EMA/ADX/VOL - کریپٹو کرنسی قاتل

EMA اوسط نظام کے ذریعے رجحان کی سمت کا تعین، ADX اشاریہ کے ذریعے رجحان کی شدت کا تعین، اور تجارتی حجم کی فلٹرنگ کے ساتھ داخلے کا مقداری تجارتی حکمت عملی

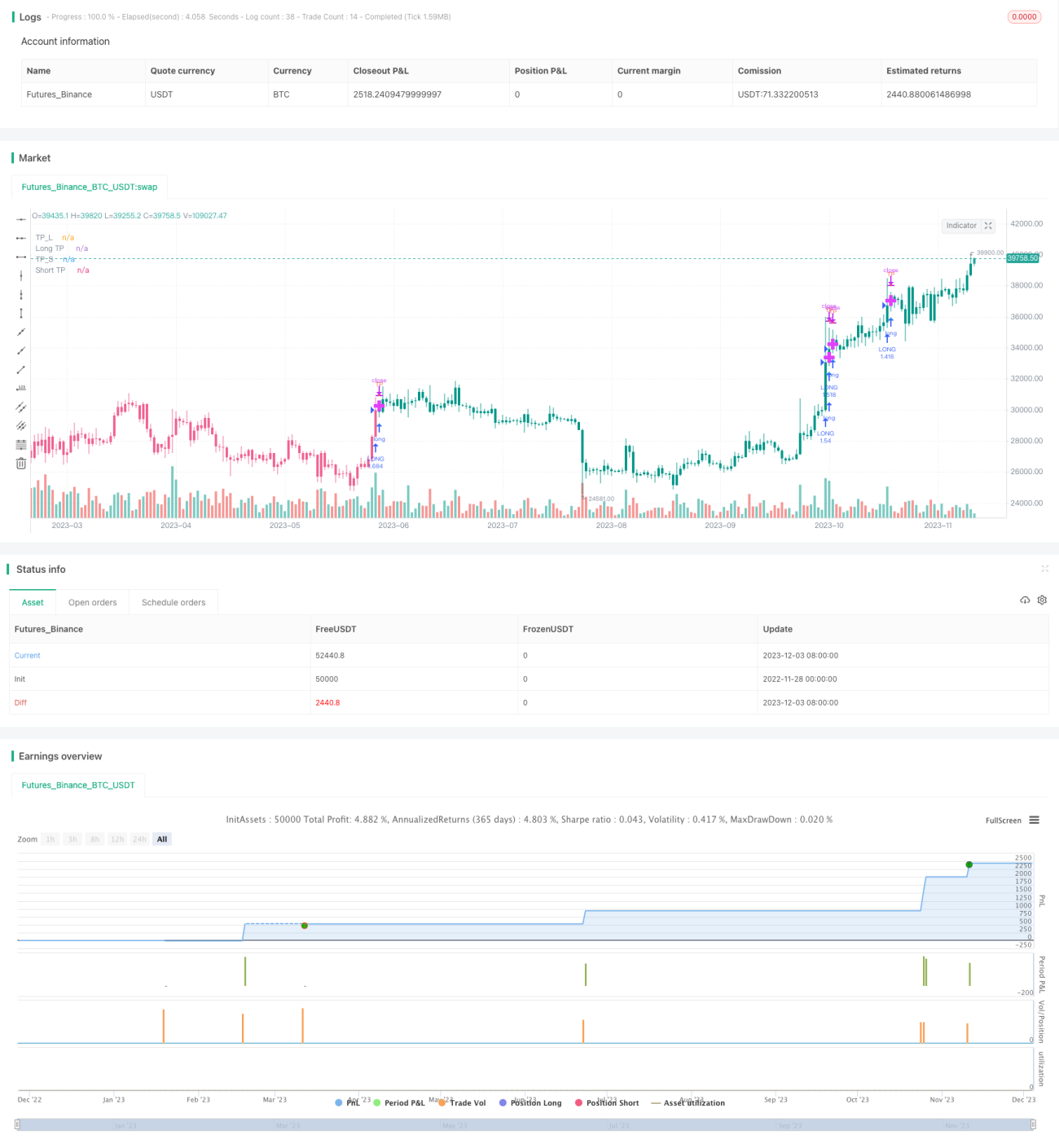

اصول

یہ حکمت عملی سب سے پہلے 5 مختلف ادوار کی EMA اوسطوں کے ذریعے قیمت کے رجحان کی سمت کا تعین کرتی ہے۔ جب 5 EMA اوسطیں سبھی بڑھتی ہوں تو صعودی رجحان کی تشکیل کا فیصلہ کیا جاتا ہے، اور جب 5 EMA اوسطیں سبھی گرتی ہوں تو نزولی رجحان کی تشکیل کا فیصلہ کیا جاتا ہے۔

پھر ADX اشاریہ کے ذریعے رجحان کی شدت کا تعین کیا جاتا ہے۔ جب DI+ لائن DI- لائن سے اوپر ہو اور ADX قدر مقررہ حد سے تجاوز کر جائے تو مضبوط صعودی مارکیٹ کا فیصلہ کیا جاتا ہے، اور جب DI- لائن DI+ لائن سے اوپر ہو اور ADX قدر مقررہ حد سے تجاوز کر جائے تو نزولی مارکیٹ کا فیصلہ کیا جاتا ہے۔

ساتھ ہی، تجارتی حجم کے اچانک اضافے کو اضافی تصدیق کے طور پر استعمال کیا جاتا ہے، جس میں موجودہ K-line کا تجارتی حجم ایک مخصوص مدت کی اوسط حجم سے کئی گنا زیادہ ہونا ضروری ہے، تاکہ کم حجم والی جگہوں پر غلط داخلے سے بچا جا سکے۔

رجحان کی سمت، رجحان کی شدت، اور تجارتی حجم کے جامع فیصلے کو ملا کر اس حکمت عملی کے صعودی اور نزولی پوزیشن کھولنے کے منطق تشکیل پاتے ہیں۔

فوائد

-

EMA اوسط نظام کا استعمال رجحان کی سمت کا تعین کرنے کے لیے، واحد EMA اوسط کے مقابلے میں زیادہ قابل اعتماد ہے۔

-

ADX اشاریہ کی مدد سے رجحان کی شدت کا تعین، واضح رجحان کے بغیر غلط داخلے سے بچتا ہے۔

-

تجارتی حجم کی فلٹرنگ کا طریقہ کار، اس بات کو یقینی بناتا ہے کہ کافی تجارتی حجم موجود ہو، جس سے حکمت عملی کی قابل اعتمادی بڑھتی ہے۔

-

متعدد شرائط کا جامع فیصلہ، پوزیشن کھولنے کے اشارے کو زیادہ درست اور قابل اعتماد بناتا ہے۔

-

حکمت عملی کے پیرامیٹرز کی زیادہ تعداد، پیرامیٹر کی اصلاح کے ذریعے حکمت عملی کی کارکردگی کو مسلسل بہتر بنانے کی گنجائش فراہم کرتی ہے۔

خطرات اور حل

-

اتار چڑھاؤ والی مارکیٹ میں، EMA اوسط اور ADX جیسے فیصلے غلط اشارے دے سکتے ہیں، جس سے غیر ضروری نقصان ہو سکتا ہے۔ پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کیا جا سکتا ہے، یا فیصلے میں مدد کے لیے دیگر اشاریوں کو شامل کیا جا سکتا ہے۔

-

تجارتی حجم کی فلٹرنگ کی شرط بہت سخت ہونے کی وجہ سے مارکیٹ کے مواقع ضائع ہو سکتے ہیں۔ تجارتی حجم فلٹرنگ کے پیرامیٹرز کو کم کیا جا سکتا ہے۔

-

حکمت عملی سے پیدا ہونے والی تجارتی تعدد زیادہ ہو سکتی ہے، لہٰذا سرمایہ کے انتظام پر توجہ دینے اور ہر پوزیشن کے سائز کو مناسب طور پر کنٹرول کرنے کی ضرورت ہے۔

بہتری کے راستے

-

مختلف پیرامیٹر مجموعوں کی جانچ کریں، بہترین پیرامیٹر تلاش کریں، اور حکمت عملی کی کارکردگی کو بہتر بنائیں۔

-

دیگر اشاریوں جیسے MACD، KDJ کو EMA اور ADX کے ساتھ ملا کر مزید مضبوط جامع پوزیشن کھولنے کا فیصلہ تیار کریں۔

-

نقصان کو روکنے کی حکمت عملی شامل کریں تاکہ خطرے کو مزید کنٹرول کیا جا سکے۔

-

پوزیشن مینجمنٹ کی حکمت عملی کو بہتر بنائیں تاکہ زیادہ سائنسی سرمایہ کا انتظام ممکن ہو سکے۔

خلاصہ

یہ حکمت عملی قیمت کے رجحان کی سمت، رجحان کی شدت، اور تجارتی حجم کی معلومات کو یکجا کر کے پوزیشن کھولنے کے قواعد تشکیل دیتی ہے، جس سے عام جال میں پھنسنے سے کسی حد تک بچا جا سکتا ہے اور اس میں کافی قابل اعتمادی ہے۔ تاہم، پیرامیٹر کی اصلاح، اشاریوں کی بہتری، اور خطرے کے کنٹرول کے ذریعے حکمت عملی کے نظام کو مزید مکمل کرنے اور کارکردگی کو بہتر بنانے کی ضرورت ہے۔ مجموعی طور پر، اس حکمت عملی کے فریم ورک میں وسیع توسیع کی صلاحیت اور بہتری کی گنجائش موجود ہے۔

- 1