منافع حاصل کیا جا سکتا ہے۔

-

دیگر انڈیکیٹرز کے ساتھ ملانا

مختلف انڈیکیٹرز کے امتزاج کی جانچ کی جا سکتی ہے تاکہ یہ دیکھا جا سکے کہ کون سا امتزاج بہترین کام کرتا ہے۔ مزید انڈیکیٹرز کو شامل کر کے کراس تصدیق کی جا سکتی ہے۔

-

پیرامیٹر کی اصلاح

مختلف پیرامیٹرز کے ساتھ بیک ٹیسٹ کیا جا سکتا ہے تاکہ پیرامیٹر کی اصلاح کی سمت مل سکے۔ اس حکمت عملی میں، بولنگر بینڈ کے پیرامیٹرز یا موونگ ایوریج کے پیرامیٹرز کو تبدیل کرنے سے بہتر نتائج مل سکتے ہیں۔

خلاصہ

یہ حکمت عملی کئی انڈیکیٹرز کو ملا کر رجحان کی سمت کا تعین کرتی ہے اور خودکار ٹیک پرافٹ اور اسٹاپ لاس سیٹ کرتی ہے، جو مضبوط رجحان میں منافع کما سکتی ہے اور ایک ٹریڈ کے نقصان کو بہت چھوٹی حد میں رکھ سکتی ہے۔ جاری کنندہ کے بیک ٹیسٹ کے اعداد و شمار سے پتہ چلتا ہے کہ اس کا منافع بخش تناسب اور منافع کی شرح دونوں بہت اچھی ہیں۔ مناسب اصلاح کے ذریعے، حکمت عملی کے استحکام اور منافع بخش صلاحیت کو مزید بہتر بنانے کی امید کی جا سکتی ہے۔

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © myn

//@version=5

strategy('Strategy Myth-Busting #7 - MACDBB+SSL+VSF - [MYN]', max_bars_back=5000, overlay=true, pyramiding=0, initial_capital=1000, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=1.0, commission_value=0.075, use_bar_magnifier = false)

/////////////////////////////////////

//* Put your strategy logic below *//

/////////////////////////////////////

//nwVqTuPe6yo- 1